下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Infrastructure asset refers to streets,bridges,gutters,and other assets of the government.

Infrastructure asset are recorded as general capital asset.They are only reported on the government-wide F/S.

Capitalization of construction period interest is not required for capital assets used in the governmental activities.

Required Vs. Modified Approach(subsequent measurement)

Required approach(for GASB 34 Depreciation of Capitalized Assets)。Depreciation expense that can be specifically identified with a functional category should be included in the direct expenses of that function.

Modified Approach (for GASB 34 Depreciation of Capitalized Assets)。Infrastructure assets that are part of a network or subsystem of a network are not required to be depreciated provided two requirements are met. Under the modified approach, infrastructure expenditures are typically reported as expenses, unless the outlays result in additions or improvements,in which case they would be capitalized.

Two requirements=Qualified Asset Management System+Disclosed Asset Preservation.

Qualified Asset Management System means

最新的合格资产清单

可计量的合格资产状况汇总

可估计的年度合格资产维保支出

Disclosed Asset Preservation

至少每三年进行一次彻底评估

评估结果证明合格资产的现状不差于政府设定并披露的标准

例子:X市考虑对排水管网采用modified approach. X市设定的排水标准为五年一遇。如果符合上述两标准,则可采用此方法。

RSI includes 1)reporting of the condition of the government‘s infrastructure;2)a comparison schedule of needed and actual expenditures to maintain the government’s infrastructure.

Change from required approach to modified approach or reverse,is accounting estimation change.

Impairment assessment are required.

Artwork and historical treasures

GR:Collection is capitalized on historical cost or fair value

SR:Not Capitalize. Need meet three conditions:

The collection is held for public exhibition

The collection is protected

The proceeds from sales of collection items to be used to acquire other items for collections

Interfund Activity

Within Government funds or Enterprise Fund,eliminated

Between Government fund and Enterprise Fund,reported as “Internal balances”

Between Government / Enterprise Funds and Fiduciary Funds reported as if external parties.

Statement of Activities is a consolidated statement of all governmental and business-type activities.It uses program approach.

The program approach provides cost information about the primary functions of the government and indicates each program‘s dependence on the general revenues of the government.

“BASE”of net position–Subtract(F9-19 上半部分)

In row direction,functions and programs are classified into three categories:

Primary government governmental activities

Primary government business-type activities

Component units

In column direction,there are expenses,indirect expenses allocation,and program revenue which is contain three 2nd tier revenues(“SOC”)

Charges for Services

Operating grants and contributions

Capital grants and contributions

Charges for services are revenues based on exchange or exchange-like transactions. E.g.water and sewer fee,building permits,housing prisoners, fines,and forfeitures,etc.

Operating / Capital grants and contributions are mandatory and voluntary NON-Exchange transactions,restricted for use in a particular program.

“BASE”of net position-Add(F9-19下半部分)

General revenues=taxes+interest earnings+other revenue

Special items and unusual OR infrequent and are within the control of management.

Internal service fund activity should generally be reported in the governmental activities column.

Fund F/S are required for the governmental,proprietary,and fiduciary funds.

GASB34 emphasize reporting by major fund.

Major fund must meet the 10% criteria within its category and also meet the 5% criteria associated with both categories.

Major fund criteria–Individual fund‘s total assets/liabilities/revenues/expenditures/expenses/deferred outflows of resources/deferred inflows of resources(类似Segment)

>=10% all Government Funds OR Enterprise Funds,And

>=5% all Government Funds AND Enterprise Funds,

The general fund will always be a major fund

Internal service funds are not considered in the evaluation of major and nonmajor funds.

Reconciliation of Governmental Fund F/S to Government-wide F/S

Reconcile from fund balance to net position(GLAS + BARE)

Reconcile from net change in fund balances to the change in net position(GOES+BARE)

