下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Governmental funds net change

Other financing sources

Expenditure–capital outlay(net of depreciation)

Service(internal)fund net position

Basis of accounting

Accrued

Revenues and Expenses

基金合并成报告,时点时期要调整。

时点GLAS气(期)GOES,后果严重要裸奔(Bare)。

时点加减非流动,时期减加债固资。

内服两者都调整,裸奔长收与预提。

长收账期超六十,预提多与固相关。

GLAS,GOES,附BARE,调整分录已完成

Proprietary Funds require “Statement of Net Position”,“Statement of Revenues,Expenses,and Changes in Fund Net Position”,“Statement of Cash Flows”

The Cash flows similar to commercial enterprise,with seven difference.

There are four categories.The financing activities are classified as “Capital and related financing activities”+“Noncapital financing activities”

Interest income/cash receipts are reported as “investing activities”

Interest expense/cash payments are either “Capital and related financing” or “Noncapital financing”

Capital asset purchases are reported as “financing activities”。

For other 3 points,please refer to F9-29

Fiduciary Funds require “Statement of Fiduciary Net Position” and “Statement of Changes in Fiduciary Net Position”

Refer to F9-32

Notes to the Financial Statements considered integral to the F/S.Notes should focus on the primary government. The main discloses:

A description of government-wide activities.

Policies relating to elimination of internal activity.

Description of the modified approach for reporting infrastructure.

The length of time used to define“available”in determining revenue recognition under the modified accrual basis(60 days)

Required Supplementary Information

Budgetary Information–original budget,final amended budget,and actual amounts.

Infrastructure Information–assessed condition of infrastructure,and estimated annual amount to maintain the preserve infrastructure for each of the past five years.

Pension Information for 10 most recent fiscal years

Sources of changes

Information about the components

Significant methods and assumptions

Annual money-weighted rate of return

Explanation of trends in changes in benefit terms/in the population/in assumptions.

Other Supplementary Information

Combining statements for nonmajor funds

Variance between originally adopted budget and final amended budget

Variance between final amended budget and actual.

Interfund activity represents the flow of resources between funds and between the primary government and its component units.It can be classified as “Reciprocal” and“Non-reciprocal”interfund activity.

Reciprocal interfund activity include“interfund loans”and“interfund services provided and used”。

Non-reciprocal interfund activity include“interfund transfers”and“interfund reimbursement”。

Interfund transfers are normally displayed as other financing sources and uses after non-operating revenues and expenses.

Interfund reimbursements are not displayed as interfund transactions.

F/S elimination and display

Eliminate activity within governmental activities

Eliminate activity within business-type activities

Eliminate activity between governmental activities and business-type activities.

Report the ransaction between the primary government and its fiduciary funds,as if between external parties.

