下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

ACCA考试《财务会计》备考考点,有想要了解的小伙伴吗?下面帮考就带领大家一起来来了解看看,想要了解的小伙伴赶紧来围观吧。

THE CONTROL ENVIRONMENT OF A COMPANY

5 Organisational structure

ISA 315 describes a company’s organisational structure as being ‘the framework within which an entity’s activities for achieving its objectives are planned, executed, controlled and reviewed’. The appendix to the ISA then explains ‘that the appropriateness of an entity’s organisational structure depends, in part, on its size and the nature of its activities’. It follows from this that an international consulting company with offices and operations in several countries has different priorities in terms of organisational structure to a national car sales company with several offices and a number of sales branches in a single country. Similarly, the organisational structure deemed suitable for such a car sales company would not be appropriate for a single site manufacturing company. Generally, an auditor may reasonably expect there to be a positive correlation between the level of inherent risk and the size and complexity of a company’s operations. In assessing, the level of the risk of material misstatement the auditor should consider as to whether the company’s organisational structure in terms of authority, responsibility and lines of reporting meet desired objectives.

6 Assignment of authority and responsibility

Normally, the larger a company’s scale of operations, then the larger the size of the workforce and, inevitably, the larger the amount of assignment of authority and responsibility that is required. Consequently, companies need to deal not only with ensuring that appropriate levels of authority and responsibility are assigned to appropriately qualified and experienced individuals. They also need to ensure that adequate reporting relationships and authorisation hierarchies are in place.

Additionally, individuals need to be properly resourced and made fully aware of their responsibilities and of how their actions interrelate with the actions of others and contribute to the objectives of the company. If a company is not successful in meeting each of these needs, then there is an increased probability of ineffective decisions, errors and oversights by employees leading to an increased risk of material misstatement in its financial statements. For example, where a wages clerk is authorised to process the wages payroll and is then assigned the (inappropriate!) authority to enter new employee details into the wages master file.

