下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Governmental accounting(Part B)

GASB 34 is the governmental reporting standards

Governmental reporting = Basic financial statements(F/S)+Required supplementary information(RSI)

F/S=government-wide financial statements+fund financial statements+notes

RSI=Management‘s discussion and analysis(MD&A)etc.

Two types of accountability focused by governmental reporting.

Operational accountability focus is to report the extent to which the government has met its operating objectives efficiently and effectively,using all resources available for that purpose,and the extent to which it can continue to meet its objectives for the future.

Fiscal accountability focus is to demonstrate that government entity‘s actions in the current period has complied with public decisions concerning the raising and spending of public funds in the shouirt-term.

The integrated approach requires financial accounting and disclosure to show operational(government-wide F/S)and fiscal(fund F/S)accountability individually and to show the relationship between operational and fiscal accountability through a reconciliation.

Required reporting for general purpose government units include:

Management‘s Discussion and Analysis(MD&A)

Government-wide F/S(Statement of Net Position+Statement of Activities)

Fund Financial Statements

Notes to Financial Statements

Required Supplementary Information(RSI)other than MD&A

Other supplementary Information

Government-wide F/S include “Statement of Net Position” +“Statement of Activities”

Governmental Funds F/S include “Balance Sheet”+“Statement of Revenues,Expenditures,and Changes in Fund Balances”

Proprietary Funds F/S include “Statement of Net Position”+“Statement of Revenues,Expenses,and Changes in Fund Net Position”+“Statement of Cash Flows”

Fiduciary Funds F/S include “Statement of Fiduciary Net Position”+“Statement of Changes in Fiduciary Net Position”

RSI include “Pension”+“Budgetary comparison schedules”+“Infrastructure information and assets using the modified approach”

Optional reporting-Comprehensive Annual Financial Report(CAFR)

CAFR=Introductory section+Required reporting+Statistical section.

Introductory section=letter of transmittal+Organizational chart+List of principal officers

Statistical section=10 years of selected financial data+10 years of economic data+other data

The financial reporting entity classification

1st tier Primary government Vs.Component(“SELF” test)

2nd tier Component unit‘s Blended presentation Vs. Discrete presentation(“SON” test)

A primary government consists of all organizations that make up the legal government entity.The primary government is considered the nucleus of the financial reporting entity.(联邦政府,州政府,县政府)

A component unit of a primary government is a legally separate organization for which the elected officials of the primary government are financially accountable.It may also be a separate organization,but its nature and the significance of its relationship with the primary government are such that exclusion of the unit‘s information would cause the primary government’s financial statements to be misleading or incomplete.(县教委, 县公安局)

If an unit meet ALL the three criteria(“Self”),then it is a primary government.

“Self”:Has a separately-elected governing body?

“Self”:Is legal separate?

“Self”:Is fiscally independent of other state and local governments?

If an unit NOT meet ALL the three criteria(“Self”),then it is a component unit.

If a component unit meet ANY the three criteria(“Son”),then it should use blended presentation(rare)。县办的信息披露

“Son”:The board of the primary government is same as the component unit?

“Son”:The component unit only serve the primary government(exclusively service)

“Son”:The organization does not qualify as a legal entity.

If an unit NOT meet Any the three criteria(“Son”),then it should use discrete presentation(most often)。县教委的信息披露

