当前位置: 首页ACCA考试业绩管理(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

又到了每日分享小课堂,各位赶快集合。今天帮考网分享的内容是2020年ACCA考试《业绩管理》科目辅导资料(4),相关考点都清楚了吗?还未了解的小伙伴一起来看看吧。

周期成本处理 - LIFECYCLE COSTING

Within the context of environmental accounting, lifecycle costing is a technique which requires the full environmental consequences, and, therefore, costs, arising from production of a product to be taken account across its whole lifecycle, literally ‘from cradle to grave’

识别环境成本 - IDENTIFYING ENVIRONMENTAL COSTS

Much of the information that is needed to prepare environmental management accounts could actually be found in a business ‘general ledger. A close review of it should reveal the costs of materials, utilities and waste disposal, at the least. The main problem is, however, that most of the costs will have to be found within the category of ’general overheads ‘if they are to be accurately identified. Identifying them could be a lengthy process, particularly in a large organization. The fact that environmental costs are often ’hidden ‘in this way makes it difficult for management to identify opportunities to cut environmental costs and yet it is crucial that they do so in a world which is becoming increasingly regulated and where scarce resources are becoming scarcer.

It is equally important to allocate environmental costs to the processes or products, which give rise to them. Only by doing this can an organization make well-informed business decisions? For example, a pharmaceutical company may be deciding whether to continue with the production of one of its drugs. In order to incorporate environmental aspects into its decision, it needs to know exactly how many products are input into the process compared to its outputs; How much waste is created during the process; how much labor and fuel is used in making the drug; how much packaging the drug uses and what percentage of that is recyclable etc. Only by identifying these costs and allocating them to the product can an informed decision be made about the environmental effects of continued production.

In 2003,the UNDSD identified four management accounting techniques for the identification and allocation of environmental costs: input/outflow analysis,flow cost accounting, activity based costing and lifecycle costing. These are referred to later under ‘different methods of accounting for environmental costs’。

