当前位置: 首页ACCA考试财务管理(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

距离ACCA考试还有52天的时间,各位小伙伴备考的如何了啊,今日帮考网为大家分享“2020年ACCA考试财务管理备考资料:知识点(1)”的相关知识点,一起过来复习巩固一下吧。

【知识点】Overtrading(过量交易)

Overtrading

Overtrading (also known as under-capitalisation)

In contrast with over-capitalisation, overtrading happens when a business tries to do too much too quickly with too little long-term capital.

Even if an overtrading business operates at a profit, it could easily run into serious trouble because it is short of cash.

Symptoms of overtrading

There is a rapid increase in sales revenue.

There is a rapid increase in the volume of current assets and possibly also non-current assets. Inventory turnover and accounts receivable turnover might slow down, in which case the rate of increase in inventories and accounts receivable would be even greater than the rate of increase in sales.

There is only a small increase in equity capital (perhaps through retained profits). Most of the increase in assets is financed by credit, especially:

• Trade accounts payable-the payment period to accounts payable is likely to lengthen.

• A bank overdraft, which often reaches or even exceeds the limit of the facilities agreed by the bank.

Some debt ratios and liquidity ratios alter dramatically.

• The proportion of total assets financed by proprietors\' (owner) capital falls, and the proportion financed by credit rises.

• The current ratio and the quick ratio fall.

• The business might have a liquid deficit; that is, an excess of current liabilities over current assets.

Causes of overtrading

• A business seeking to increase its revenue too rapidly without an adequate capital base.

• When a business repays a loan, it often replaces the old loan with a new one (refinancing). However a business might repay a loan without replacing it, with the consequence that it has less long-term capital to finance its current level of operations.

• A business might be profitable, but in a period of inflation, its retained profits might be insufficient to pay for replacement non-current assets and inventories, which now cost more because of inflation.

Suitable solutions to reduce the degree of overtrading.

• New capital from the shareholders could be injected.

• Better control could be applied to inventories and accounts receivable. The company could abandon ambitious plans for increased sales and more non-current asset purchases.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝12月份ACCA考试取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

