当前位置: 首页ACCA考试财务会计(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

各位小伙伴注意了,今天帮考网为大家分享2020年ACCA考试《财务会计》备考考点(4),供大家参考,希望对大家有所帮助。

THE CONTROL ENVIRONMENT OF A COMPANY (二)

One Communication and enforcement of integrity and ethical values

Many companies have high values and seek to promote honesty and integrity among their employees on a day-to-day basis. Clearly, if it is evident those such values do exist and are communicated effectively to employees and enforced, this will have the effect of increasing confidence in the design, administration and monitoring of controls – leading to a reduced risk of material misstatement in a company’s financial statements. For example, where a company adopts comprehensive anti-bribery and corruption policies and procedures with regard to contract tendering, and has formal employee notification and checking practices in this regard, it follows that there is reduced risk of material misstatement due to the omission of provisions for fines for the non-compliance with relevant laws and regulations. Alternatively, the existence in a company of comprehensive and ethical procedures with regard to the granting of credit facilities to customers and the pursuance of payment of for goods and services supplied, together with regular supervisory control in this respect, is likely to lead to increased audit confidence in the trade receivables area. This is because the existence of a system allowing goods and services to be a supplied on credit to customers provides the opportunity for fraud to be perpetrated against the company by employees and customers, particularly if controls are deficient in terms of their design or implementation.

Two Commitment to competence

Competence is the knowledge and skills necessary to accomplish tasks that define the individual’s job. It is self-evident that if individual employees are tasked with carrying out duties that are beyond their competence levels, then desired objectives are unlikely to be met. For example, there is an increased probability that the objective of avoiding material misstatement in a set of complex financial statements will not be met if prepared by an inexperienced company accountant. This is simply due to the inexperience (translating to a lower competence level) of the accountant. From this, it follows that the auditor will have increased confidence in internal control relevant to the audit, where management have taken measures to ensure employees who participate in internal control are competent to carry out relevant tasks effectively. Measures taken by management in this regard can cover a range of activity including for example, rigorous technical and aptitude testing at the employee recruitment stage and in-house or external training courses and mentoring from colleagues that are more senior.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

80

80ACCA考试难度大吗?:ACCA考试难度大吗?ACCA考试的难度是以英国大学学位考试的难度为标准,第一(f1-f3)、第二部分(f4-f9)的难度分别相当于学士学位高年级课程的考试难度,第三部分p阶段的考试相当于硕士学位最后阶段的考试。第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。第二部分的考试除了本门课程的内容之外。