时点调整:GLAS+BARE

Governmental funds balance

Less:non-current Liability

Add:non-current Assets

Service(internal)fund net position

Basis of accounting

Accrued

Revenues and Expenses

时期调整:GOES+BARE

22

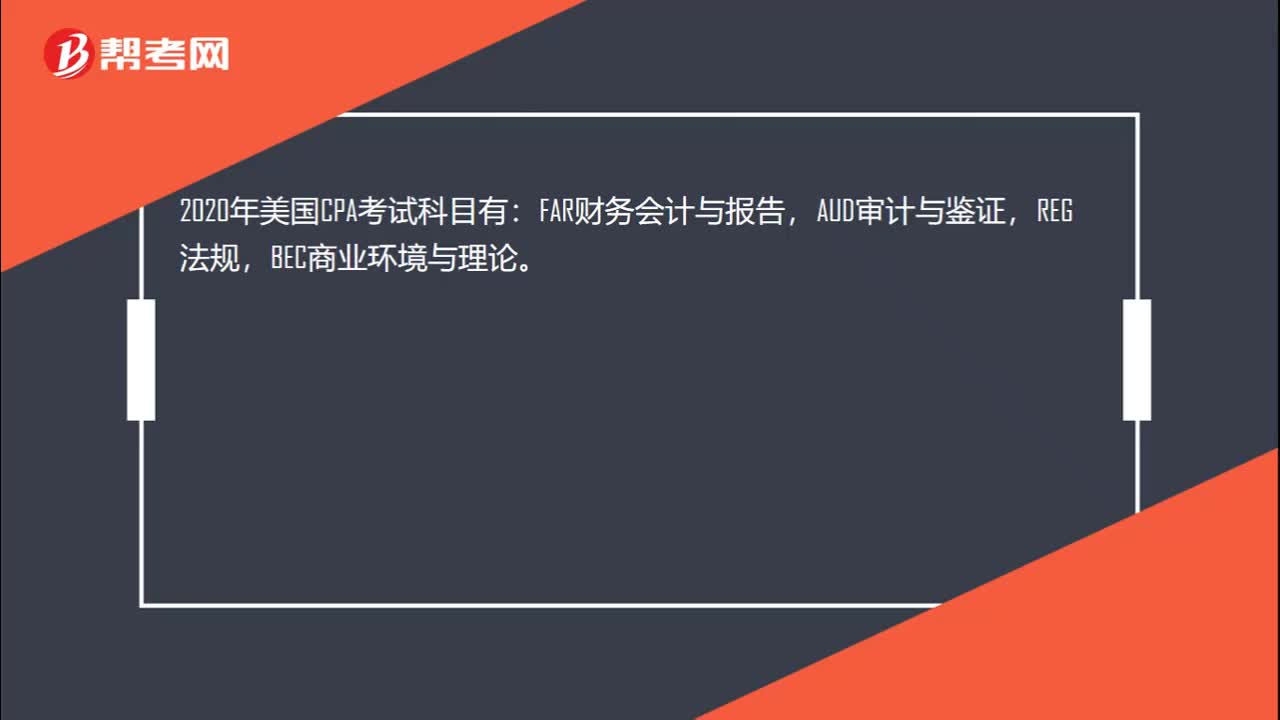

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

80

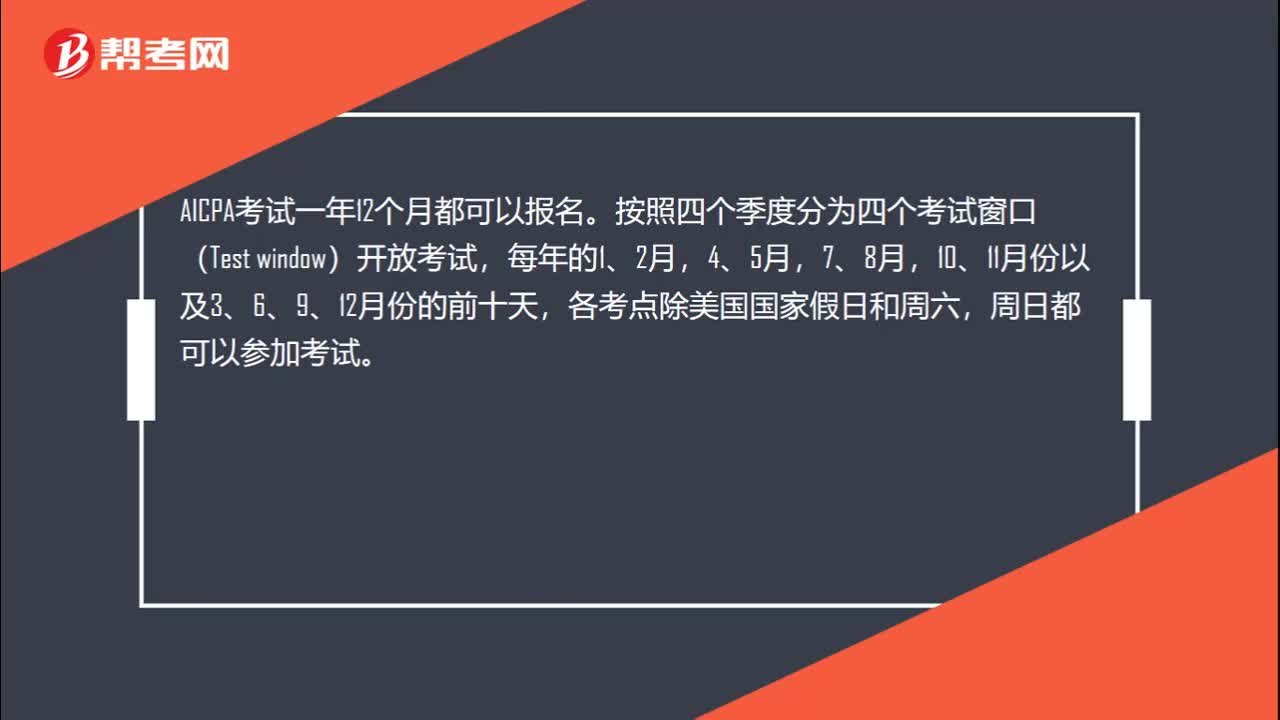

