当前位置: 首页ACCA考试财务管理(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

今日帮考网为大家分享2020年ACCA考试财务管理备考资料:知识点(8),供大家参考,希望对大家有所帮助,查看更多备考内容请关注帮考网ACCA考试频道。

【知识点】Liquidity ratio(流动比率)

Liquidity ratio

Working capital ratios may help to indicate whether a company is over-capitalised, with excessive working capital, or if a business is likely to fail. A business which is trying to do too much too quickly with too little long-term capital is overtrading.

Current ratio

The current ratio is the standard test of liquidity. A company should have enough current assets that give a promise of \'cash to come\' to meet its commitments to pay its current liabilities. Too high a ratio implies that too much cash may be tied up in receivables and inventories. What is \'comfortable\' varies between different types of business.

Quick ratio

Companies are unable to convert all their current assets into cash very quickly. In some businesses where inventory turnover is slow, most inventories are not very liquid assets, and the cash cycle is long. For these reasons, we calculate an additional liquidity ratio, known as the quick ratio or acid test ratio.

This ratio should ideally be at least 1 for companies with a slow inventory turnover. For companies with a fast inventory turnover, a quick ratio can be less than 1 without suggesting that the company is in cash flow difficulties.

Again, these liquidity ratios are a guide to the risk of cash flow problems and insolvency. If a company suddenly finds that it is unable to renew its short-term liabilities (for example, if the bank suspends its overdraft facilities), there will be a danger of insolvency unless the company is able to turn enough of its current assets into cash quickly.

The sales revenue / net working capital ratio

The ratio of

shows the level of working capital supporting sales and indicates how efficiently working capital is being used to generate sales. Working capital must increase in line with sales to avoid liquidity problems and this ratio can be used to forecast the level of working capital needed for a projected level of sales.

【知识点】Early settlement discounts(提前付款现金折扣)

Early settlement discounts

Early settlement discounts may be employed to shorten average credit periods and to reduce the investment in accounts receivable and therefore interest costs of the finance invested in trade receivables. The benefit in interest cost saved should exceed the cost of the discounts allowed.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝12月份ACCA考试取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

