下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

又到了每日分享小课堂,各位赶快集合。今天帮考网分享的内容是2020年ACCA考试审计与认证业务(基础)精选考点(5),相关考点都清楚了吗?还未了解的小伙伴一起来看看吧。

ACCAF8考试:Audit risk

什么是审计风险

According to the IAASB Glossary of Terms (1), audit risk is defined as follows:

‘The risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. Audit risk is a function of material misstatement and detection risk.’

为什么审计风险对于审计师是重要的

Audit risk is fundamental to the audit process because auditors cannot and do not attempt to check all transactions. Students should refer to any published accounts of large companies and think about the vast number of transactions in a statement of comprehensive income and a statement of financial position. It would be impossible to check all of these transactions, and no one would be prepared to pay the auditors to do so, hence the importance of the risk‑based approach toward auditing. Traditionally, auditors have used a risk-based approach in order to minimize the chance of giving an inappropriate audit opinion, and audits conducted in accordance with ISAs must follow the risk‑based approach, which should also help to ensure that audit work is carried out efficiently, using the most effective tests based on the audit risk assessment.

Auditors should direct audit work to the key risks (sometimes also described as significant risks), where it is more likely that error in transactions and balances will lead to a material misstatement in the financial statements. It would be inefficient to address insignificant risks in a high level of detail, and whether a risk is classified as a key risk or not is a matter of judgment for the auditor.

相关准则- ISAS

There are many references throughout the ISAs to audit risk, but perhaps the two most important audit risk-related ISAs are as follows:

ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with ISAs

ISA 200 sets out the overall objectives of the auditor, and the standard explains the nature and scope of an audit designed to enable an auditor to meet those objectives. References to audit risk are frequently made by ISA 200, and the standard requires that the auditor shall plan and perform an audit with professional skepticism, recognizing that circumstances might exist that may cause the financial statements to be materially misstated. Professional skepticism is defined as an attitude that includes a questioning mind and a critical assessment of evidence.

ISA 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 deals with the auditor’s responsibility to identify and assess the risks of material misstatement in the financial statements through an understanding of the entity and its environment, including the entity’s internal controls and risk assessment process. The first version of ISA 315 was originally published in 2003 after a joint audit risk project had been carried out between the IAASB, and the United States Auditing Standards Board. Changes in the audit risk standards have arguably been the single biggest change in auditing standards in recent years, so the significance of ISA 315, and the topic of audit risk, should not be underestimated by auditing students.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

