下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

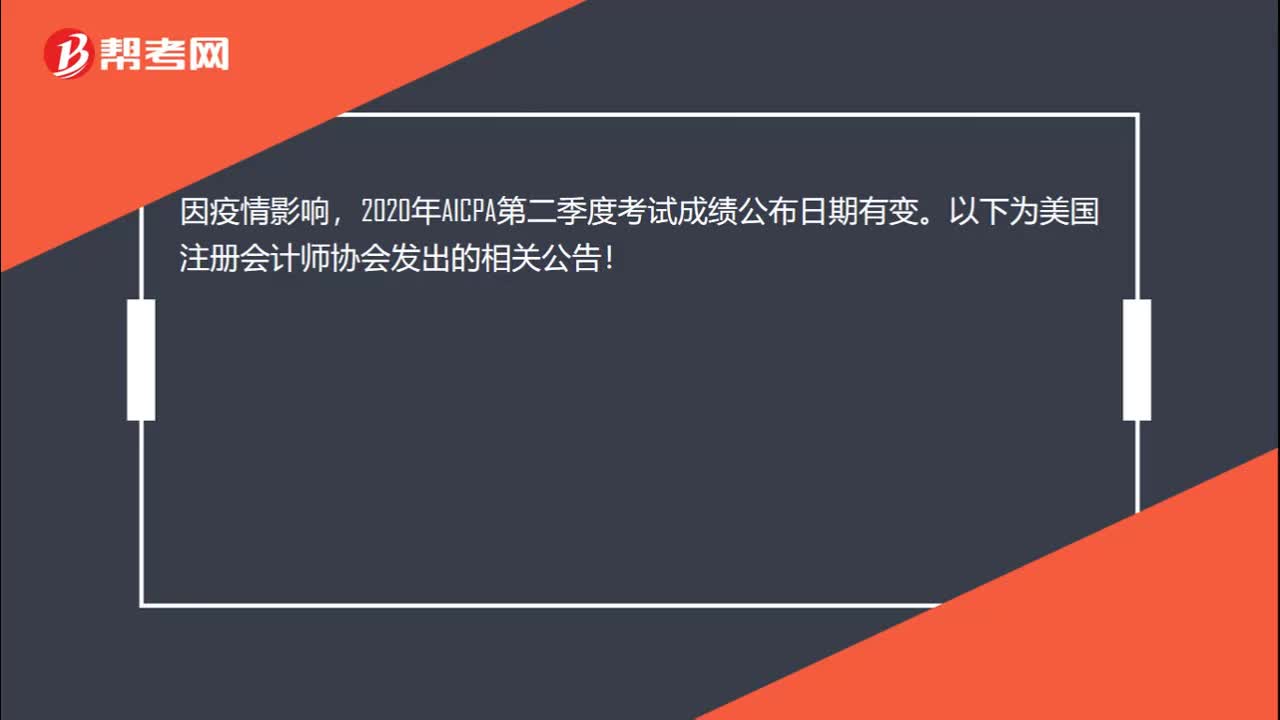

各位小伙伴大家好,很多想要报考美国CPA考试的考生不知道该如何准备全英文考试,为了帮助大家更好地备考,帮考网为大家带来了练习题供考生练习,帮助大家熟悉题目,具体内容如下:

一、A tax return preparer is not required to:

Audit the corporate records

Examine the business operations

Copy all underlying documents

In preparing a client\\\'s current-year individual income tax return, a tax practitioner discovers an errorin the prioryear\\\'s return. Under the rules of practice, the tax practitioner:

a. Is barred from preparing the current year\\\'s return until the prior-year erroris rectified.

b. Is required to notify the IRS of the error.

c. Must file an amended return to correct the error.

d. Must advise the client of the error.

答案:d

二、According to the FASB and IASB conceptual frameworks, useful information must exhibit the fundamental qualitative characteristics of:

a. Neutrality and verifiability.

b. Comparability and materiality.

c. Faithful representation and relevance.

d. Understandability and timeliness.

答案:c

三、According to the FASB and IASB conceptual frameworks, the primary users of financial reports include all of the following, except:

a. Regulators.

b. Lenders.

c. Creditors.

d. Investors.

