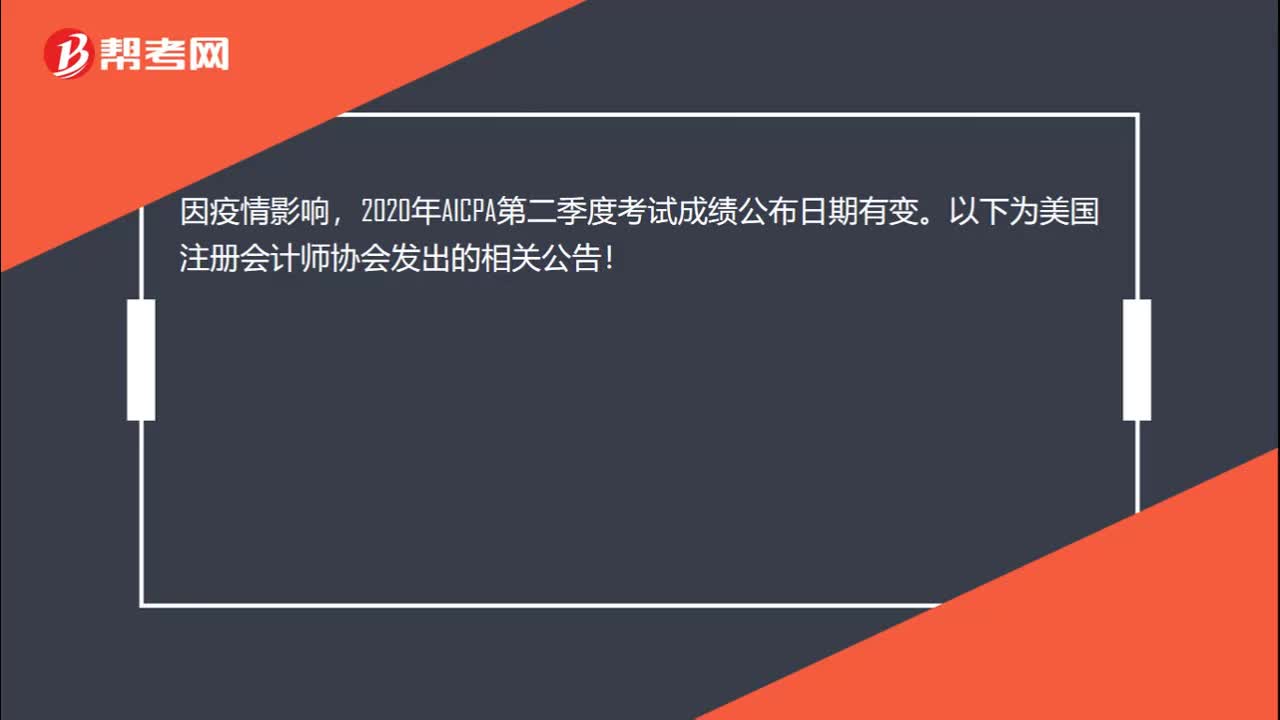

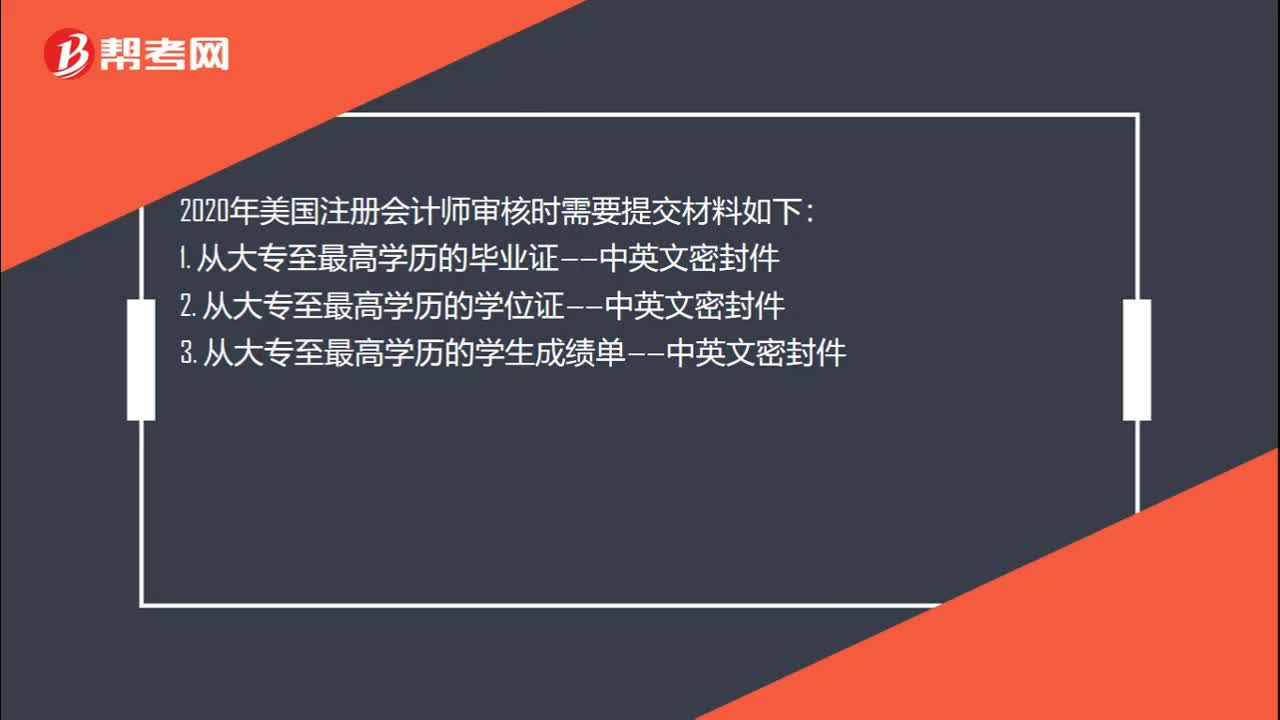

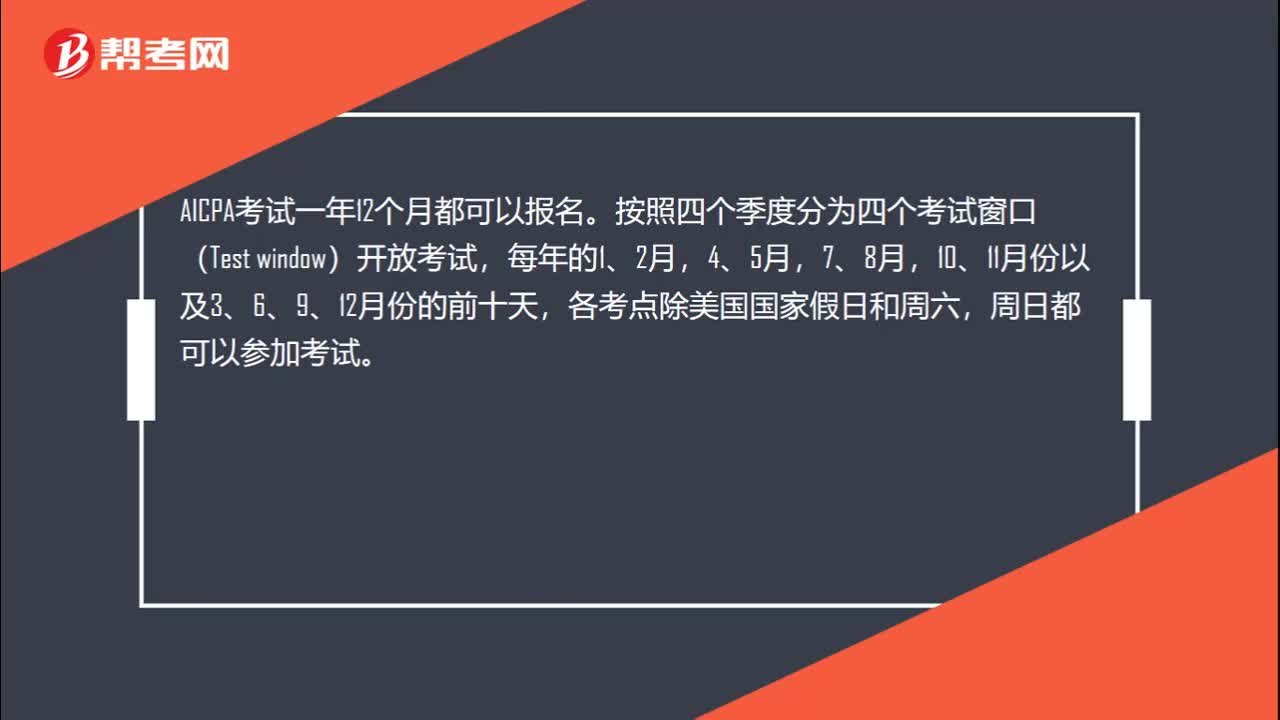

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Under U.S. GAAP, interest cost included in the net pension cost recognized for a period by an employer sponsoring a defined benefit pension plan represents the:

a. Increase in the fair value of plan assets due to the passage of time.

b. Amortization of the discount on unrecognized prior service costs.

c. Increase in the projected benefit obligation due to the passage of time.

d. Shortage between the expected and actual returns on plan assets.