802020年美国CPA准考证打印时间延长了几个月?:2020年美国CPA准考证打印时间延长了几个月?NTS有效期在2020.4.1-2020.6.30期间到期的,NASBA会将NTS到期时间延长至2020.9.30。考生无需采取任何行动,也无需联系NASBA或您的州会计委员会。NASBA会在第一时间官方公布NTS及考试成绩完成延迟时间的更新。你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。

25

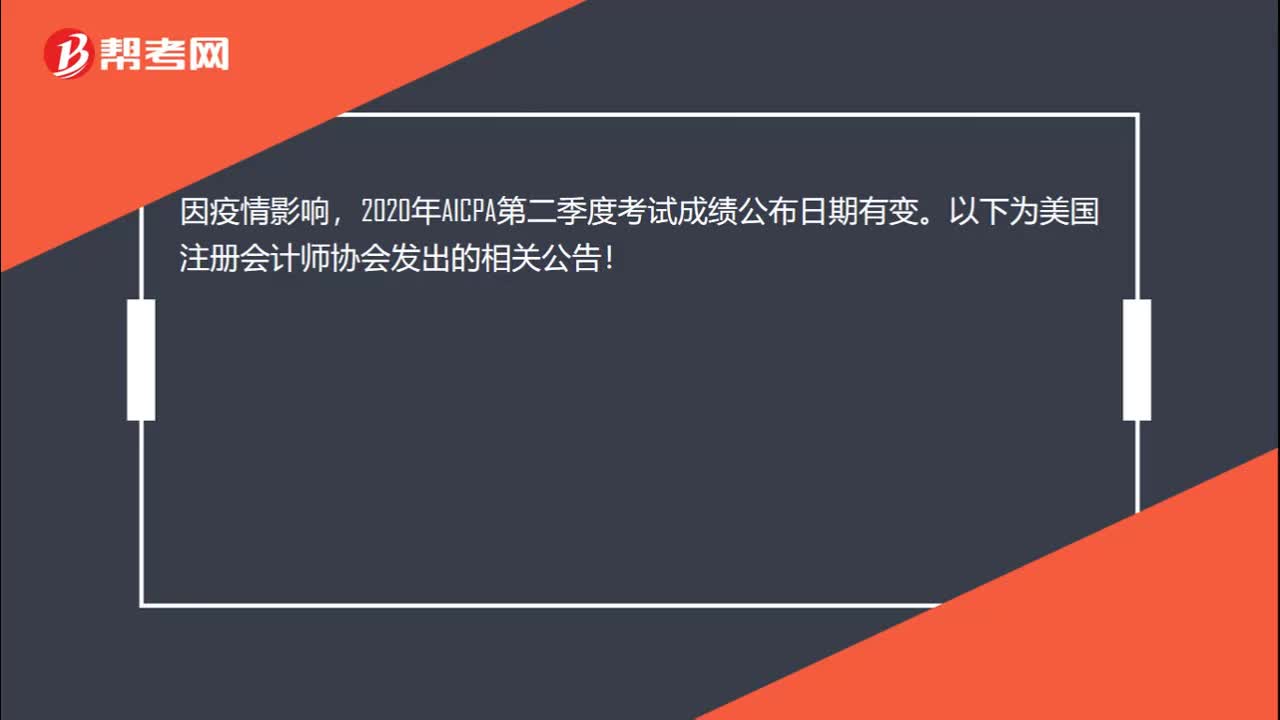

252020年美国注册会计师Q2考季成绩能查了吗?:2020年美国注册会计师Q2考季成绩能查了吗?因疫情影响,2020年AICPA第二季度考试成绩公布日期有变。以下为美国注册会计师协会发出的相关公告!

00:222020-05-21

01:202020-05-21

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料