下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

报考了2020年ACCA考试的小伙伴们注意了,你们复习的怎么样了?今天帮考网分享2020年ACCA考试:会计师与企业基础练习题(6),快来看看吧!

IAS 1 (revised) Presentation of financial statements

- Dividend cannot be shown in profit or loss (income statement). Dividends must be presented on the face of the statement of changes in equity or in the notes

- Statement of changes in equity for owner changes in equity. Non-owner changes in equity. Non-owner changes must be shown in the statement of comprehensive income.

- Revaluation gains must be shown the other comprehensive income

IAS 8 (revised) Accounting policies, changes in accounting estimates and errors

Accounting policies are the specific principles, bases, conventions, rules and practices adopted by an entity in preparing and presenting financial statements.

IFRS 8 Operating segments (replaced IAS 14 Segment reporting)

IFRS 8 is a disclosure standard:

- Segment reporting is necessary for a better understanding and assessment of:

. Past performance

. Risks and returnswww.Examw.com

. Informed judgements

- IFRS 8 adopts the managerial approach to identifying segments.

- The standard gives guidance on how segment should be identified and what information should be disclosed for each

It also sets out requirements for related disclosures about products and services, geographical areas and major customers.

IAS 33 Earnings per share

Earnings per share is a measure of the amount of profits earned by a company for each ordinary share. Earnings are profits after tax and preferred dividends

Ordinary share: an equity instrument that is subordinate to all other classes of equity instruments.

Basic EPS: is calculated by dividing the net profit or loss for the period attributable to ordinary shareholders by the weighted average number of ordinary shares outstanding during the period.

Basic EPS = Net profit/ (loss) attributable to ordinary shareholders /

Weighted average no. of ordinary shares outstanding

Effect on basic EPS OF changes in capital structure:

- New issues/buy backs,

- Capitalization/bonus issue, share split/reverse share split,

- Rights issue

Right issue:

To arrive at figures for EPS when a rights issue is made, first calculate the theoretical ex-rights price. This is a weighted average value per share.

今天的试题分享到此结束,预祝各位小伙伴顺利通过接下来的ACCA考试,如需查看更多ACCA考试试题,记得关注帮考网!

63

63ACCA报考有年龄限制吗?:ACCA报考有年龄限制吗?ACCA报考是没有年龄限制的,报名参加ACCA考试,1.凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;顺利完成了大一全年的所有课程考试,专即可报名成为ACCA的正式学员;3.未符合1、2项报名资格的申请者,可以先申请参加FIA资格考试,通过FFA、FMA和FAB三门课程后,可以申请转入ACCA并且豁免F1-F3三门课程的考试。

