当前位置: 首页ACCA考试业绩管理(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

各位小伙伴注意了,备考已经进入了关键期,现在状态如何啊,今天帮考网为大家分享2020年ACCA考试《业绩管理》科目辅导资料(3),一起来看看吧。

环境成本会计 - ACCOUNTING FOR ENVIRONMENTAL COSTS

In the context of Paper F5, when the syllabus requires you to describe the different methods of accounting for environmental costs, it aims to cover two areas:

Internal reporting of environmental costs, which has already been discussed in the introduction.

Management accounting techniques for the identification and allocation of environmental costs: the most appropriate ones for the Paper F5 syllabus are those identified by the UNDSD, namely input/outflow analysis, flow cost accounting, activity-based costing and lifecycle costing.

输入/输出分析 - INPUT/OUTFLOW ANALYSIS

This technique records material inflows and balances this with outflows on the basis that, what comes in, must go out. So, if 100kg of materials have been bought and only 80kg of materials have been produced, for example, then the 20kg difference must be accounted for in some way. It may be, for example, that 10% of it has been sold as scrap and 90% of it is waste. By accounting for outputs in this way, both in terms of physical quantities and, at the end of the process, in monetary terms too, businesses are forced to focus on environmental costs.

流量成本处理 - FLOW COST ACCOUNTING

This technique uses not only material flows but also the organizational structure. It makes material flows transparent by looking at the physical quantities involved, their costs and their value. It divides the material flows into three categories: material, system and delivery and disposal. The values and costs of each of these three flows are then calculated. The aim of flow cost accounting is to reduce the quantity of materials which, as well as having a positive effect on the environment, should have a positive effect on a business‘ total costs in the long run.

作业成本处理 - ACTIVITY-BASED COSTING

ABC allocates internal costs to cost centers and cost drivers based on the activities that give rise to the costs. In an environmental accounting context, it distinguishes between environment-related costs, which can be attributed to joint cost centers, and environment-driven costs, which tend to be hidden on general overheads.

