当前位置: 首页ACCA考试财务会计(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

今日帮考网为大家分享2020年ACCA考试《财务会计》备考考点(3),供大家参考,希望对大家有所帮助,查看更多备考内容请关注帮考网ACCA考试频道。

THE CONTROL ENVIRONMENT OF A COMPANY (三)

Three Participation by those charged with governance

The directors of a limited liability/limited company are charged with the company’s governance. As such, they are responsible for overseeing the strategic direction of the company and its obligations related to its accountability – for example, to governments, shareholders and to society in general. In particular, in most jurisdictions the company’s directors are responsible for the preparation of its financial statements. Given the influence that the actions of directors have on a company’s internal control, the extent of their day-to-day active involvement in the company’s operations has a pervasive effect on the internal control of the company.

The extent to which directors do get involved will, to some extent, depend on legislation or codes of practice setting out guidance for best practice in given jurisdictions. For example, the UK Corporate Governance Code (with which companies listed on the London Stock Exchange should comply) sets out standards of good practice, including those pertaining to board leadership and effectiveness. Notwithstanding legislation and codes of practice, the extent of each director’s participation is largely influenced by the nature of their professional discipline and their individual perspective about how they should carry out their respective roles.

Some may see themselves as micromanagers, while others will trust subordinates to carry out defined duties with minimal interference. Frequently, directors will be very experienced and adopt an arms-length approach to getting involved in operational tasks. However, they may insist on monitoring activity by way of receipt of formal narrative reports. Other directors may adopt a more casual (but equally thorough!) ‘Working alongside subordinates’ approach as a method of monitoring activities.

All of the variables mentioned above with regard to director involvement, should be important considerations of an auditor as part of the process of ascertaining the extent of internal control in the company and in assessing its effectiveness.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