29

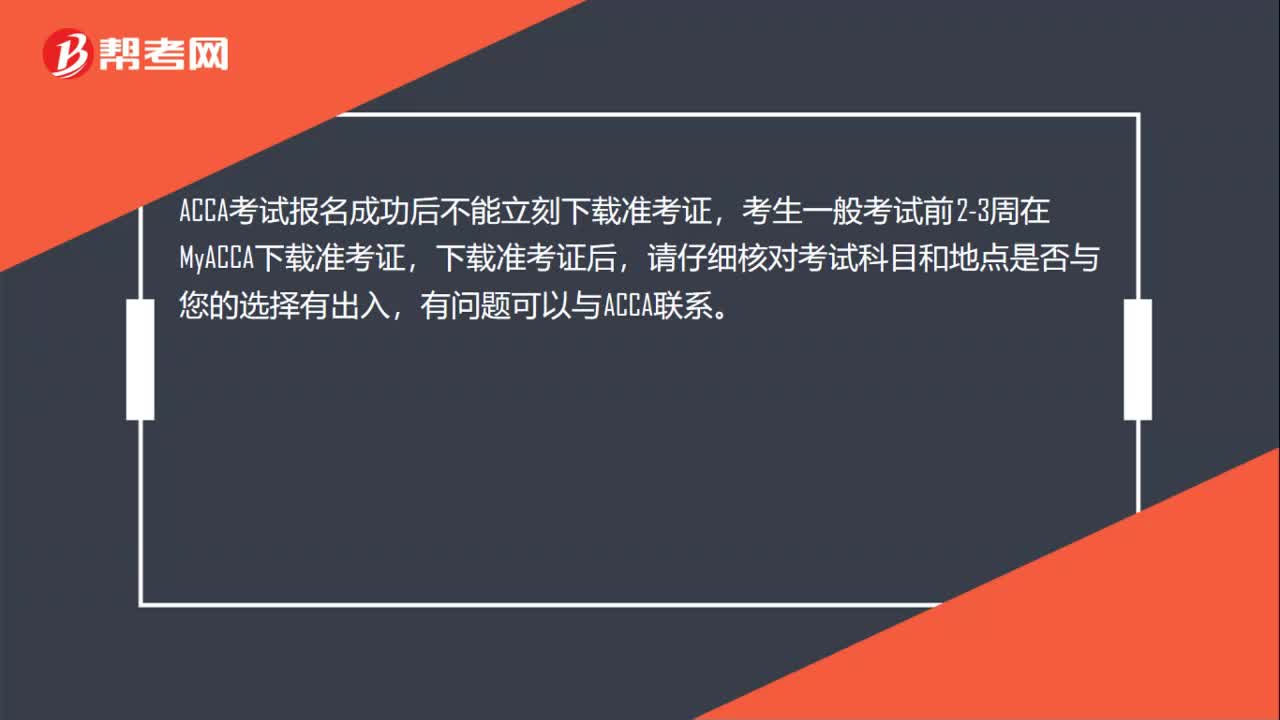

29ACCA考试准考证什么时候打印?:ACCA考试准考证什么时候打印?ACCA考试报名成功后不能立刻下载准考证,考生一般考试前2-3周在知MyACCA下载准考证,下载准考证后,请仔细核对考试科目和地点是否与您的选择有出入,有问题可以与ACCA联系。

