下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

众所周知,USCPA考试是全英文作答,所以对于很多报考美国注册会计师的考生而言,尽快熟悉全英文的答题环境也是非常重要的,为了帮助大家更好的备考,帮考网为大家分享了美国注册会计师USCPA考试FAR财务会计与报告练习试题,详情如下:

1. Which of the following methods of determining bad debt expense does not properly match expense against revenue?

a.Charging bad debts with a percentage of accounts receivable under the allowance method.

b.Charging bad debts as accounts are written off as uncollectible.

c.Charging bad debts with an amount derived from aging accounts receivable under the allowance method.

d.Charging bad debts with a percentage of sales under the allowance method.

答案:B

2.According to the FASB and IASB conceptual frameworks, useful information must exhibit the fundamental qualitative characteristics of:

a. Neutrality and verifiability.

b. Comparability and materiality.

c. Faithful representation and relevance.

d. Understandability and timeliness.

答案:C

3.What is the underlying concept governing the recording of gain contingencies?

a. Relevance.

b. Consistency.

c. Reliability.

d. Conservatism.

答案:D

4.According to the FASB conceptual framework, which of the following attributes would not be used to measure inventory?

a.Present value of future cash flows.

b.Replacement cost.

c.Historical cost.

d.Net realizable value.

答案:A

5.According to the FASB and IASB conceptual frameworks, the objective of general purpose financial reporting is to:

a.Report on how effectively and efficiently management has used the entity\'s resources.

b.Provide financial information that is useful to primary users.

c.Comply with the need forconservatism.

d.Comply with generally accepted accounting principles.

答案:B

6.If the payment of employees\' compensation forfuture absences is probable, the amount can be reasonably estimated, and the obligation relates to rights that accumulate, the compensation should be:

a. Accrued if attributable to employees\' services already rendered.

b. Accrued if attributable to employees\' services not already rendered.

c. Recognized when paid.

d. Accrued if attributable to employees\' services whether already rendered or not.

答案:A

7.According to the FASB and IASB conceptual frameworks, the objective of general purpose financial reporting is to:

a.Report on how effectively and efficiently management has used the entity\'s resources.

b.Provide financial information that is useful to primary users.

c.Comply with the need forconservatism.

d.Comply with generally accepted accounting principles.

答案:B

8.If the payment of employees\' compensation forfuture absences is probable, the amount can be reasonably estimated, and the obligation relates to rights that accumulate, the compensation should be:

a. Accrued if attributable to employees\' services already rendered.

b. Accrued if attributable to employees\' services not already rendered.

c. Recognized when paid.

d. Accrued if attributable to employees\' services whether already rendered or not.

答案:A

9.Taylor, an unmarried taxpayer, had $90,000 in adjusted gross income forthe current year. During the current year, Taylordonated land to a church and made no other contributions. Taylorpurchased the land 15 years ago as an investment for$14,000. The land\'s fair market value was $25,000 on the day of the donation. What is the maximum amount of charitable contribution that Taylormay deduct as an itemized deduction forthe land donation forthe current year?

a. $11,000

b. $25,000

c. $0

d. $14,000

答案:B

10.On January 2, Year 3, to better reflect the variable use of its only machine, Holly, Inc. elected to change its method of depreciation from the straight-line method to the units of production method. The original cost of the machine on January 2, Year 1, was $50,000, and its estimated life was 10 years. Holly estimates that the machine\'s total life is 50,000 machine hours. Machine hours usage was 8,500 during Year 2 and 3,500 during Year 1.

Holly\'s income tax rate is 30%. Holly should report the accounting change in its Year 3 financial statements as a(n):

a. The correct treatment is not provided in any of the answer choices.

b. Adjustment to beginning retained earnings of $2,000.

c. Cumulative effect of a change in accounting principle of $1,400 in its income statement.

d. Cumulative effect of a change in accounting principle of $2,000 in its income statement.