25

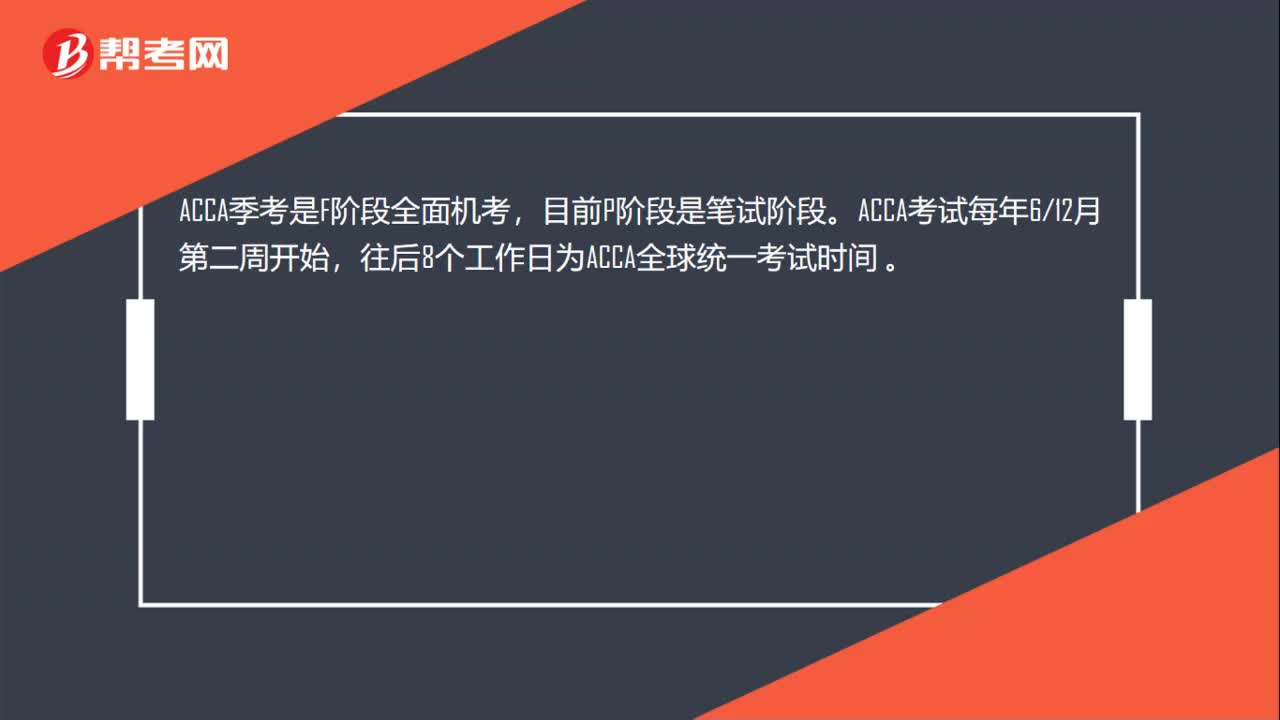

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

56

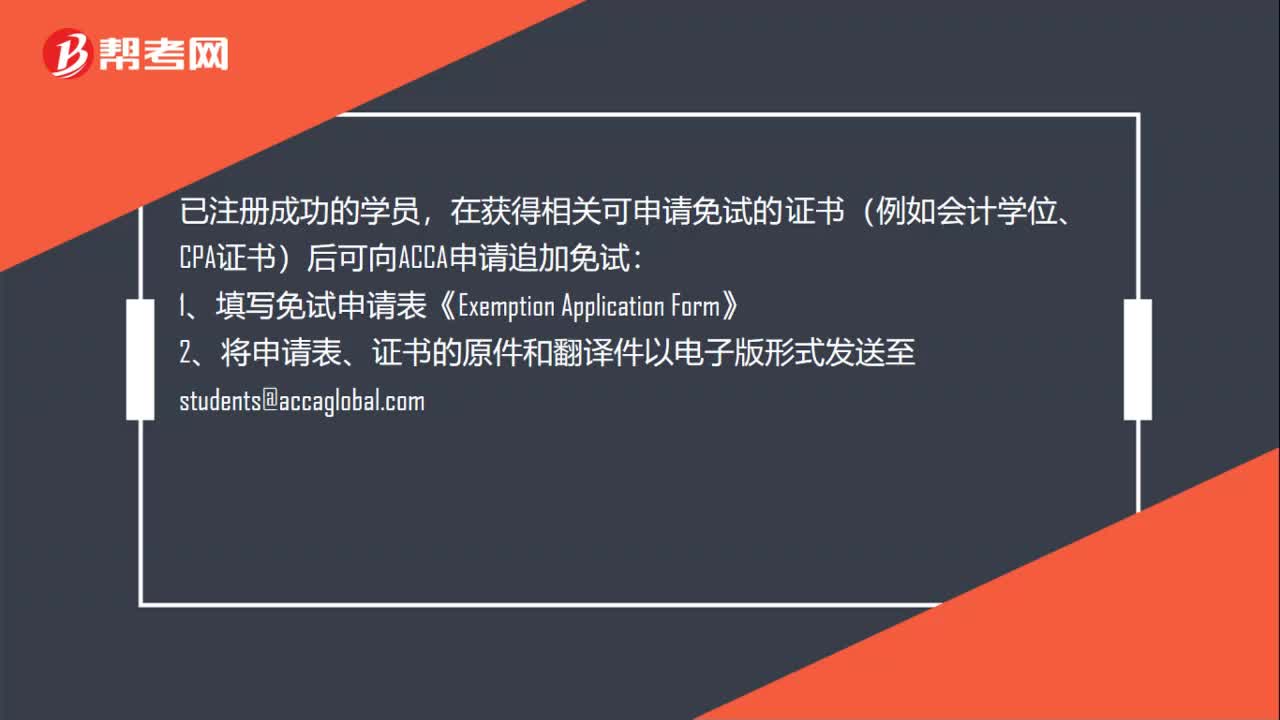

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

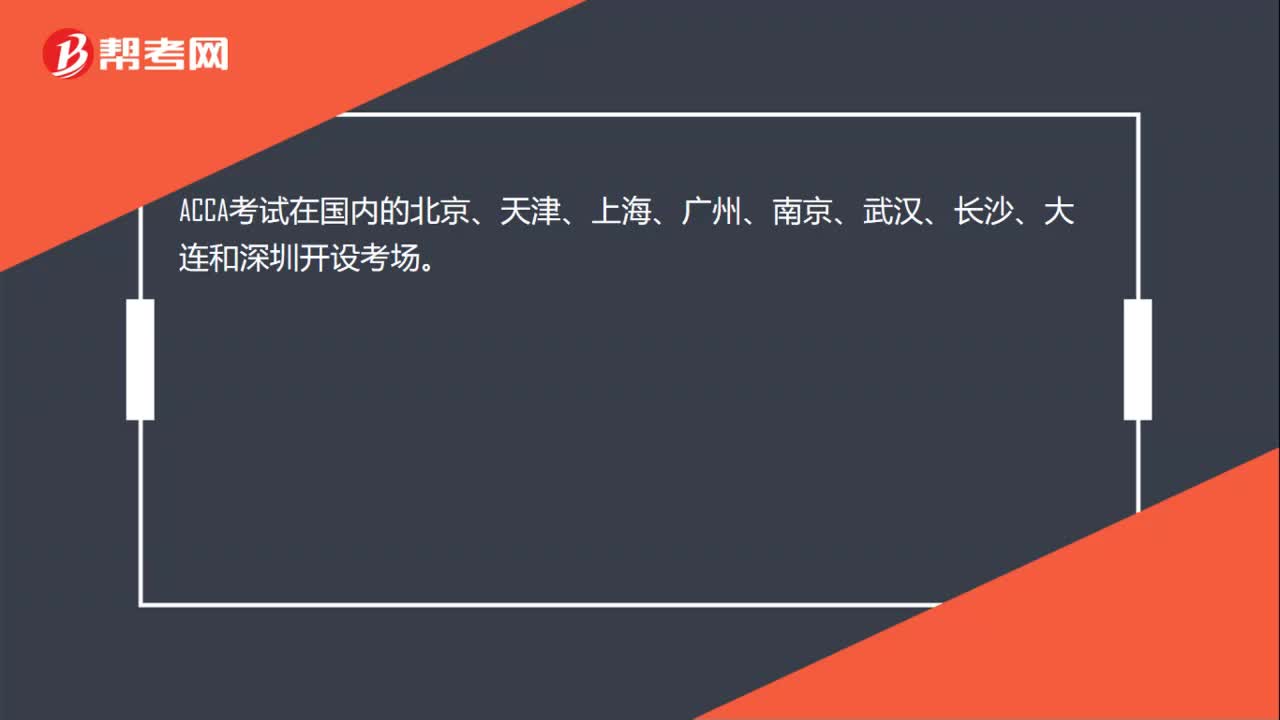

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料