下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Blended presentation is preferred

Combines financial information with the primary government

Financial information of the component unit is not presented in separate columns.

Discrete presentation is preferred

Displays component units in separate columns

F/S of the reporting entity should provide an overview of the entity based on financial accountability.

Most component units should use discrete presentation.

Reporting Not-for-Profit entities as a Component Unit of Government

Not-for-Profit organizations that provide ongoing support to a primary government or to a component unit of that primary government may also be a component unit of the primary government. E.g. private foundations associated with state universities or public health care facilities.

Criteria for Discrete Presentation–meet ALL of ABS(防锁死刹车系统/树脂)

Access:The primary government must have access to the resources of the private not-for-profit organization

Benefit:The private organization must be for the near exclusive benefit of the primary government.

Significance:Resources of the private not-for-profit organization must be significant to the primary government.

If a legally separate and tax-exempt organizations meet ALL of the “ABS”,it should be reported as a discrete component.

Governmental reporting summary(F9-10)is very important.Please scrutinize it.

Required reporting for general purpose government units include:

Management‘s Discussion and Analysis(MD&A)

Government-wide F/S(Statement of Net Position+Statement of Activities)

Fund Financial Statements

Notes to Financial Statements

Required Supplementary Information(RSI)other than MD&A

Other supplementary Information

Management‘s Discussion and Analysis(MD&A)is a narrative that provides a brief,objective,and easily readable analysis of the government’s financial activities based upon currently known facts,decisions,and conditions.The following should be included(F9-11):

Description of the F/S

Identity of the primary government and discrete component units

Economic conditions and outlook

Major initiatives

Government-wide Financial Statement(GW F/S)use the economic resources measurement focus and the full accrual basis of accounting.

GW F/S includes all assets and liabilities over which a government has control or responsibility.

Therefore,fiduciary funds are excluded,but governmental funds,proprietary funds,and the component units are included.

GW F/S include “Statement of Net Position” and “Statement of Activities”

Statement of Net Position–a consolidated statement

Net Position=Assets–Liabilities

Net Position=Net investment in capital assets+Restricted+Unrestricted

GASB 34 reporting model requires that capital assets,including infrastructure assets,be included in the government-wide F/S.