56

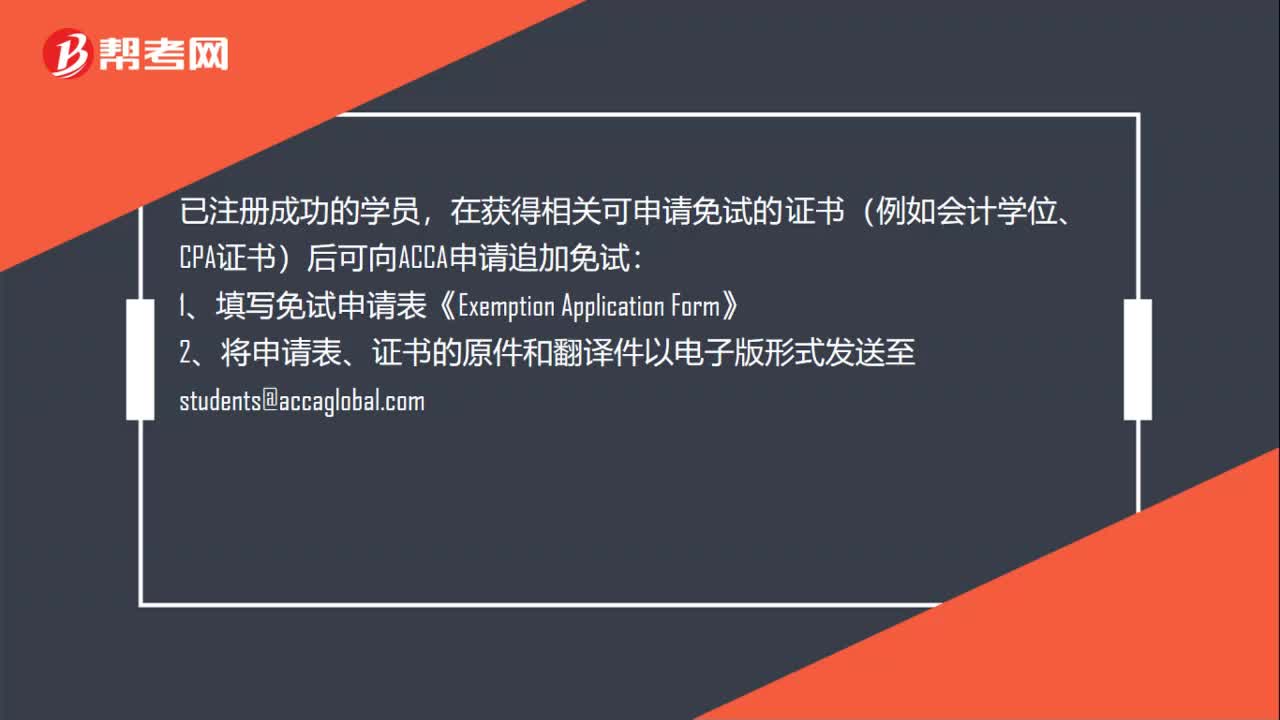

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

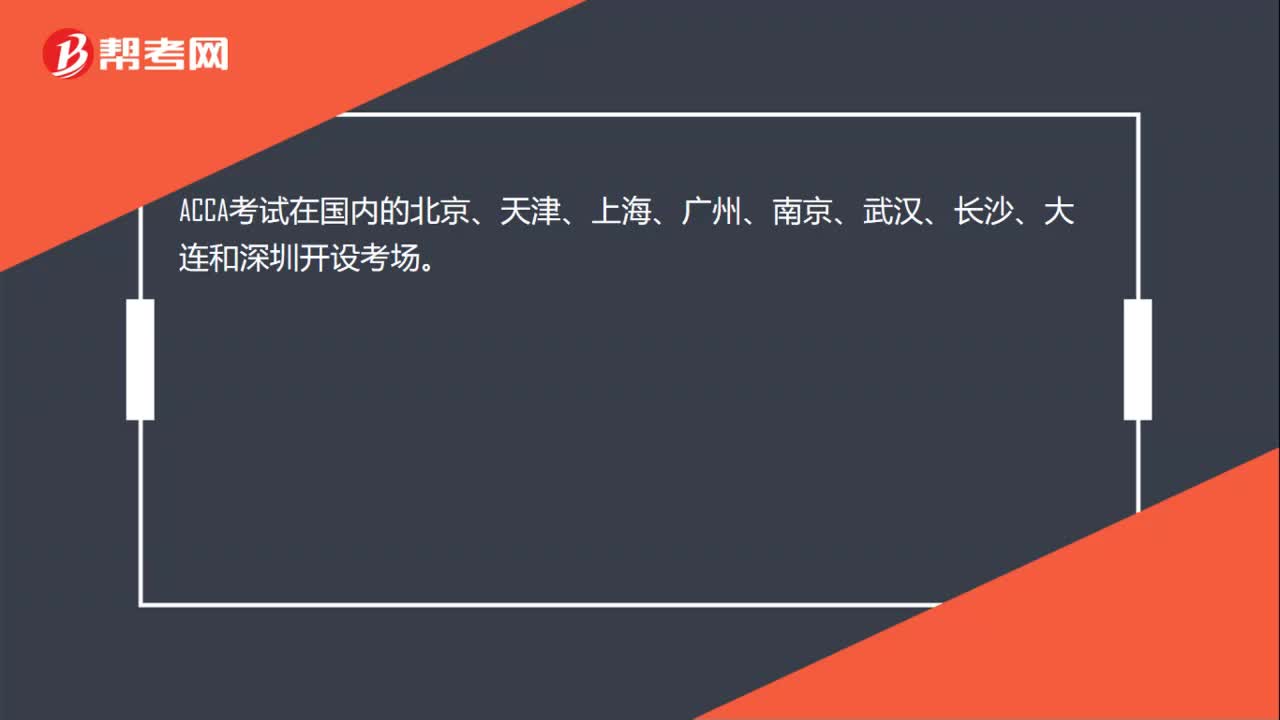

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料