以上就是帮考网给大家带来的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

66

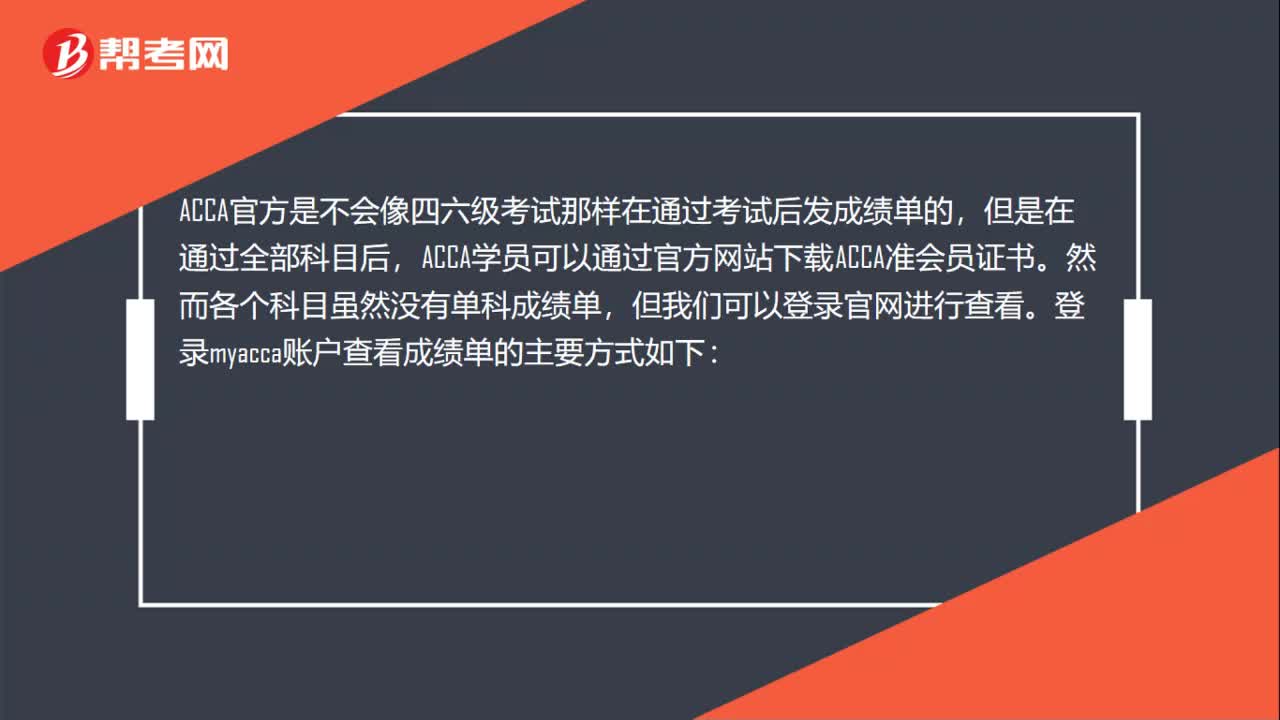

66ACCA考试有成绩单吗?:ACCA考试有成绩单吗?ACCA官方是不会像四六级考试那样在通过考试后发成绩单的,但是在通过全部科目后,ACCA学员可以通过官方网站下载ACCA准会员证书。然而各个科目虽然没有单科成绩单,但我们可以登录官网进行查看。登录myacca账户查看成绩单的主要方式如下:1、登陆ACCA官网accaglobal.com,进入学员个人页面;2、 输入个人的学员注册号码及密码后点击按钮“login”