答案:C

Explanation

Choice "c" is correct. Under U.S. GAAP, interest cost included in the net pension cost recognized for a period by an employer sponsoring a defined benefit pension plan represents the increase in the projected benefit obligation due to the passage of time.

Choice "d" is incorrect. The shortage between the expected and actual returns on plan assets represents a net loss from actual experience different from that assumed.

Choice "a" is incorrect. An increase in the fair value of the plan assets due to the passage of time represents the actual return on plan assets. (It excludes the contributions received and benefit payments made during the period.)

Choice "b" is incorrect. Amortization of the discount on unrecognized prior service costs represents the current period's expense relating to prior service costs (which were not recognized until this period).

86

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

30

302020年AICPA怎么报考?:2020年AICPA怎么报考?AICPA报考流程如下:1.学历预评估。2. 学分评估,确认报考州。3.学历认证。4.补学分。5.申请NTS。6.预约考位。7. 安排行程。8.申请执照。

22

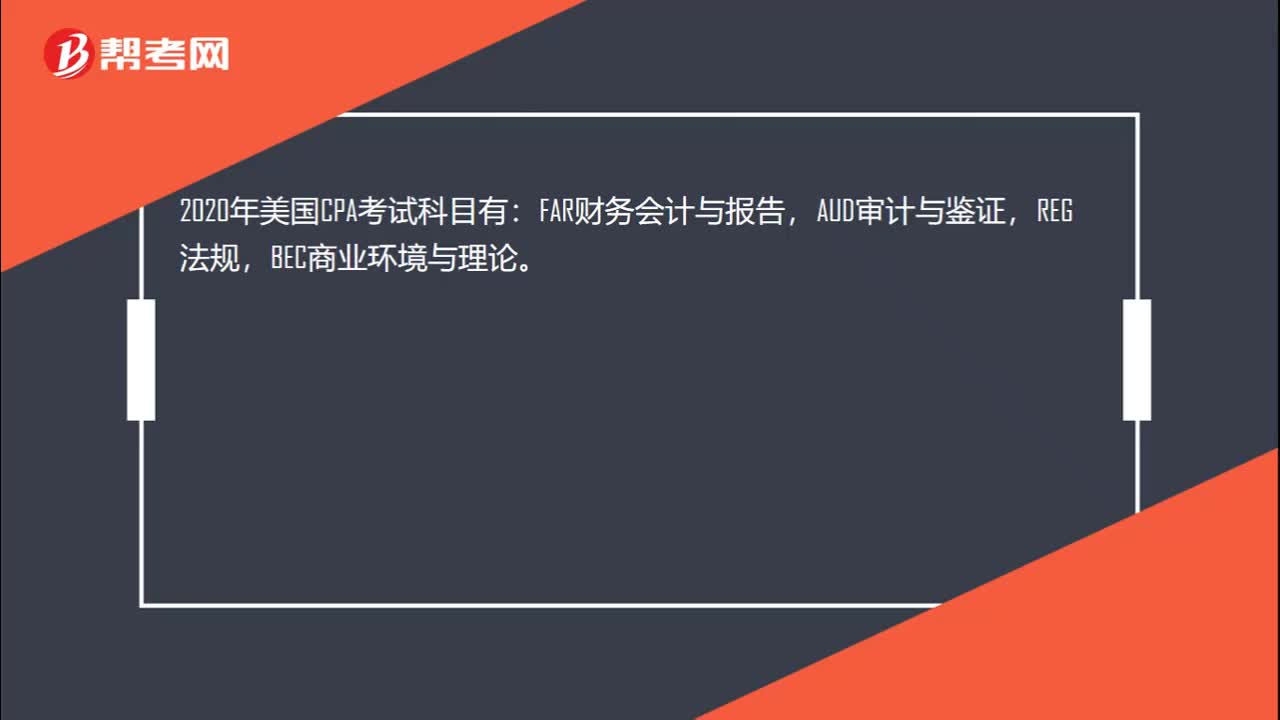

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料