以上就是帮考网给大家带来的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

66

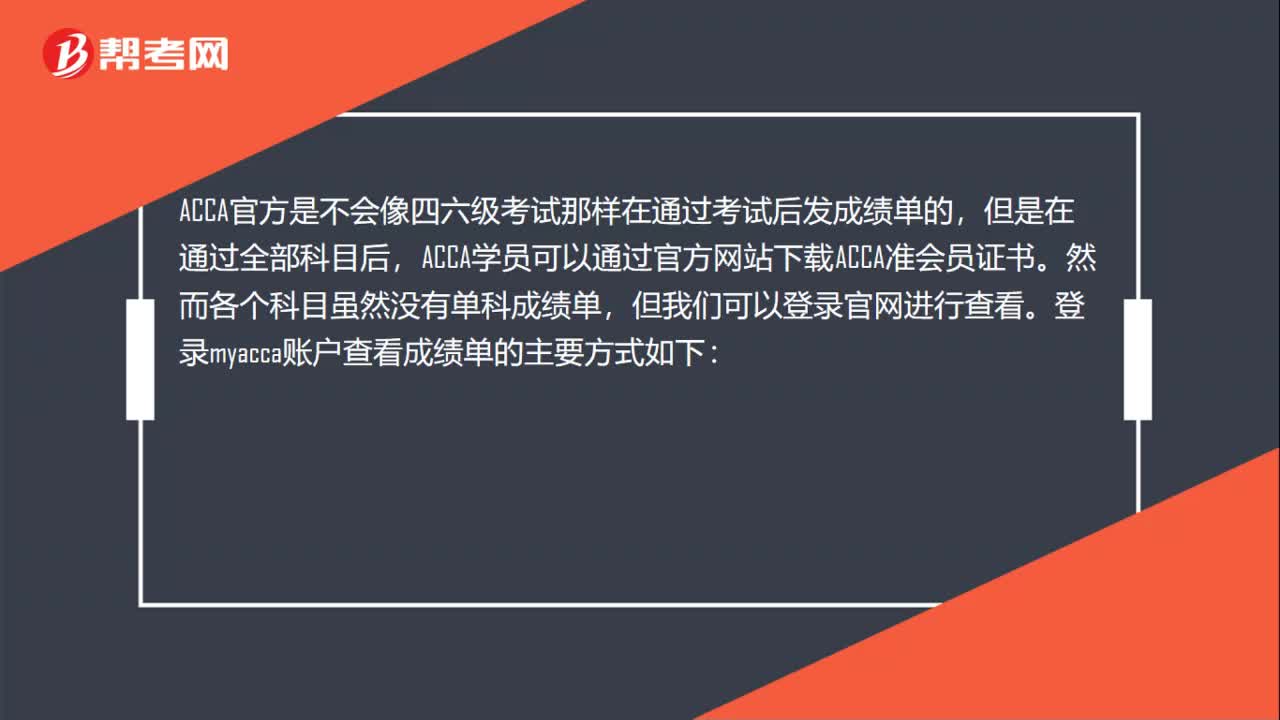

66ACCA考试有成绩单吗?:ACCA考试有成绩单吗?ACCA官方是不会像四六级考试那样在通过考试后发成绩单的,但是在通过全部科目后,ACCA学员可以通过官方网站下载ACCA准会员证书。然而各个科目虽然没有单科成绩单,但我们可以登录官网进行查看。登录myacca账户查看成绩单的主要方式如下:1、登陆ACCA官网accaglobal.com,进入学员个人页面;2、 输入个人的学员注册号码及密码后点击按钮“login”

