下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

各位小伙伴大家好,美国CPA考试共有三种题型:选择题,案例分析题和写作题,不同科目题型分配不同,为了帮助大家更好地备考,帮考网带来了练习题供大家练习,帮助大家熟悉题型和积累答题经验,具体内容如下:

1.At the beginning of Year 2, a company invested $40,000 in a marketable equity security. At that time the security was appropriately classified as an available-for-sale security. At the end of Year 2, the security had a fair value of $28,500. The change in fair value is deemed temporary. How should this change in fair value be reported in the financial statements?

a. As a realized loss of $11,500 as part of net income.

b. As an unrealized loss of $11,500 as part of net income.

c. As a realized loss of $11,500 as part of other comprehensive income.

d. As an unrealized loss of $11,500 as part of other comprehensive income.

答案:D

Explanation

Choice “d” is correct. Unrealized gains and losses on available-for-sale (AFS) securities are booked in other comprehensive income (OCI). Changes in the fair value of the securities will continue to go to OCI until the security is sold, at which point the balance in OCI will be removed and a realized gain orloss will be booked on the income statement. Because the security has not been sold, the change in fair value from $40,000 to $28,500 represents an unrealized loss of $11,500, which goes straight to OCI.

Choice “a” is incorrect. This choice would only be correct if the security was actually sold for$28,500. Changes in fair value forAFS securities represent unrealized gains orlosses which go to OCI.

Choice “c” is incorrect. The loss of $11,500 will go into OCI, but it will be unrealized rather than realized.

Choice “b” is incorrect. Unrealized losses on AFS securities go into OCI rather than onto the income statement.

2.Kale Co. purchased bonds at a discount on the open market as an investment and intends to hold these bonds to maturity. Kale should account forthese bonds at:

a. Fair value.

b. Lower of cost ormarket.

c. Amortized cost.

d. Cost.

答案:C

Explanation

Choice "c" is correct. Bond investments which are intended to be held until the maturity date are classified as held-to-maturity securities and are reported at their amortized cost.

Choice "d" is incorrect. Investments in marketable securities are reported at fair value orat their amortized cost, depending on their classification.

Choice "a" is incorrect. Trading securities and available-for-sale securities are reported at their fair value.

Choice "b" is incorrect. The lower of cost ormarket method is no longer used to account formarketable securities.

以上就是今天分享的全部内容了,希望本文对各位有所帮助,预祝各位取得满意的成绩,如需了解更多相关内容,请关注帮考网!