22

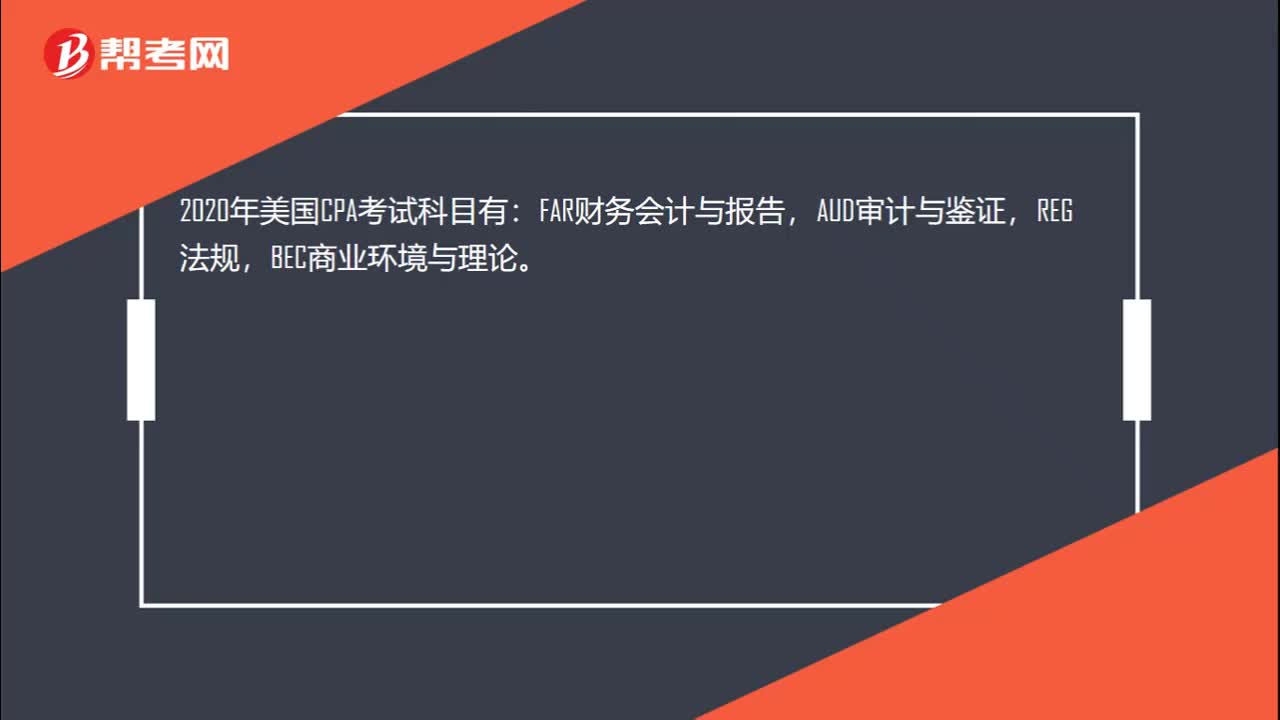

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

80

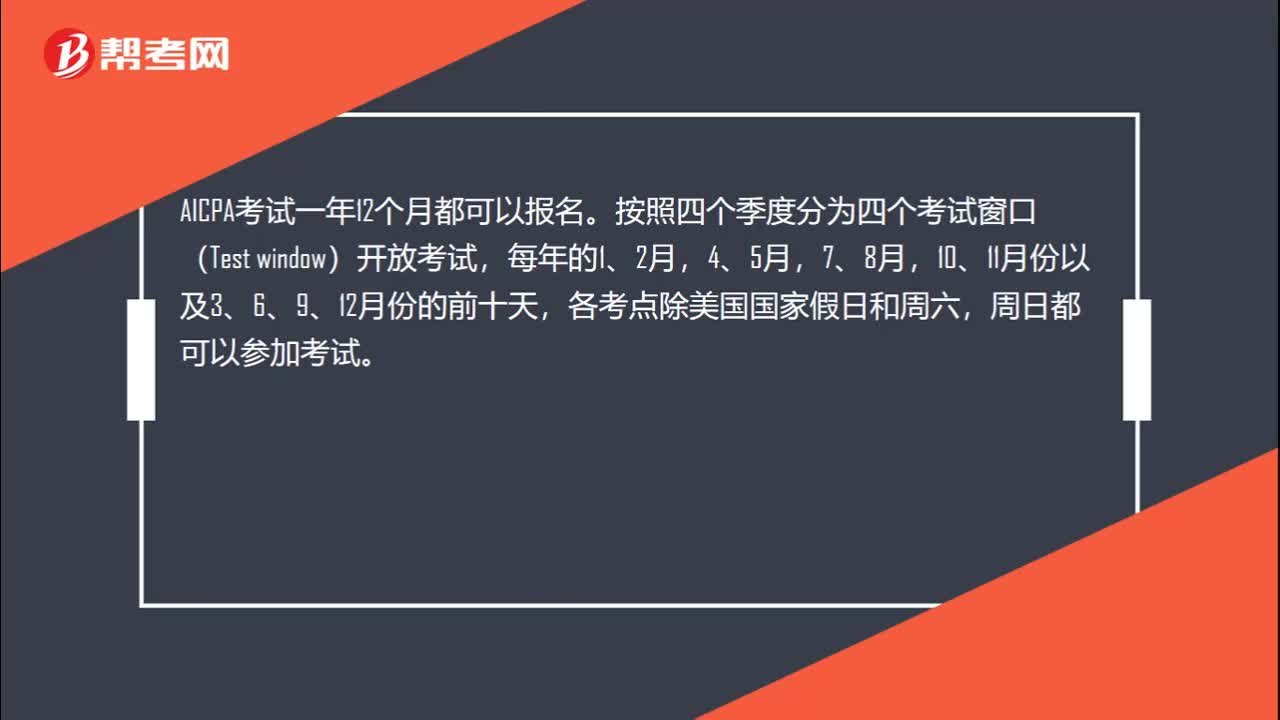

802020年美国CPA准考证打印时间延长了几个月?:2020年美国CPA准考证打印时间延长了几个月?NTS有效期在2020.4.1-2020.6.30期间到期的,NASBA会将NTS到期时间延长至2020.9.30。考生无需采取任何行动,也无需联系NASBA或您的州会计委员会。NASBA会在第一时间官方公布NTS及考试成绩完成延迟时间的更新。