下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编每天为您准备了5道每日一练题目(附答案解析),一步一步陪你备考,每一次练习的成功,都会淋漓尽致的反映在分数上。一起加油前行。

1、Equity return series are best described as, for the most part:【单选题】

A.platykurtotic (less peaked than a normal distribution).

B.leptokurtotic (more peaked than a normal distribution).

C.mesokurtotic (identical to the normal distribution in peakedness).

正确答案:B

答案解析:“Statistical Concepts and Market Returns,” Richard A. DeFusco, CFA, Dennis W. McLeavey, CFA, Jerald E. Pinto, CFA, and David E. Runkle, CFA

2013 Modular Level I, Vol. 1, Reading 7, Section 9

Study Session 2–7–l

Explain measures of sample skewness and kurtosis.

B is correct. Most equity return series have been found to be leptokurtotic.

2、An analyst does research about risk management applications of option strategies.With respect to option strategies, the shape of the graph that illustrates both thevalue at expiration and profit for buying a call is most similar in shape to thegraph for:【单选题】

A.selling a put.

B.a covered call position.

C.a protective put position.

正确答案:C

答案解析:有保护的看跌期权(protective put position)是购买一股股票的同时再买人针对该股票的一个看跌期权,当股票价格上涨时股票可以获利,看跌期权没有价值;而如果股票价格下跌股票损失时,看跌期权则可以获利,所以从图形上来看其收益类似于购买了一个看涨期权。

3、The probability of Event A is 40%. The probability of Event B is 60%. The joint probability of AB is40%. The probability (P) that A or B occurs, or both occur, is closest to:【单选题】

A.60%.

B.40%.

C.84%.

正确答案:A

答案解析:P(A or B)=P(A)+P(B)-P(AB)=0.40+0.60-0.40=0.60 or 60%.

CFA Level I

"Probability Concepts," Richard A. DeFusco, Dennis W. McLeavey, Jerald E. Pinto, and David E.Runkle

Section 2

4、The price of a good falls from $15 to $13. Given this decline in price, the quantity demanded of the good rises from 100 units to 120 units. The price elasticity of demand for the good is closest to:【单选题】

A.1.3.

B.1.5.

C.10.0.

正确答案:A

答案解析:“Elasticity,” Michael Parkin

2011 Modular Level I, Vol. 2, pp. 10-11

Study Session 4-13-a

Calculate and interpret the elasticities of demand (price elasticity, cross elasticity, and income elasticity) and the elasticity of supply and discuss the factors that influence each measure.

Price elasticity of demand is calculated as:

Price elasticity of demand = %ΔQ / %ΔP = (ΔQ / Qave) / (ΔP / Pave)

In this case, (20 / 110) / (2 / 14) = 1.27 rounded to 1.3

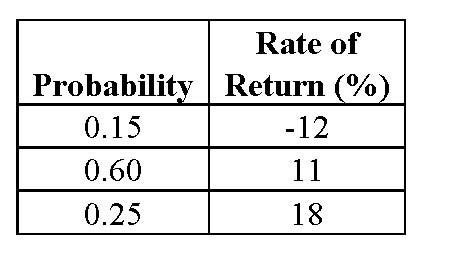

5、The table below provides a probability distribution of stock returns for shares of Orion Corporation:

The variance of returns for Orion Corporation stock is closest to:【单选题】

A.44.36

B.50.94

C.88.71

正确答案:C

答案解析:“An Introduction to Portfolio Management,” Frank K. Reilly and Keith C. Brown

2010 Modular Level I, Vol. 4, pp.242-244

Study Session 12-50-c

Compute and interpret the expected return, variance, and standard deviation for an

individual investment and the expected return and standard deviation for a portfolio.

C is correct. The table below provides the calculation of the variance

Expected return E( R) = 9.3%

Variance of returns = 88.71

459

459What are the indices for a skewed distribution?:What are the indices for a skewed distribution?

265

265What are the responsibilities of the members in reference to the CFA Institute?:Once accepted as a member:每年交述职报告和年费but must not over promise the competency and future investment results.Case

640

640What members and candidates should notice in CFA examinations?:or security of the CFA examinations.(不能恶心CFA),考试不能作弊:考试内容要保密:A. No.:Responsibilities as a CFA Institute Member.right④Case

微信扫码关注公众号

获取更多考试热门资料