22

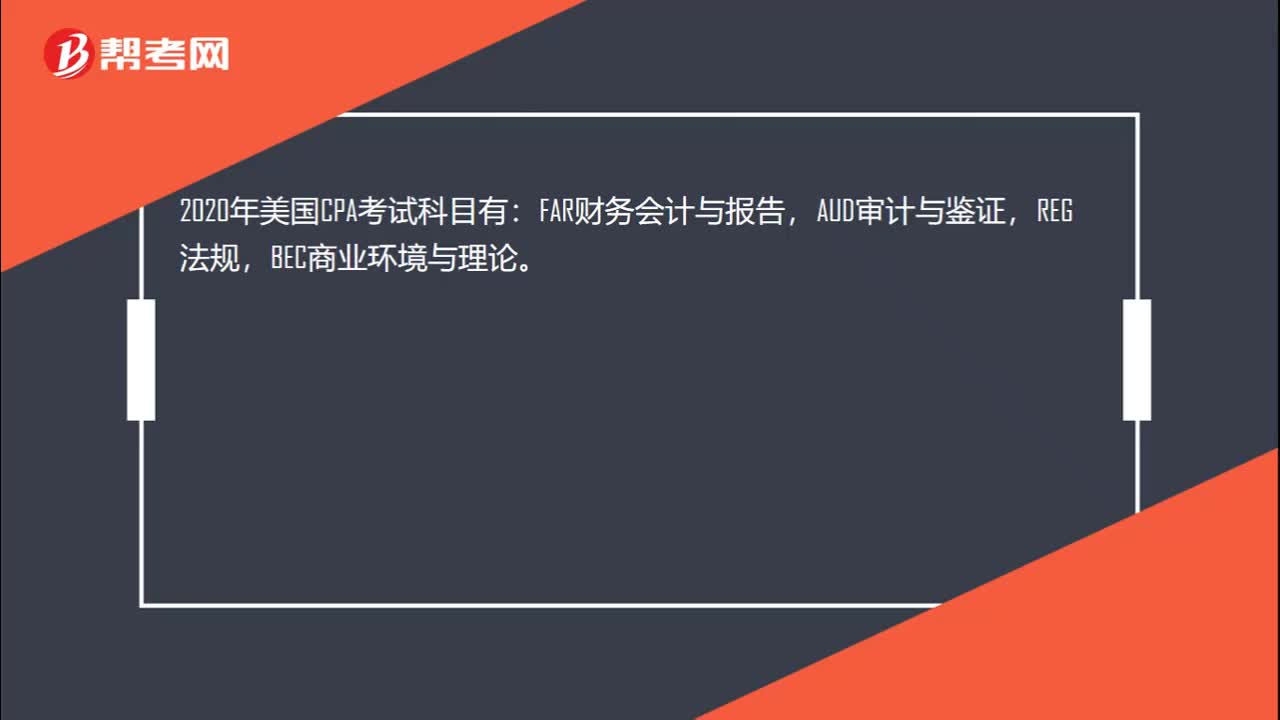

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

80

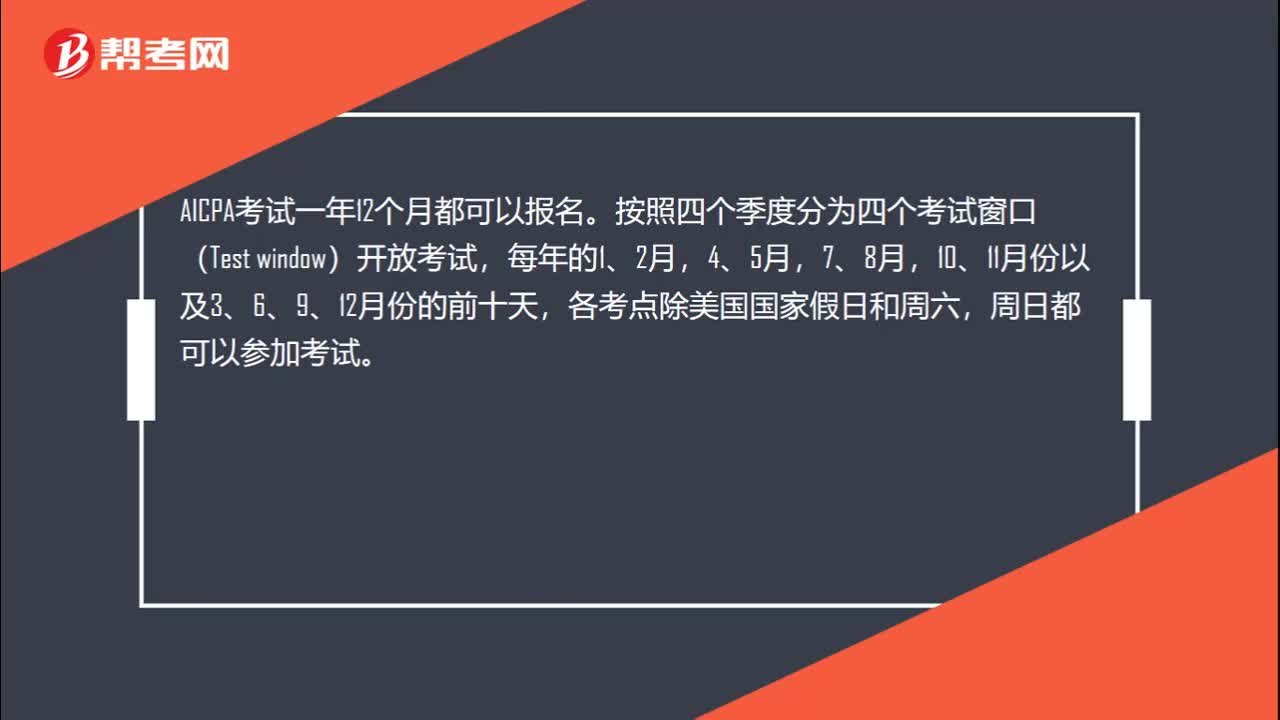

802020年美国CPA准考证打印时间延长了几个月?:2020年美国CPA准考证打印时间延长了几个月?NTS有效期在2020.4.1-2020.6.30期间到期的,NASBA会将NTS到期时间延长至2020.9.30。考生无需采取任何行动,也无需联系NASBA或您的州会计委员会。NASBA会在第一时间官方公布NTS及考试成绩完成延迟时间的更新。