你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。

25

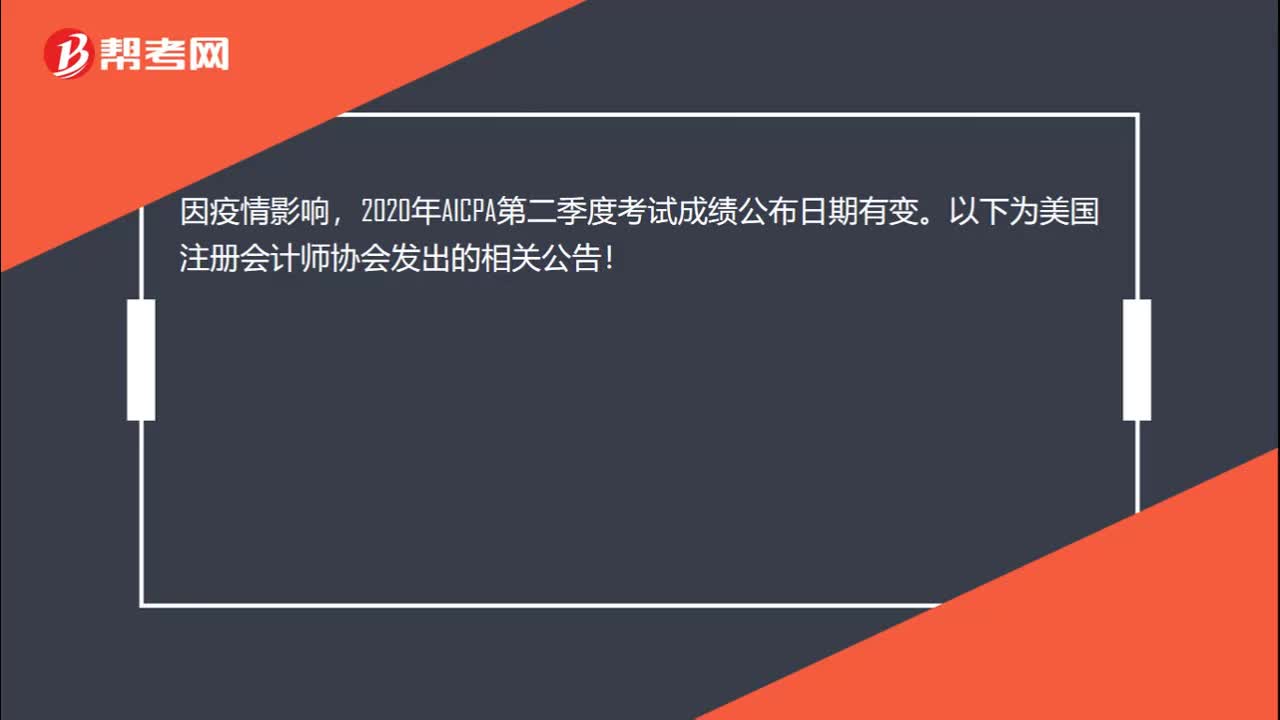

252020年美国注册会计师Q2考季成绩能查了吗?:2020年美国注册会计师Q2考季成绩能查了吗?因疫情影响,2020年AICPA第二季度考试成绩公布日期有变。以下为美国注册会计师协会发出的相关公告!

00:222020-05-21

01:202020-05-21

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料