22

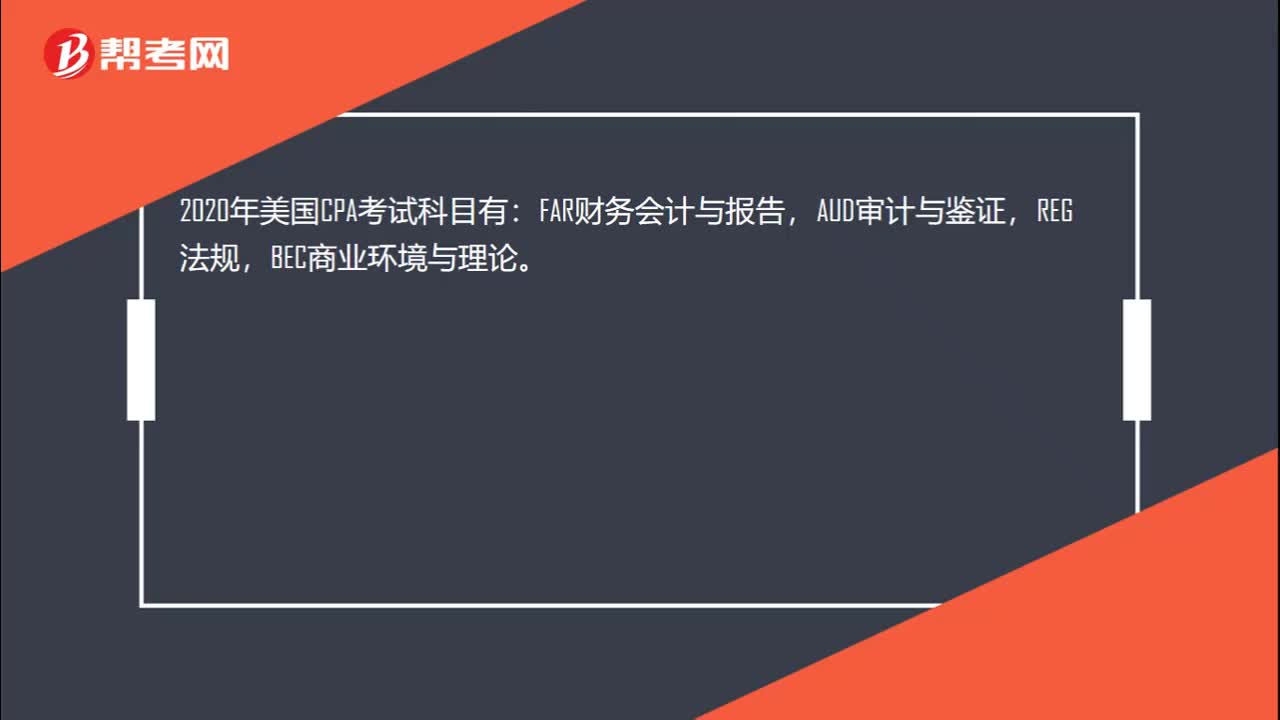

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

80

802020年美国CPA准考证打印时间延长了几个月?:2020年美国CPA准考证打印时间延长了几个月?NTS有效期在2020.4.1-2020.6.30期间到期的,NASBA会将NTS到期时间延长至2020.9.30。考生无需采取任何行动,也无需联系NASBA或您的州会计委员会。NASBA会在第一时间官方公布NTS及考试成绩完成延迟时间的更新。你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。

25

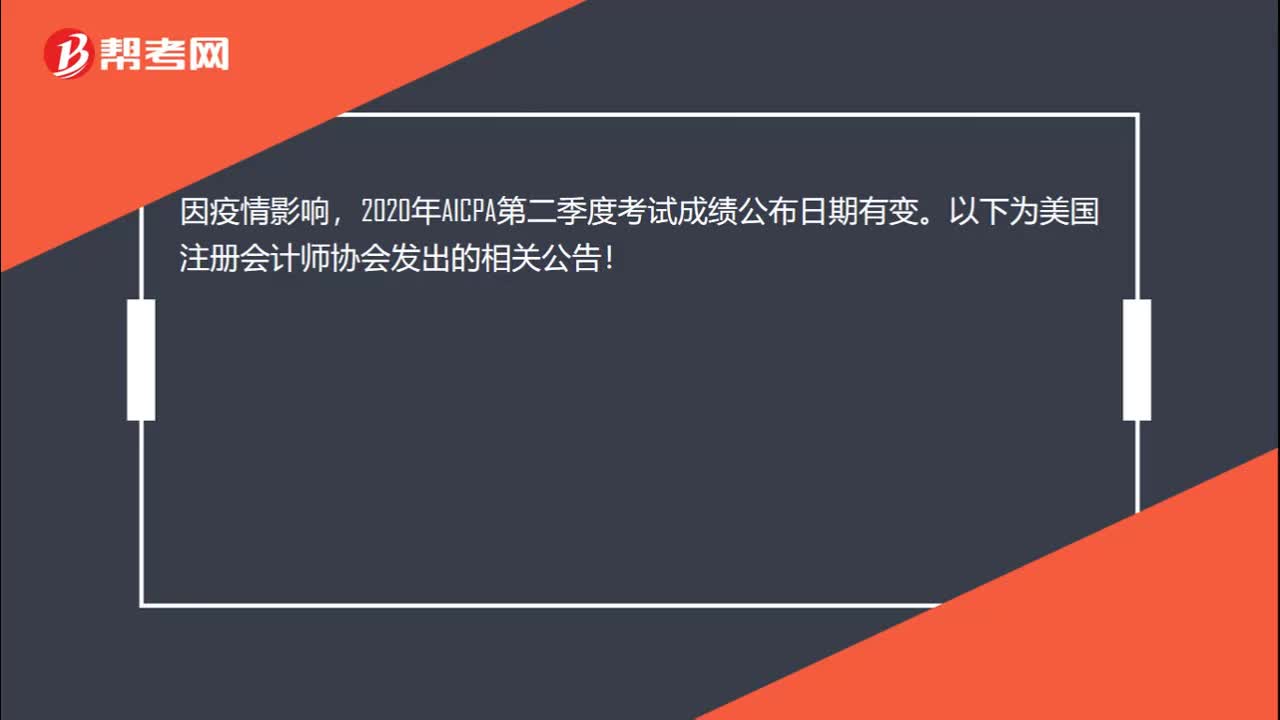

252020年美国注册会计师Q2考季成绩能查了吗?:2020年美国注册会计师Q2考季成绩能查了吗?因疫情影响,2020年AICPA第二季度考试成绩公布日期有变。以下为美国注册会计师协会发出的相关公告!

00:222020-05-21

01:202020-05-21

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料