25

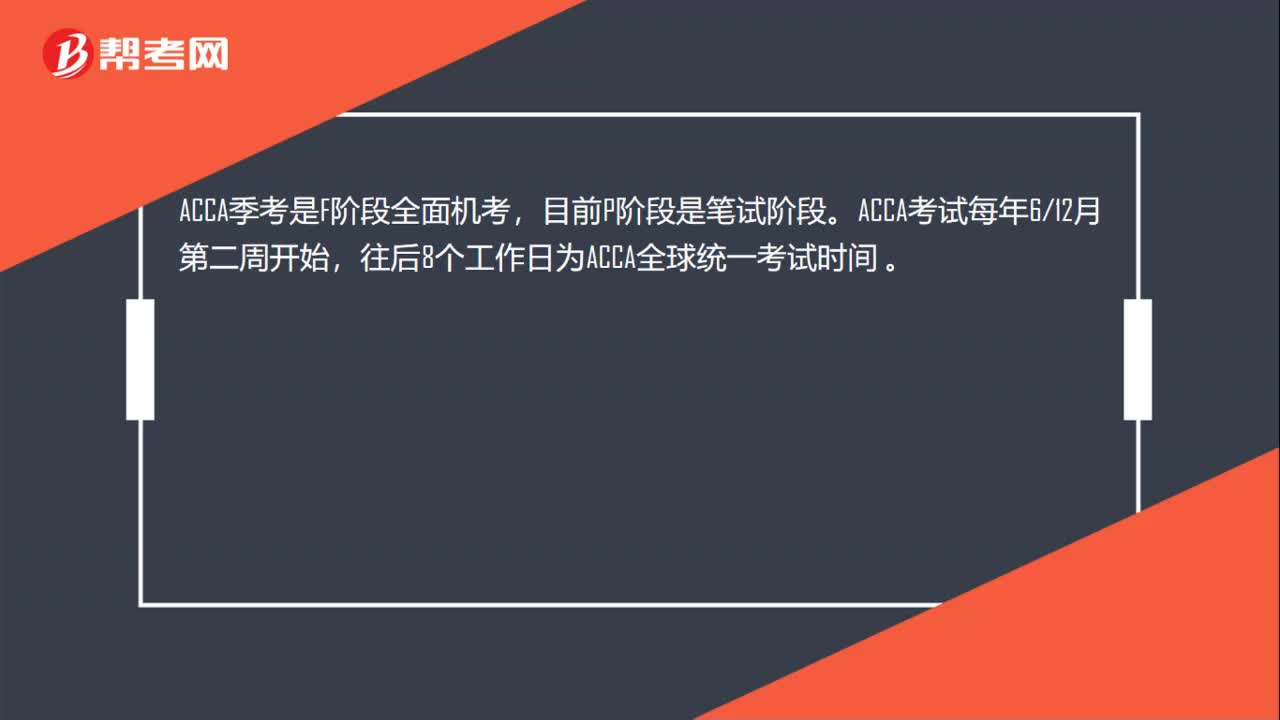

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

56

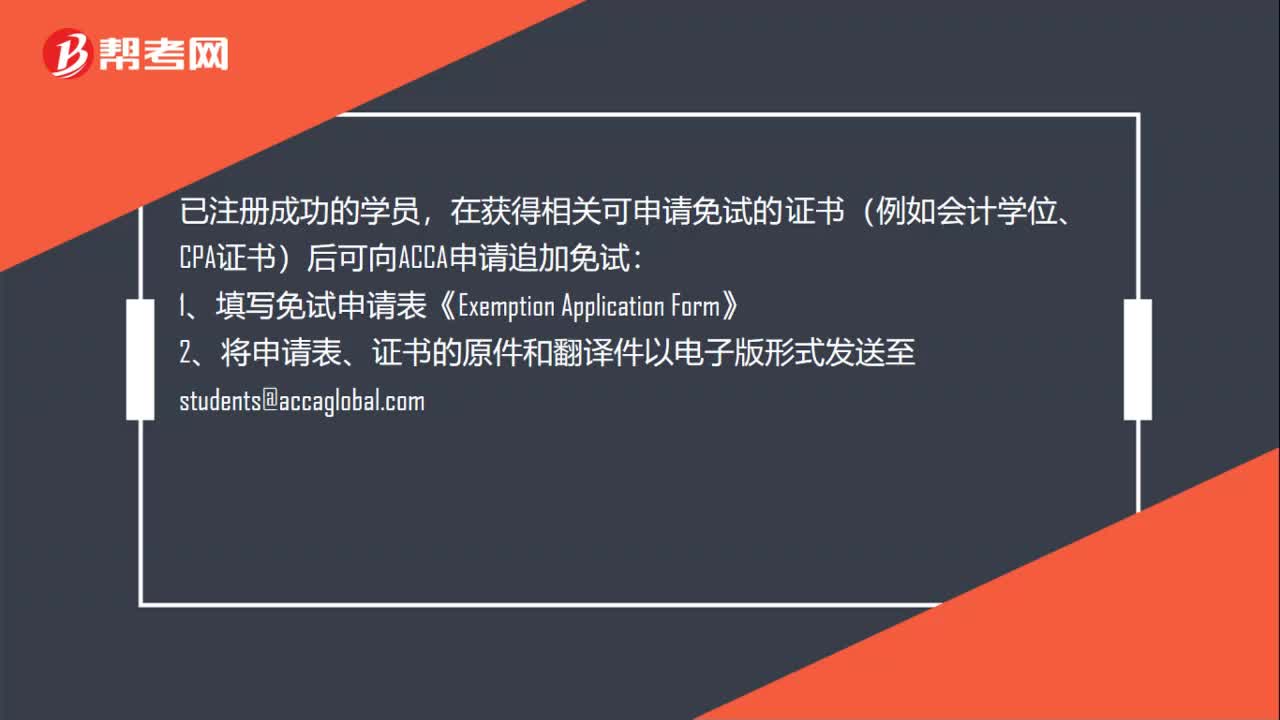

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

20

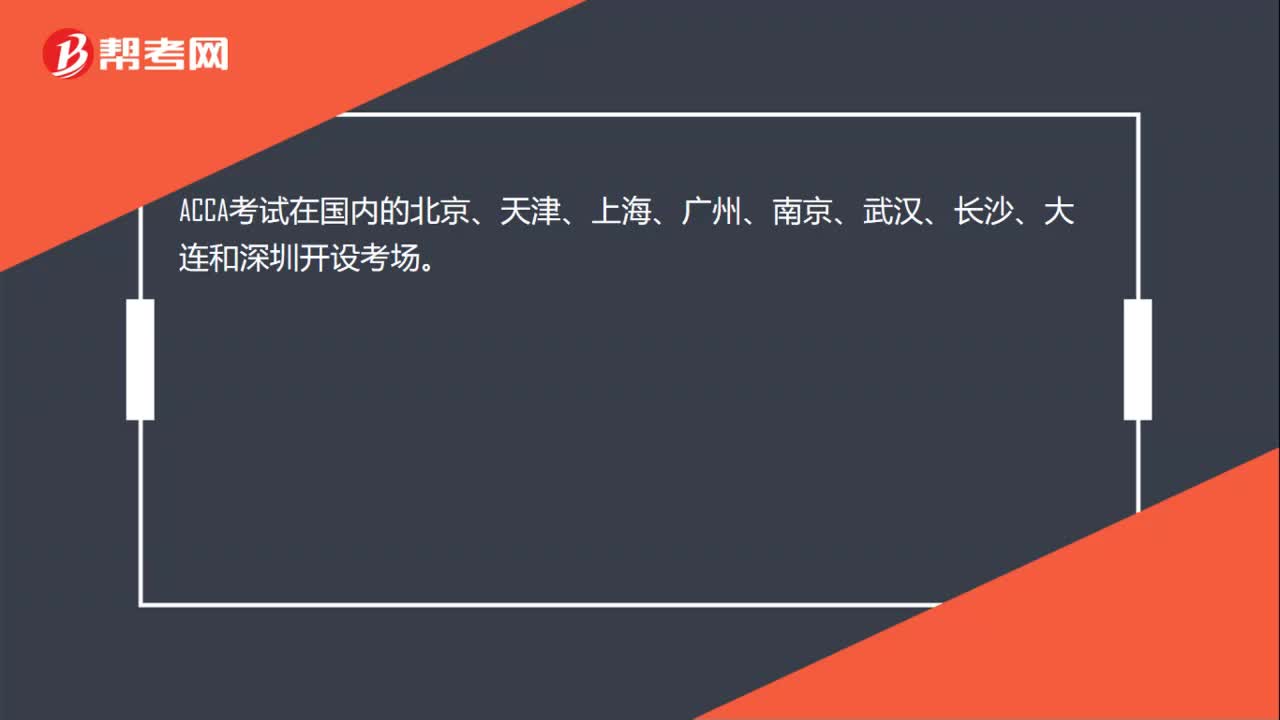

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料