答案:a

四、 Red Co. had $3 million in accounts receivable recorded on its books. Red wanted to convert the $3 million in receivables to cash in a more timely manner than waiting the 45 days forpayment as indicated on its invoices. Which of the following would alterthe timing of Red\\\'s cash flows forthe $3 million in receivables already recorded on its books?

a.Discount the receivables outstanding.

b.Factorthe receivables outstanding.

c.Demand payment from customers before the due date.

d.Change the due date of the invoice.

答案:b

五、On December 31, Year 1, Paxton Co. had a note payable due on August 1, Year 2. On January 20, Year 2, Paxton signed a financing agreement to borrow the balance of the note payable from a lending institution to refinance the note. The agreement does not expire within one year, and no violation of any provision in the financing agreement exists. On February 1, Year 2, Paxton was informed by its financial advisorthat the lender is not expected to be financially capable of honoring the agreement. Paxton\\\'s financial statements were issued on March 31, Year 2. How should Paxton classify the note on its balance sheet at December 31, Year 1?

a.As a current liability because the lender is not expected to be financially capable of honoring the agreement.

b.As a long-term liability because no violation of any provision in the financing agreement exists.

c.As a current liability because the financing agreement was signed after the balance sheet date.

d.As a long-term liability because the agreement does not expire within one year.

答案:a

六、Gar Co. factored its receivables without recourse with Ross Bank. Gar received cash as a result of this transaction, which is best described as a:

a.Sale of Gar\\\'s accounts receivable to Ross, with the risk of uncollectible accounts retained by Gar.

b.Loan from Ross to be repaid by the proceeds from Gar\\\'s accounts receivable.

c.Sale of Gar\\\'s accounts receivable to Ross, with the risk of uncollectible accounts transferred to Ross.

d.Loan from Ross collateralized by Gar\\\'s accounts receivable.

答案:c

七、On Merf\\\'s April 30, 1993, balance sheet a note receivable was reported as a noncurrent assetand its accrued interest foreight months was reported as a current asset. Which of the following terms would fit Merf\\\'s note receivable?

a.Principal and interest are due December 31, 1993.

b.Principal is due August 31, 1994, and interest is due August 31, 1993, and August 31, 1994.

c.Both principal and interest amounts are payable on December 31, 1993, and December 31, 1994.

d.Both principal and interest amounts are payable on August 31, 1993, and August 31, 1994.

答案:b

八、A company has a defined benefit pension plan forits employees. On December 31, year 1, the accumulated benefit obligation is $45,900, the projected benefit obligation is $68,100, and the fair value of the plan assets is $62,000.

What amount, if any, related to the definedbenefit plan should be recognized in the balance sheet at December 31, year 1?

a. A liability of $6,100.

b. An unrealized loss of $6,100.

c. Nothing, as the fair value of the plan assets exceeds the accumulated benefit obligation.

d. An assetof $16,100.

答案:a

以上就是今天分享的全部内容了,各位小伙伴根据自己的情况进行查阅,希望本文对各位有所帮助,预祝各位取得满意的成绩,如需了解更多相关内容,请关注帮考网!