33

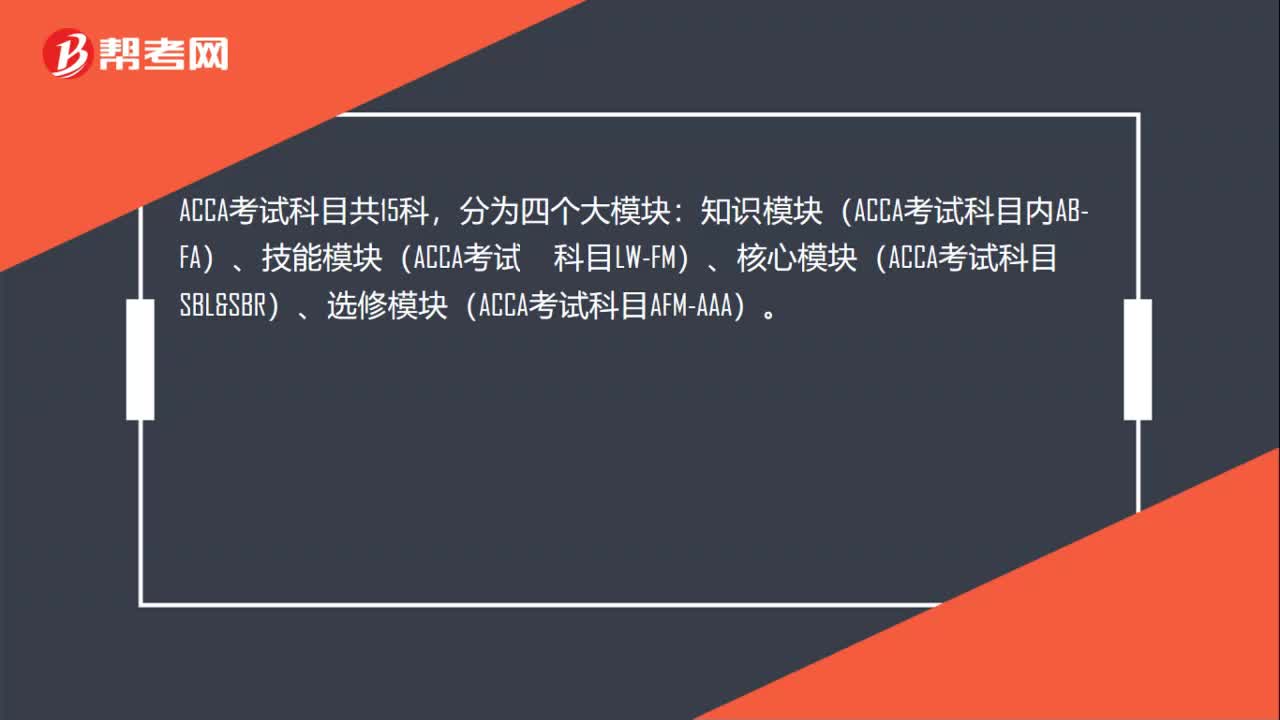

33ACCA考试科目有哪些?:ACCA考试科目有哪些?ACCA考试科目共15科,分为四个大模块:知识模块(ACCA考试科目内AB-FA)、技能模块(ACCA考试容科目LW-FM)、核心模块(ACCA考试科目SBLSBR)、选修模块(ACCA考试科目AFM-AAA)。

18

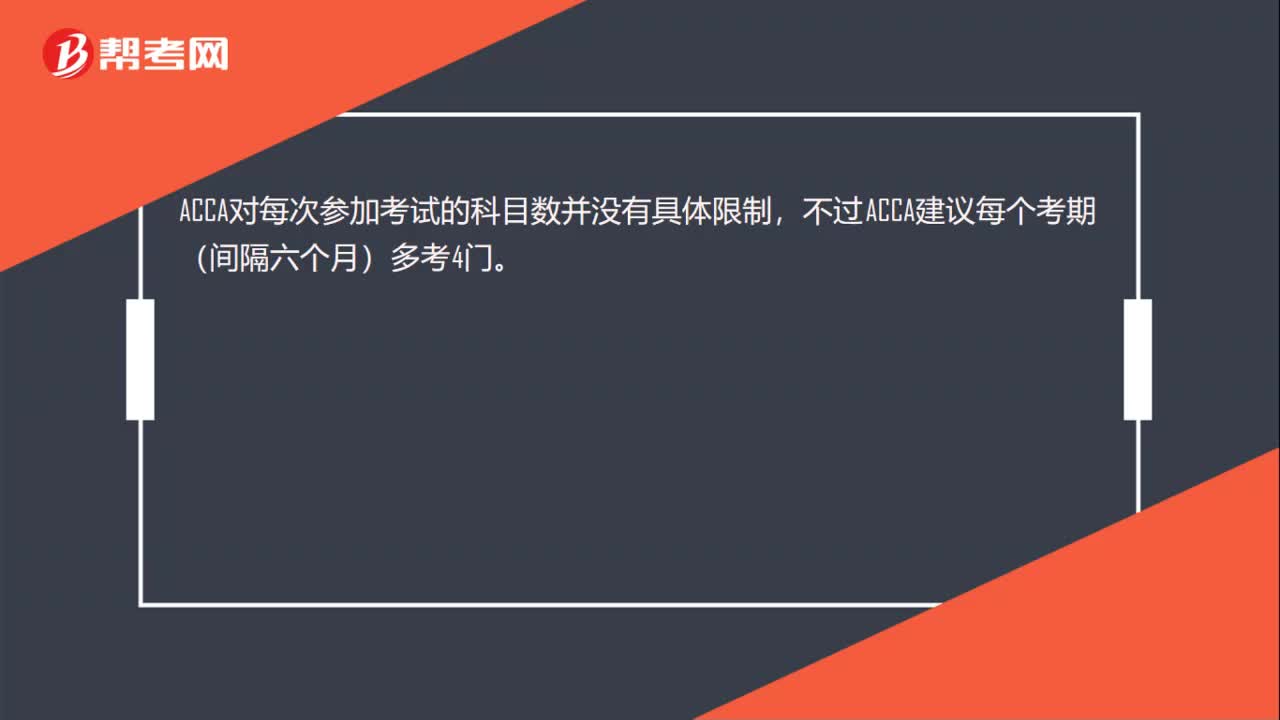

18ACCA考试对报考科目有限制吗?:ACCA考试对报考科目有限制吗?ACCA对每次参加考试的科目数并没有具体限制,不过ACCA建议每个考期(间隔六个月)多考4门。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料