33

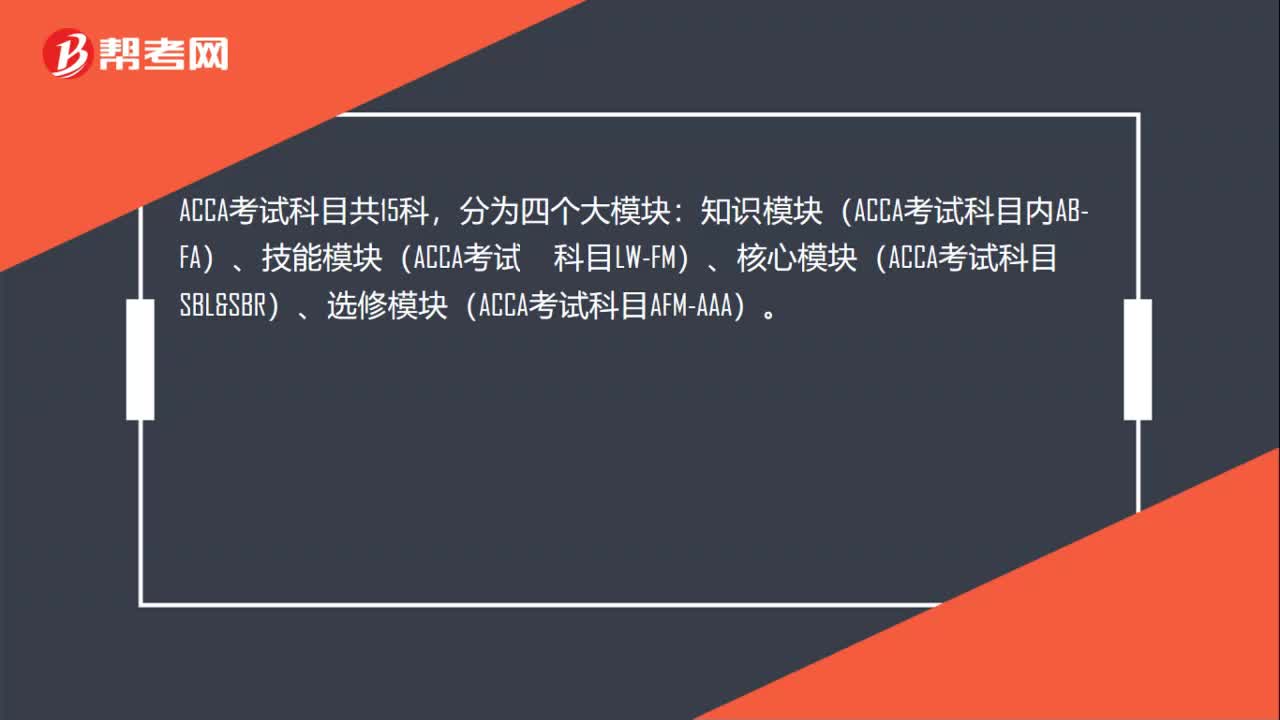

33ACCA考试科目有哪些?:ACCA考试科目有哪些?ACCA考试科目共15科,分为四个大模块:知识模块(ACCA考试科目内AB-FA)、技能模块(ACCA考试容科目LW-FM)、核心模块(ACCA考试科目SBLSBR)、选修模块(ACCA考试科目AFM-AAA)。

18

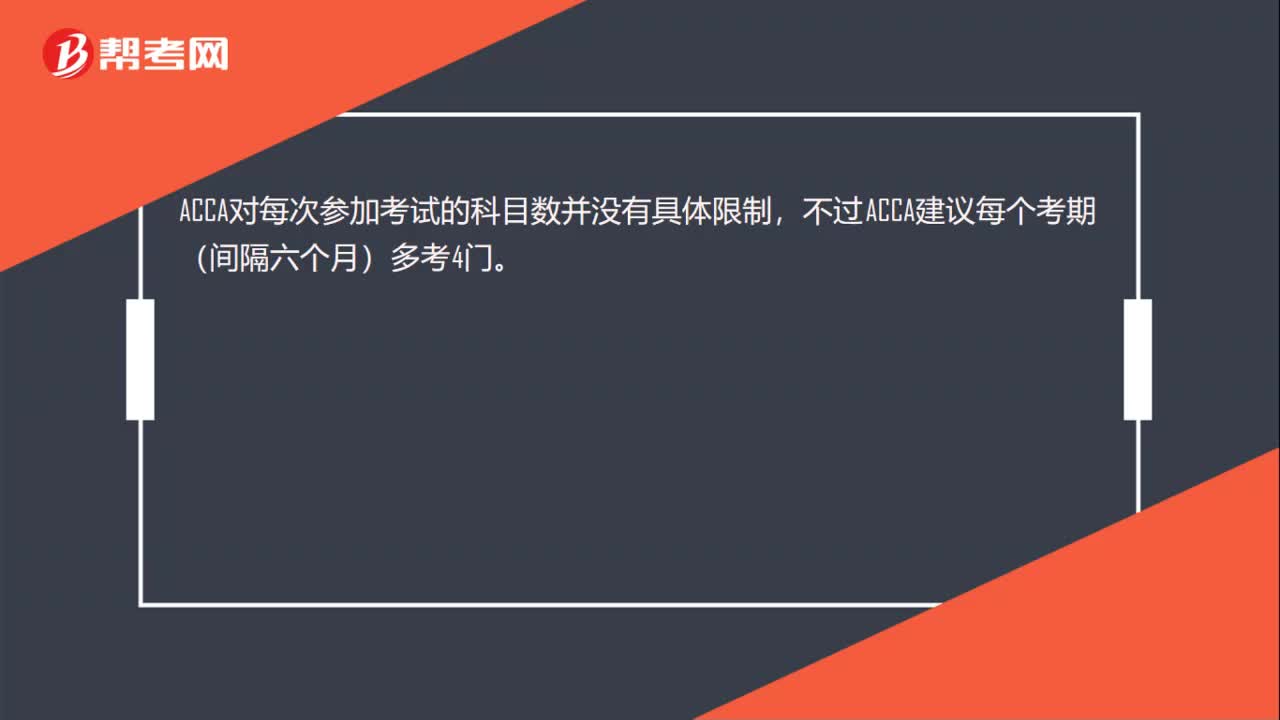

18ACCA考试对报考科目有限制吗?:ACCA考试对报考科目有限制吗?ACCA对每次参加考试的科目数并没有具体限制,不过ACCA建议每个考期(间隔六个月)多考4门。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料