86

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

30

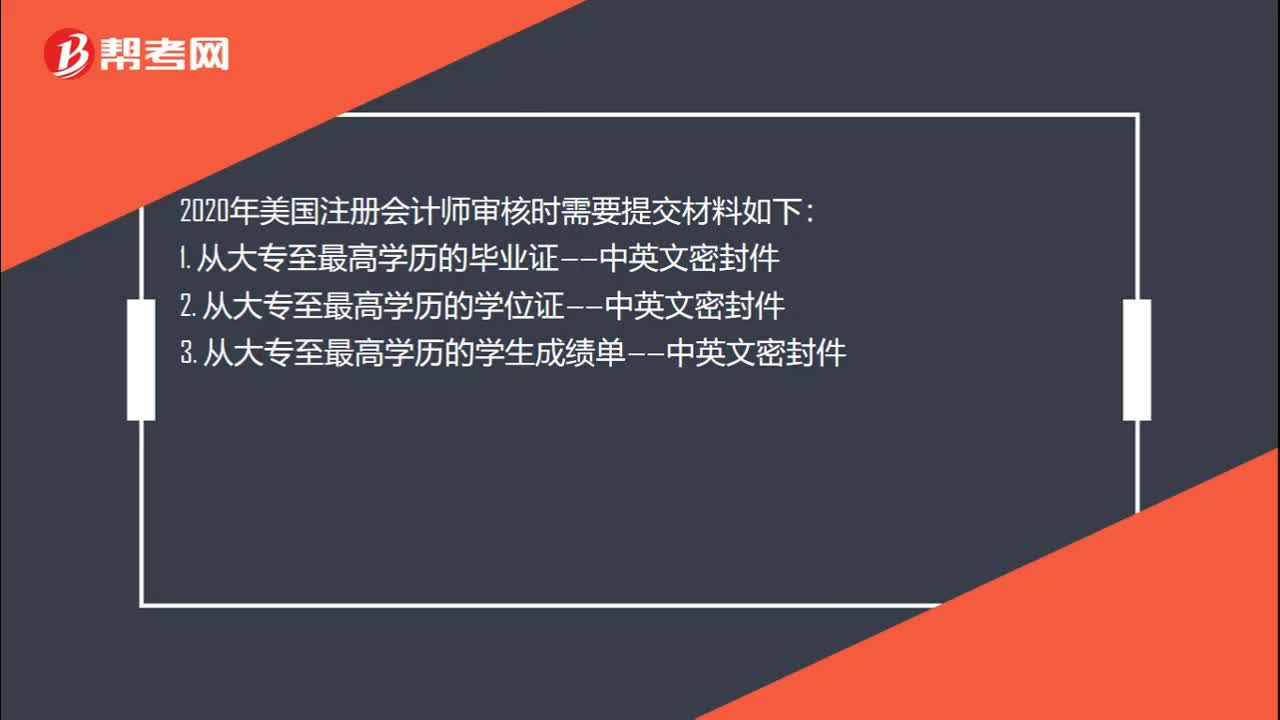

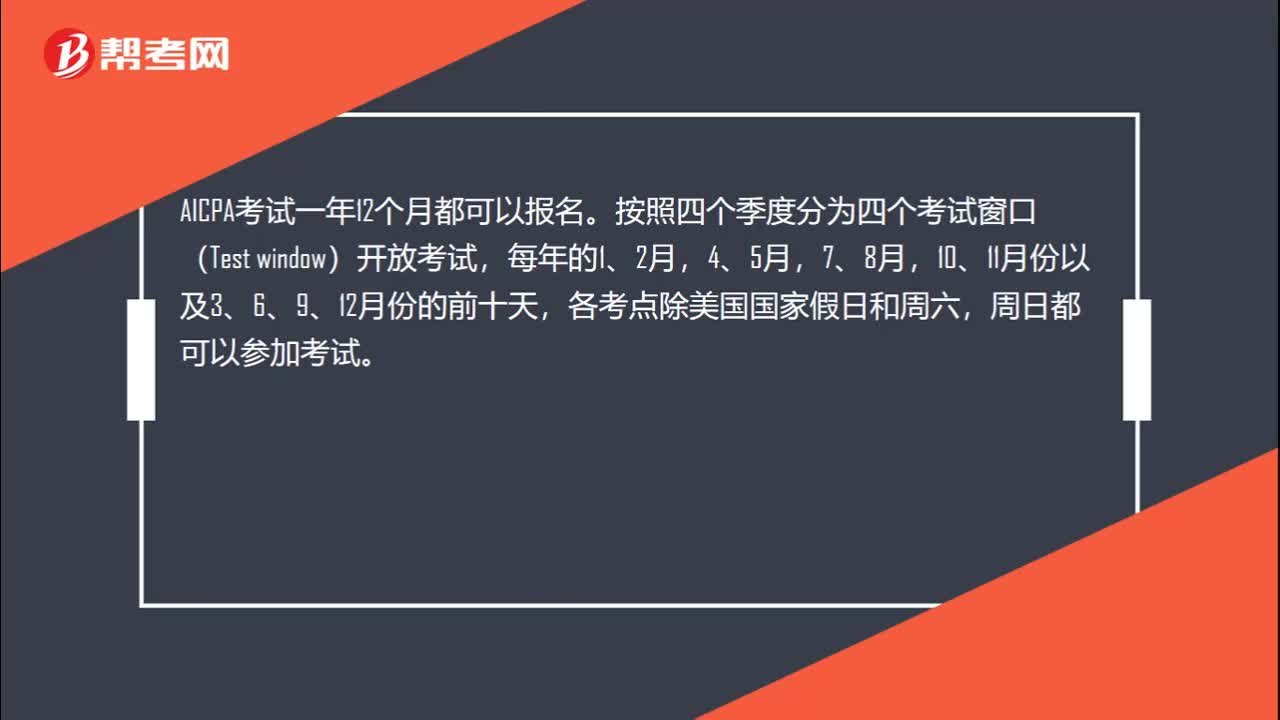

302020年AICPA怎么报考?:2020年AICPA怎么报考?AICPA报考流程如下:1.