25

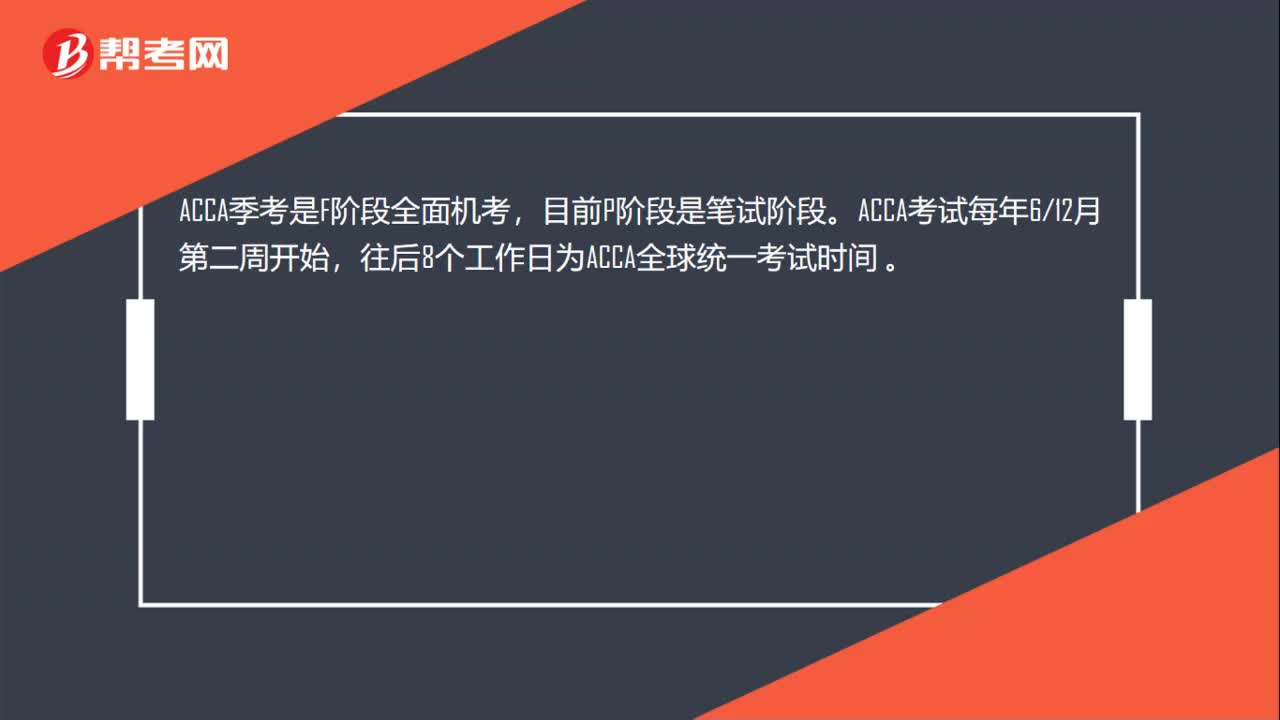

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

21

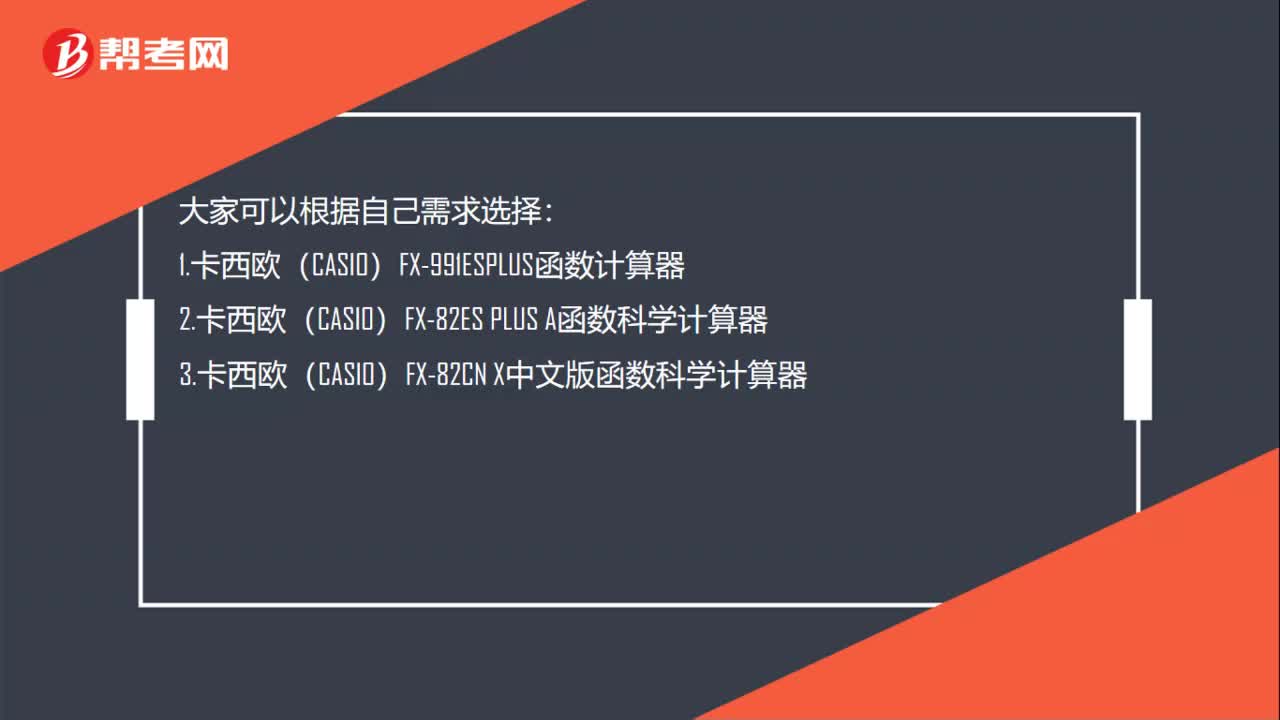

21ACCA考试用什么计算器?:ACCA考试用什么计算器?大家可以根据自己需求选择:1.卡西欧(CASIO)FX-991ESPLUS函数计算器2.卡西欧(CASIO)FX-82ESPLUS A函数科学计算器3.卡西欧(CASIO)FX-82CNX中文版函数科学计算器

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料