当前位置: 首页ACCA考试财务会计(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

距离ACCA考试还有45天的时间,各位小伙伴备考的如何了啊,今日帮考网为大家分享“2020年ACCA考试《财务会计》备考考点(2)”的相关知识点,一起过来复习巩固一下吧。

THE CONTROL ENVIRONMENT OF A COMPANY (四)

Four Management’s philosophy and operating style

A company’s board of directors will comprise of individuals each with a different mind – set as to philosophy and operating style, manifested in characteristics such as their:

Approach to taking and managing business risk

Attitudes and actions toward financial reporting

Attitudes toward information processing and accounting and functions personnel.

Each of the above characteristics underlie a company’s control environment and it is crucial for an auditor to have an understanding of them. Dealing with each in turn:

Approach to taking and managing business risk. Business risk is the risk inherent in a company because of its day-to-day operations and it comprises several components. The first of these is financial risk – for example, the risk that the company may have insufficient cash flow to continue in operation. The second component is operational risk – for example, the risk that the company’s product lines may decline in popularity leading to a sharp decline in sales and profitability. The final component of business risk is compliance risk – for example, the risk that the company may be in breach of health and safety regulations, leading to the possibility of hefty fines or even the closedown of operational activity. Candidates should be aware that a risk-based approach to an audit requires the identification and assessment of inherent risk factors and then of the control risk pertaining to these, in order to determine the risk of material misstatement, prior to carrying out substantive procedures. By adopting a top-down approach to the audit and first identifying business risks, auditors should be able to identify the associated inherent risks arising. They can then progress through the audit using the audit risk model (audit risk = the risk of material misstatement x detection risk) to determine the amount of detailed testing required in each area of the financial statements. To illustrate this approach, referring to the compliance risk example above, an inherent risk arising from the risk of a breach of health and safety regulations. Therefore, there is a risk that the company’s liabilities may be understated due to the omission of a provision required in the financial statements, in respect of a fine for a non-compliance.

The directors’ approach to taking and managing business risk has obvious ramifications on a company’s financial statements, and the auditor should be aware of the various factors that influence directors in this area, and of applicable controls in place. It is often the case that a newly established company with young entrepreneurial directors and a flat management structure will have a more liberal approach to taking and managing business risk than a well-established company will with more experienced directors, and a steep hierarchical management structure.

Consequently, it is likely that there would be a lower level of a risk of material misstatement in the financial statements of the latter company. Attitude and actions toward financial reporting. Financial Reporting Standards exist to help facilitate fairness, consistency and transparency of financial reporting. However, some determinants of profitability such as the measure of depreciation, the valuation of inventory or the amount of a provision remain open to the subjective judgment of management. Consequently, the auditor needs to gain an understanding of directors’ attitudes and actions to financial reporting issues and then make a judgment as to the extent of reliance that can be placed upon these. It may be that a company that is struggling in a faltering economy, and in another driven by a culture to report increasing profits, there is a tendency to adopt aggressive (as opposed to conservative) accounting principles, in order to meet profit expectations. Clearly, on such audit engagements it is important for the auditor to remain resolute in exercising appropriate levels of professional sceptics throughout.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

80

80ACCA考试难度大吗?:ACCA考试难度大吗?ACCA考试的难度是以英国大学学位考试的难度为标准,第一(f1-f3)、第二部分(f4-f9)的难度分别相当于学士学位高年级课程的考试难度,第三部分p阶段的考试相当于硕士学位最后阶段的考试。第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。第二部分的考试除了本门课程的内容之外。