86

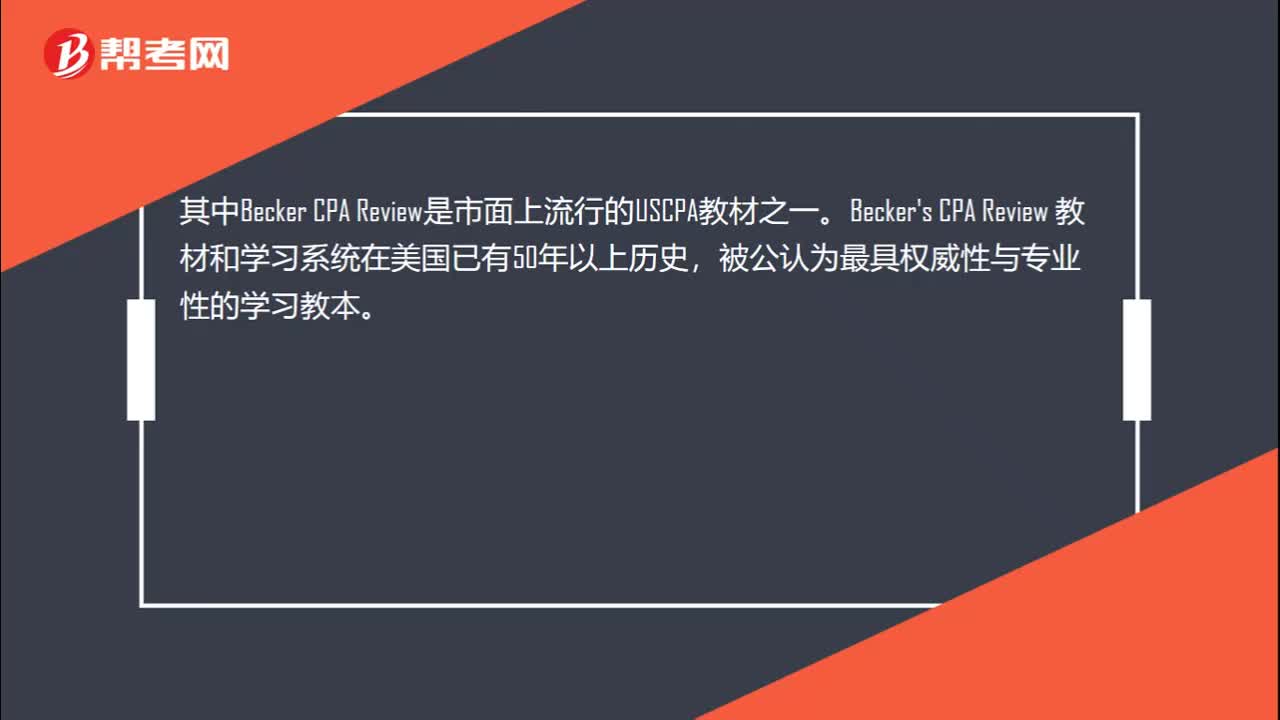

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

22

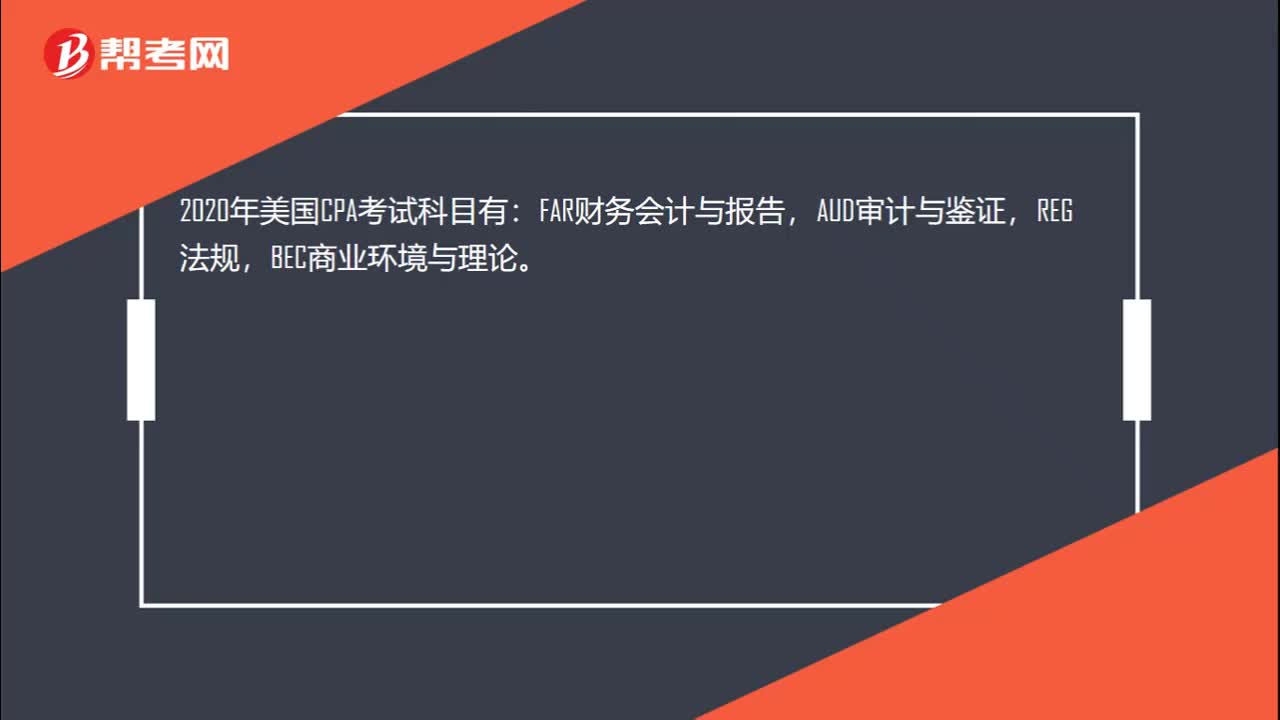

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

42

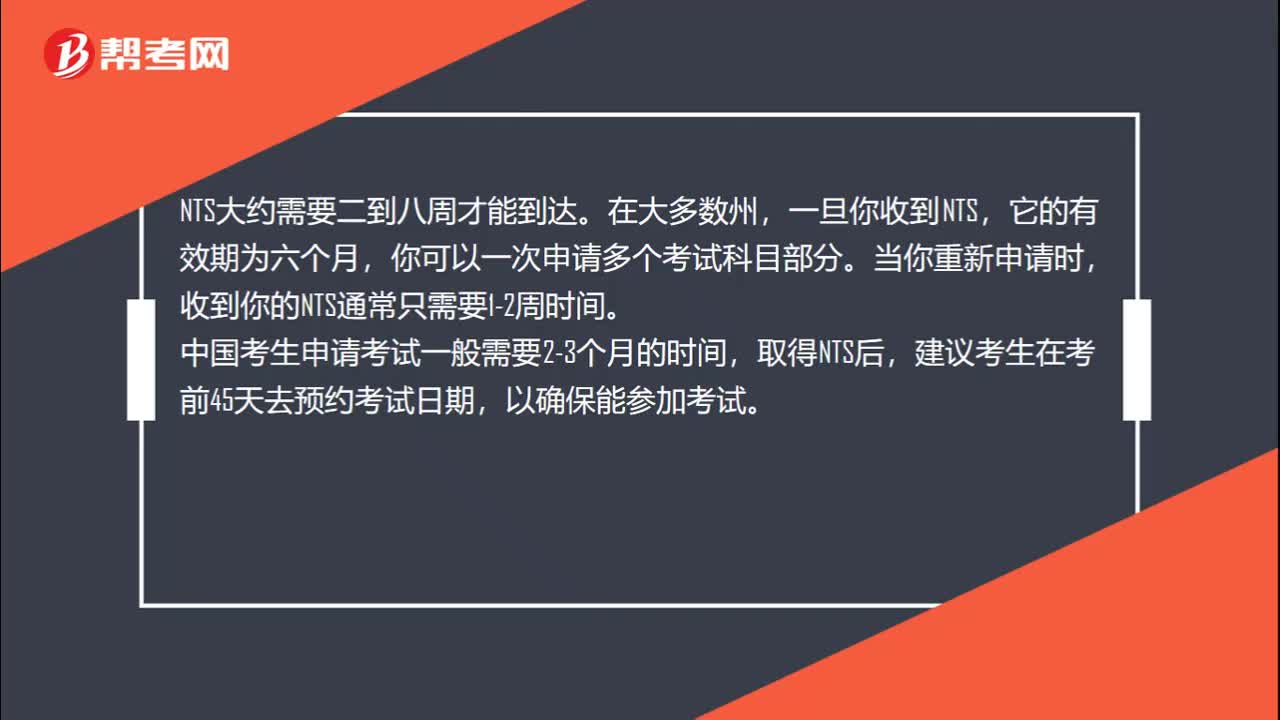

422020年AICPA考试预约考试后多久收到NTS准考证?:2020年AICPA考试预约考试后多久收到NTS准考证?NTS大约需要二到八周才能到达。在大多数州,一旦你收到NTS,它的有效期为六个月,你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。中国考生申请考试一般需要2-3个月的时间,取得NTS后,建议考生在考前45天去预约考试日期,以确保能参加考试。

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料