以上是关于ACCA考试《财务会计》备考考点的内容,小伙伴们都清楚了吗?如果大家对于ACCA考试还有其他问题,可以多多关注帮考网,我们将继续为大家答疑解惑。

44

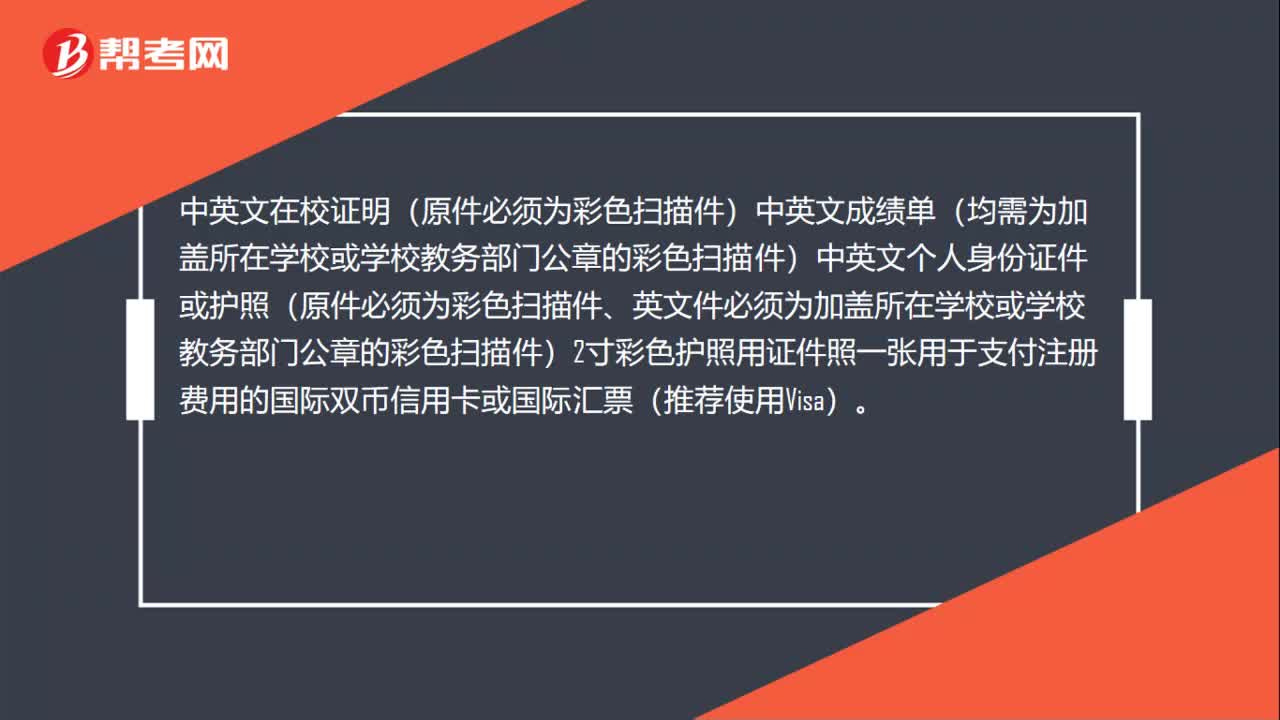

44报考ACCA需要准备什么?:中英文在校证明(原件必须为彩色扫描件)中英文成绩单(均需为加盖所在学校或学校教务部门公章的彩色扫描件)中英文个人身份证件或护照(原件必须为彩色扫描件、英文件必须为加盖所在学校或学校教务部门公章的彩色扫描件)2寸彩色护照用证件照一张用于支付注册费用的国际双币信用卡或国际汇票(推荐使用Visa)。

