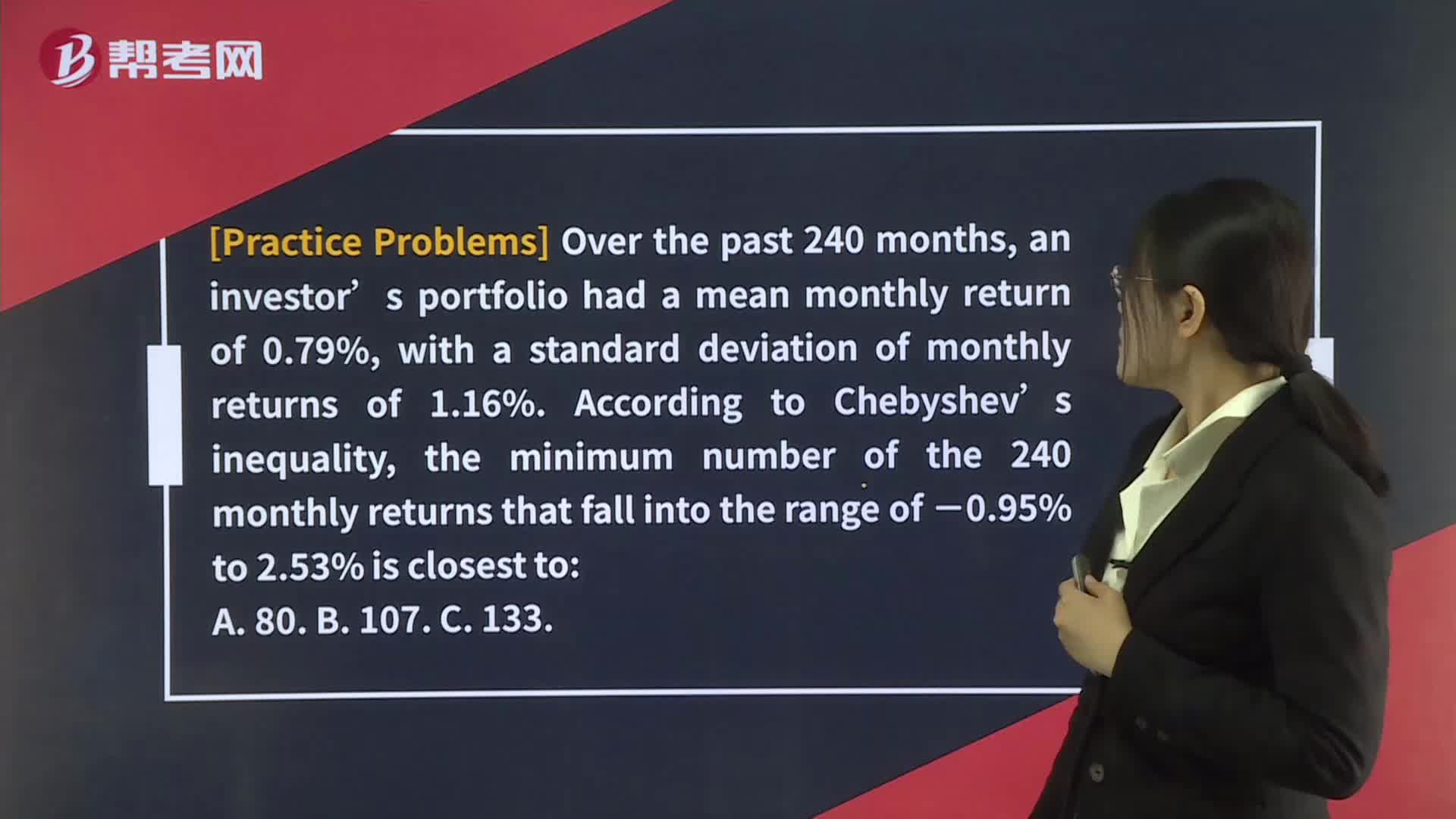

Chebyshev’s Inequality

Chebyshev’s inequality is a statistical concept that provides an upper bound on the probability that a random variable deviates from its mean by a certain amount. It states that for any distribution, the probability that a random variable deviates from its mean by more than k standard deviations is at most 1/k^2, where k is any positive number greater than 1.

Mathematically, Chebyshev’s inequality can be expressed as:

P(|X-μ|≥kσ)≤1/k^2

where P is the probability, X is the random variable, μ is the mean of X, σ is the standard deviation of X, and k is any positive number greater than 1.

For example, if a random variable X has a mean of 50 and a standard deviation of 10, Chebyshev’s inequality states that the probability that X deviates from its mean by more than 2 standard deviations (i.e., k=2) is at most 1/2^2, or 25%. Therefore, the probability that X lies between 30 and 70 (i.e., within 2 standard deviations of the mean) is at least 75%.

Chebyshev’s inequality is a powerful tool in probability theory and statistics, as it provides a general bound on the deviation of a random variable from its mean, regardless of the distribution of the variable. However, it is a relatively weak bound, as it does not take into account the shape of the distribution or any other characteristics of the variable.

帮考网校

帮考网校