25

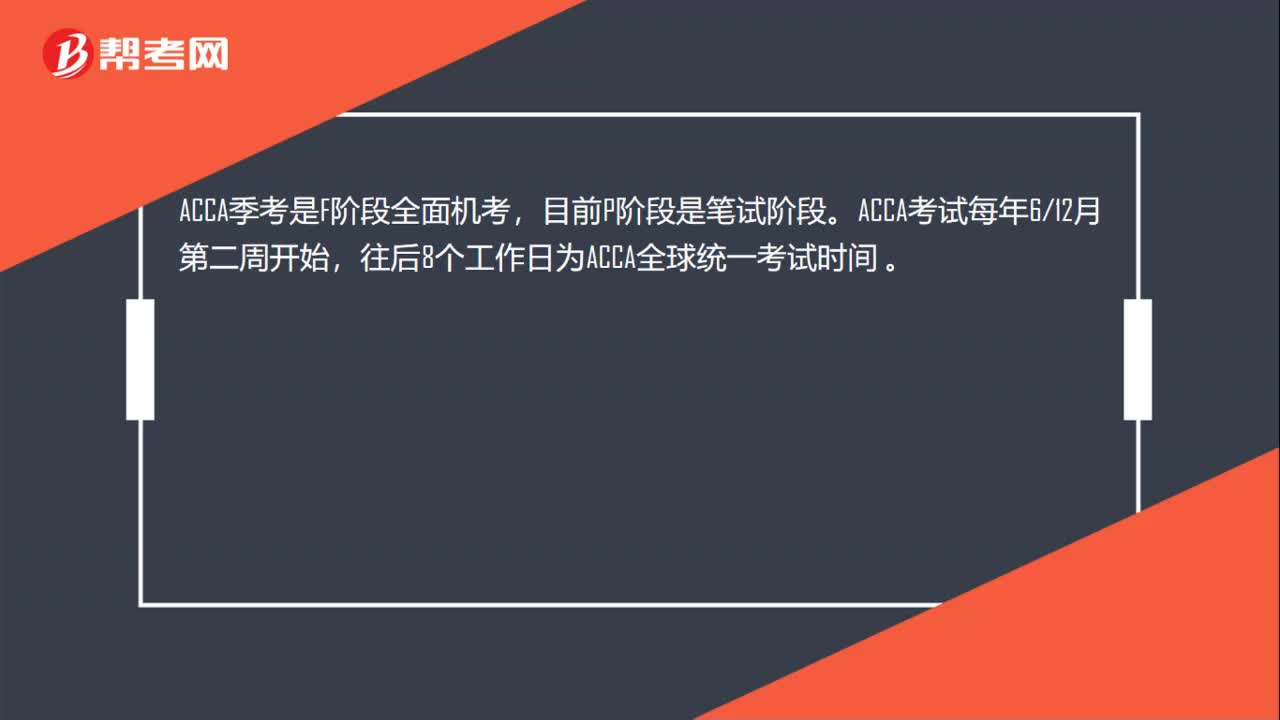

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

56

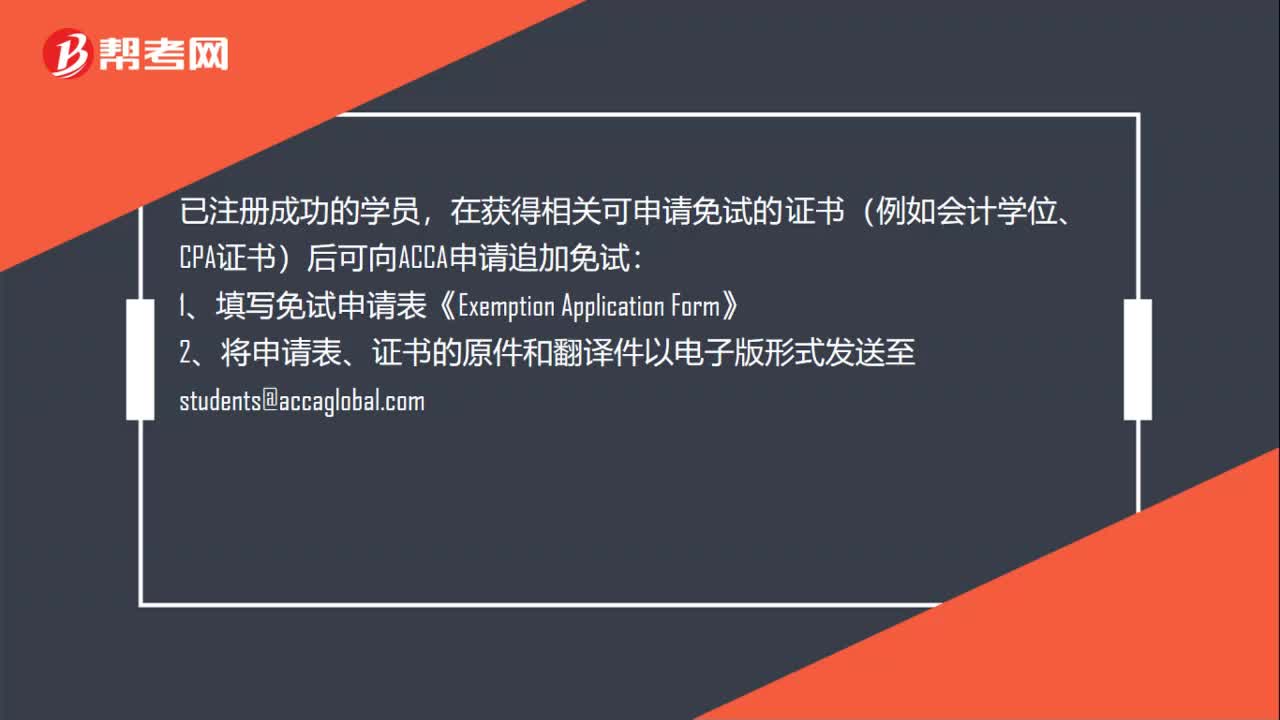

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

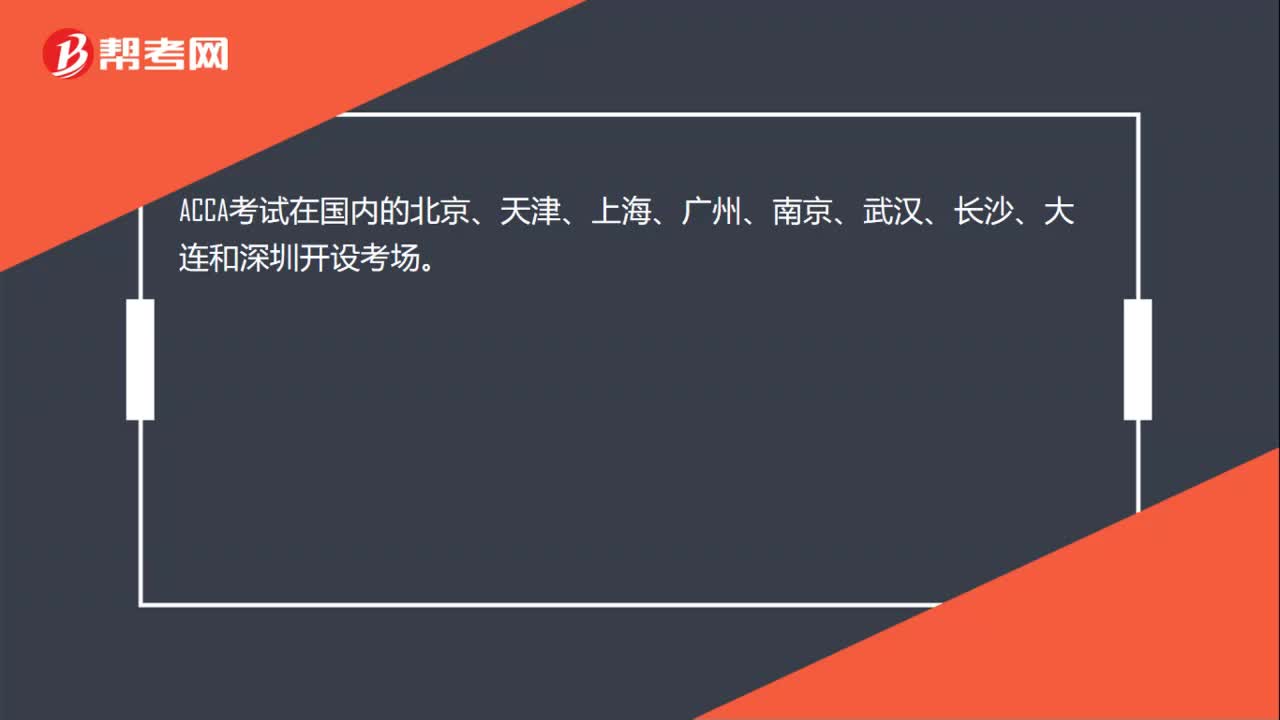

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料