56

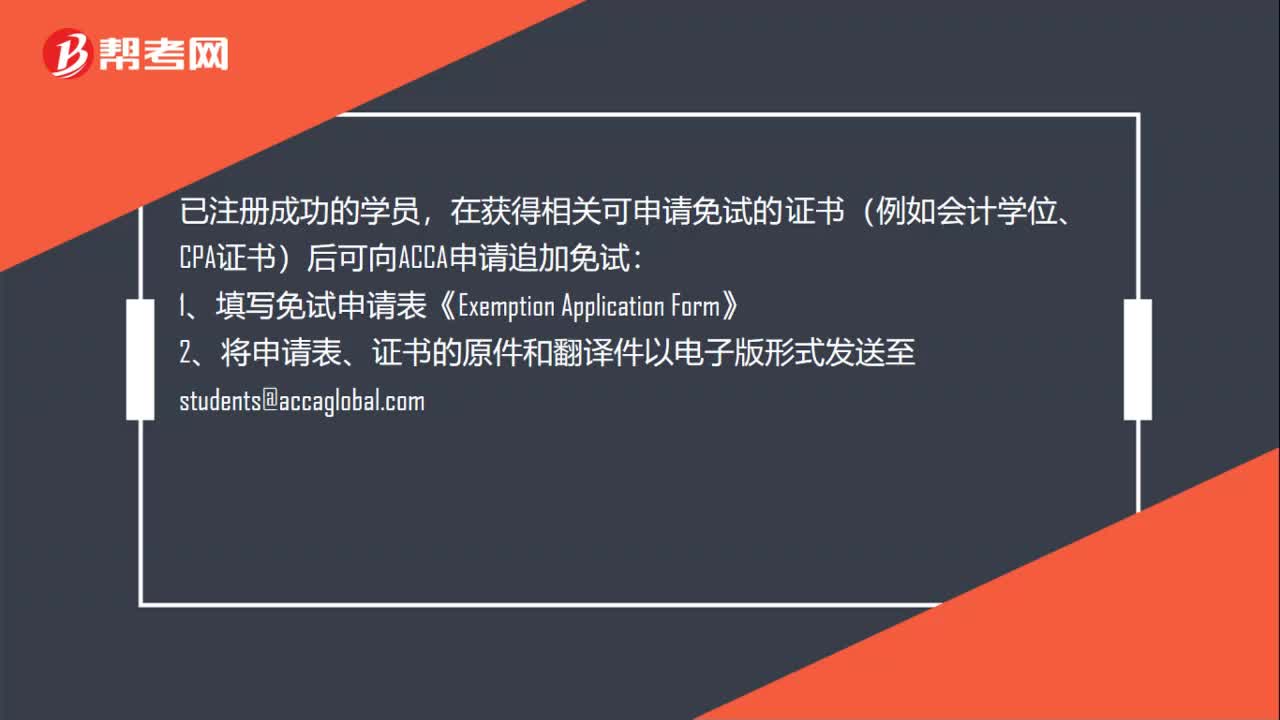

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

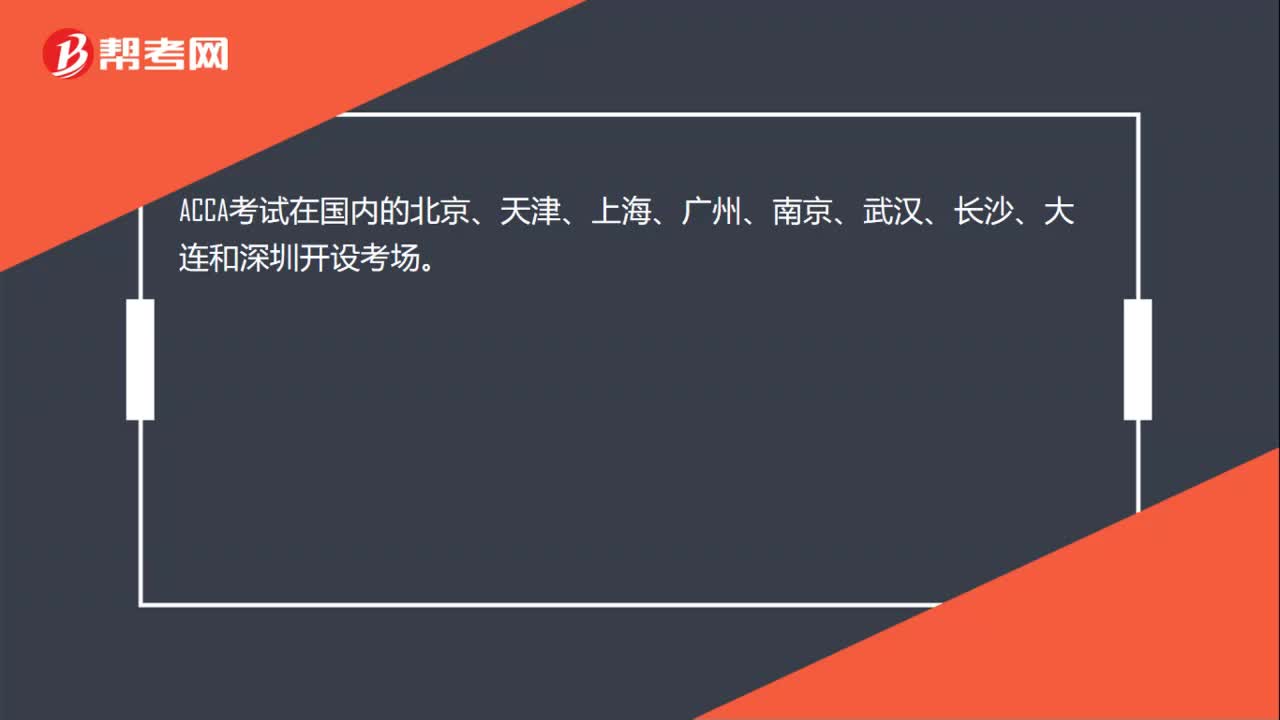

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料