56

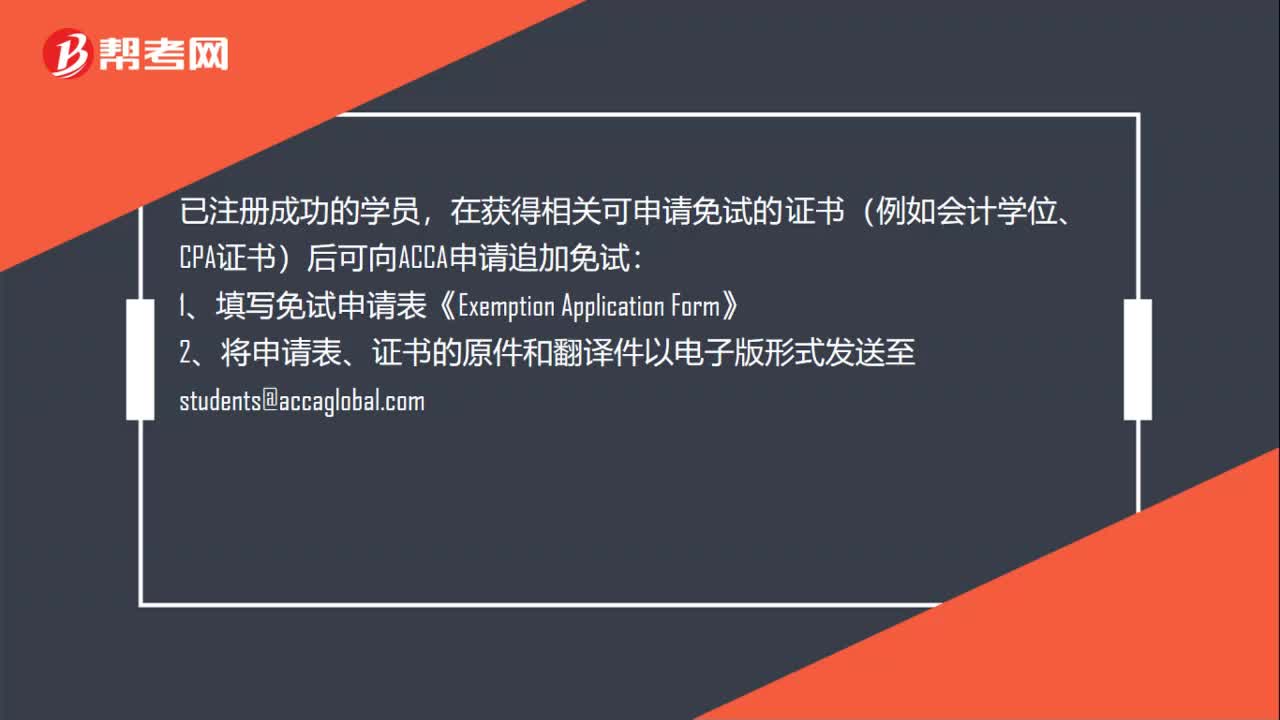

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

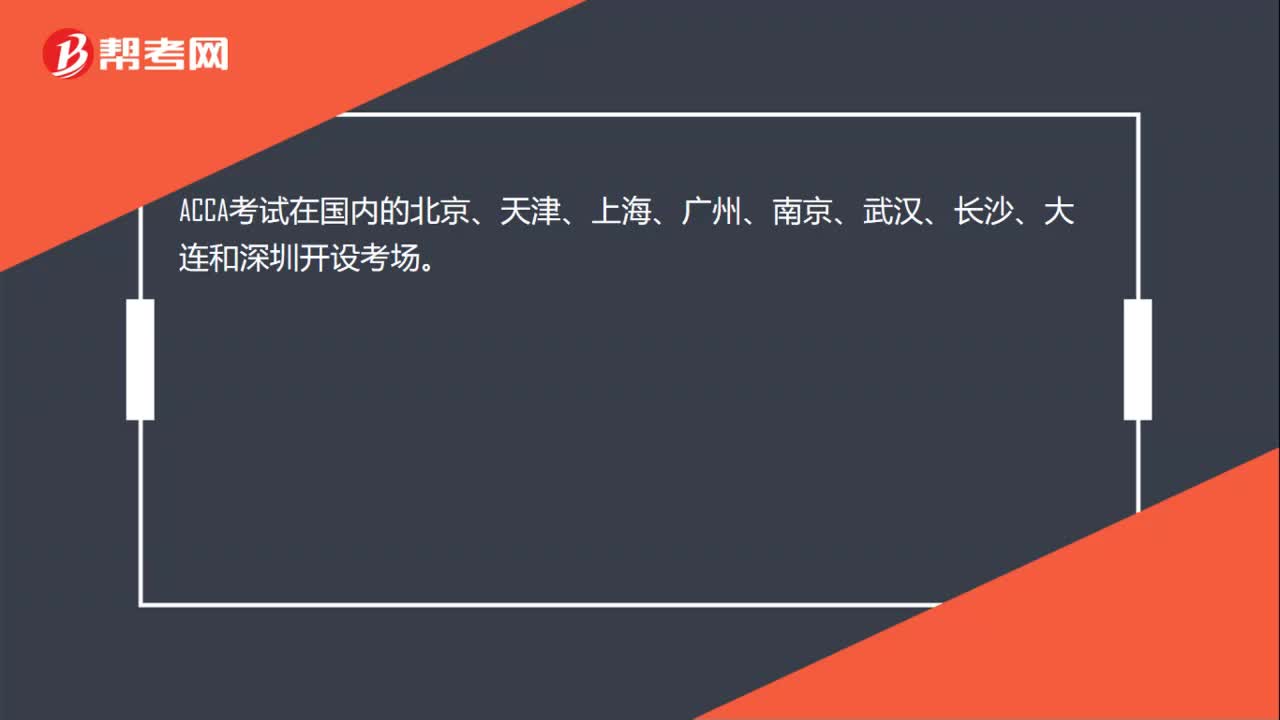

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料