学历预评估。2. 学分评估,确认报考州。3.学历认证。4.补学分。5.申请NTS。6.预约考位。7. 安排行程。8.申请执照。

22

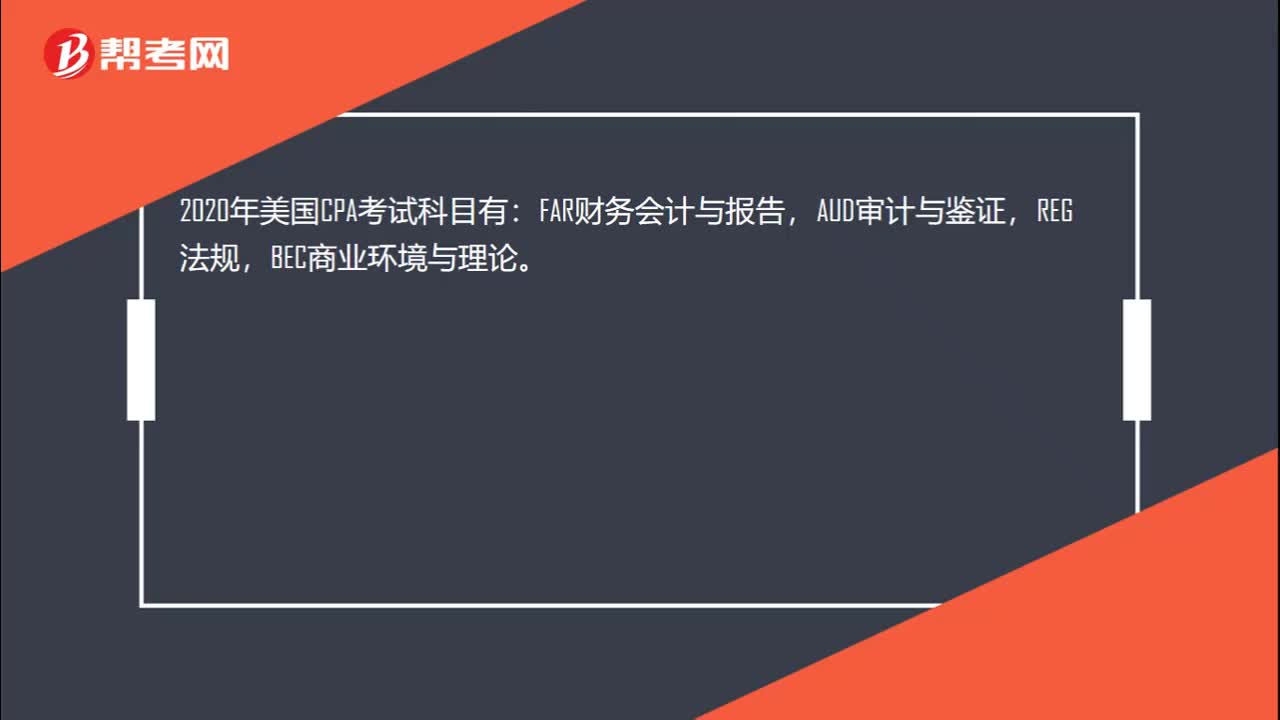

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料