你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。

25

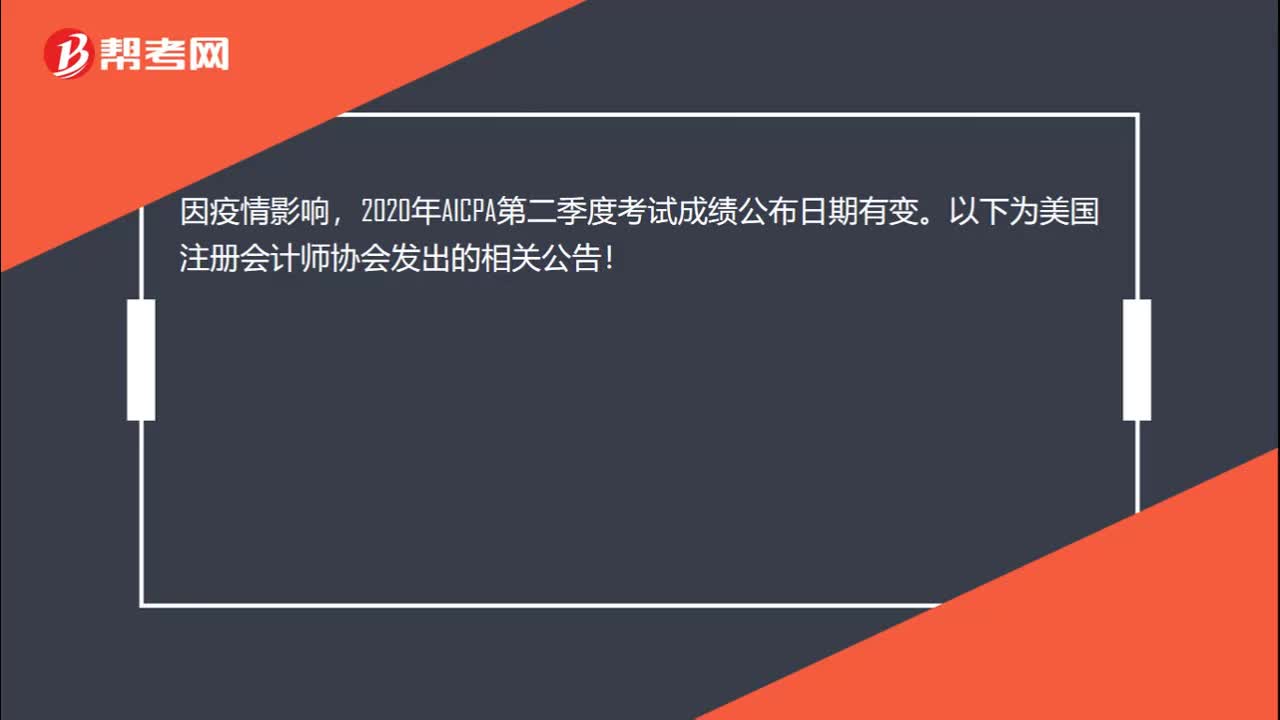

252020年美国注册会计师Q2考季成绩能查了吗?:2020年美国注册会计师Q2考季成绩能查了吗?因疫情影响,2020年AICPA第二季度考试成绩公布日期有变。以下为美国注册会计师协会发出的相关公告!

00:222020-05-21

01:202020-05-21

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料