答案:A

以上就是今天分享的全部内容了,希望本文对各位有所帮助,预祝各位取得满意的成绩,如需了解更多相关内容,请关注帮考网!

86

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

30

302020年AICPA怎么报考?:2020年AICPA怎么报考?AICPA报考流程如下:1.学历预评估。2. 学分评估,确认报考州。3.学历认证。4.补学分。5.申请NTS。6.预约考位。7. 安排行程。8.申请执照。

42

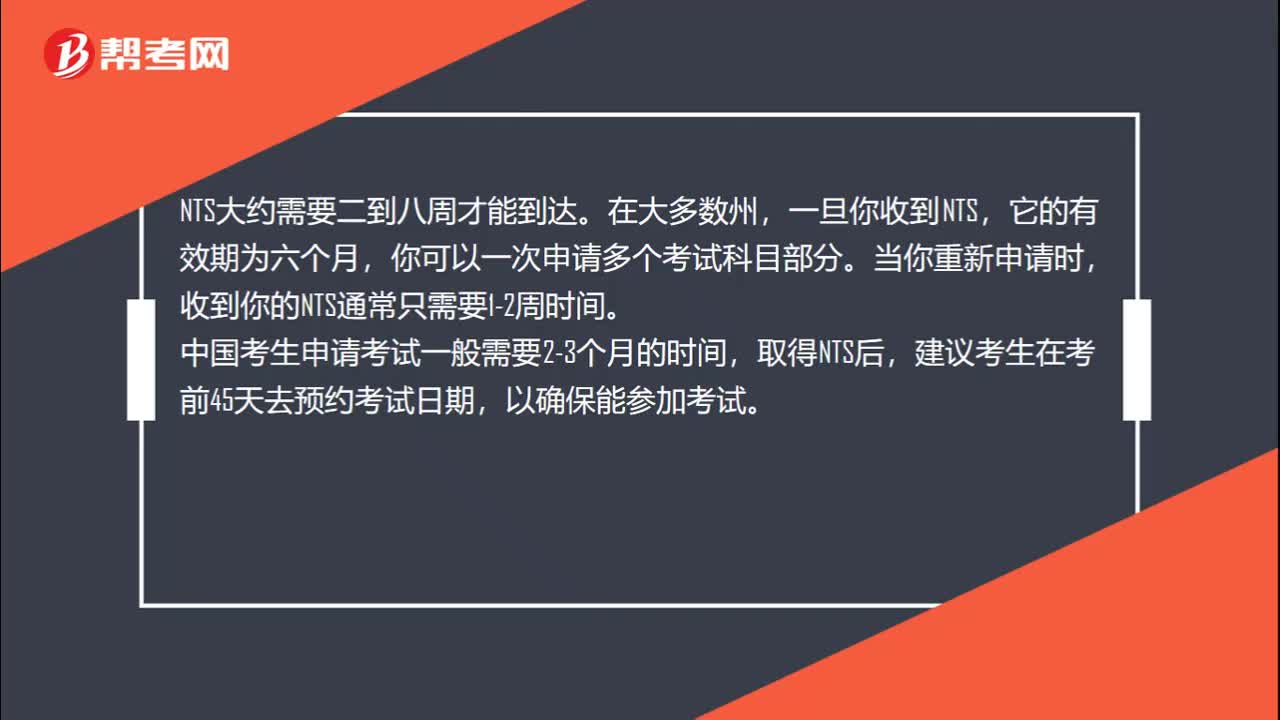

422020年AICPA考试预约考试后多久收到NTS准考证?:2020年AICPA考试预约考试后多久收到NTS准考证?NTS大约需要二到八周才能到达。在大多数州,一旦你收到NTS,它的有效期为六个月,你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。中国考生申请考试一般需要2-3个月的时间,取得NTS后,建议考生在考前45天去预约考试日期,以确保能参加考试。

00:22

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料