20

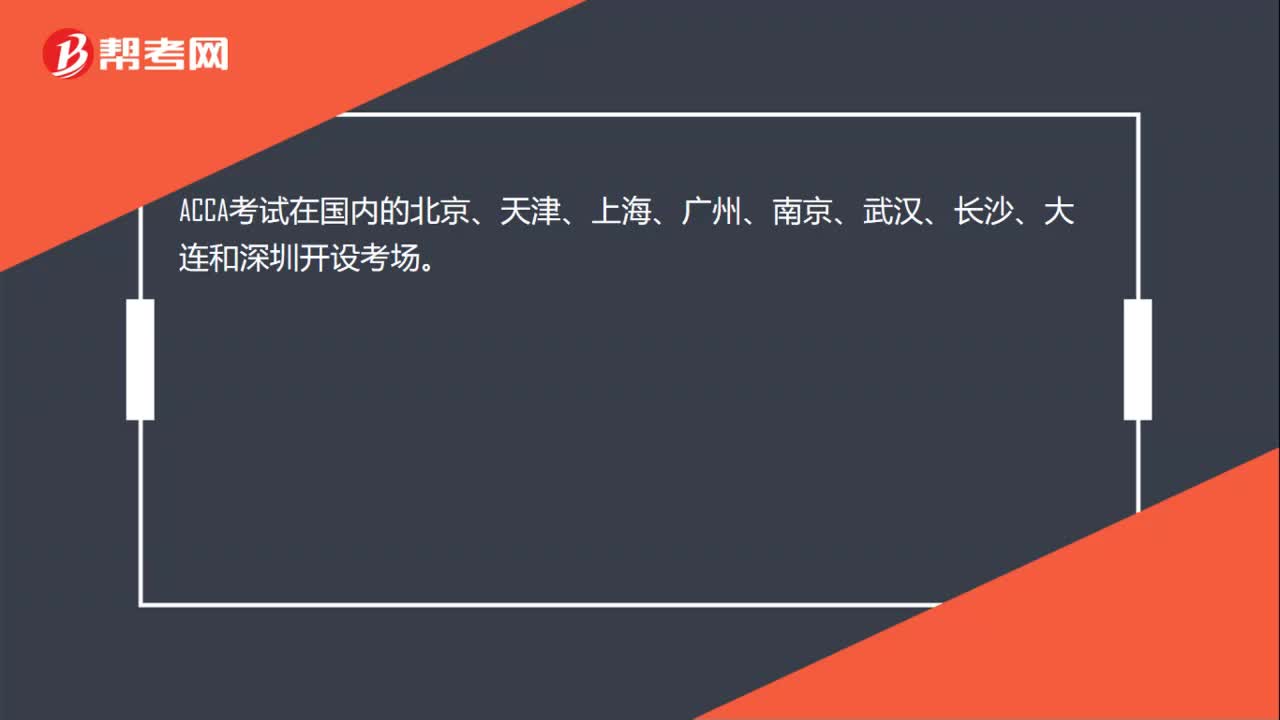

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

42

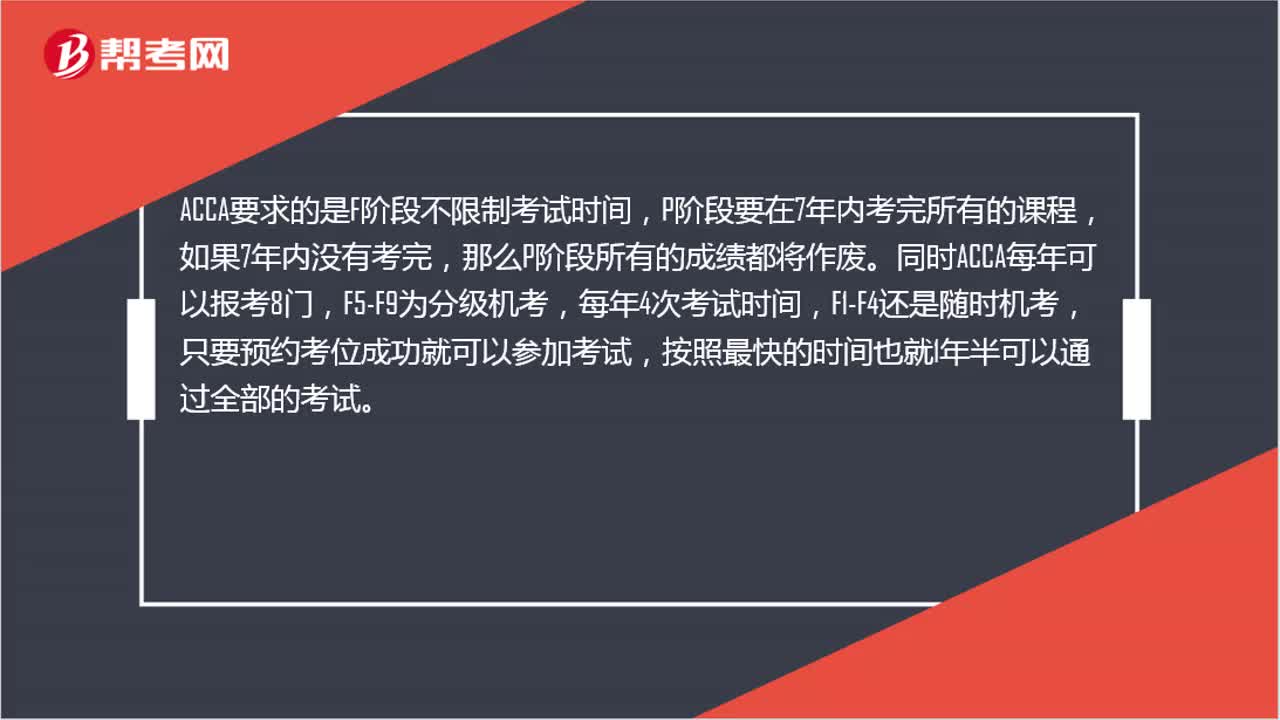

42ACCA考试需要几年才能拿到证书?:ACCA考试需要几年才能拿到证书?ACCA要求的是F阶段不限制考试时间,P阶段要在7年内考完所有的课程,如果7年内没有考完,那么P阶段所有的成绩都将作废。同时ACCA每年可以报考8门,F5-F9为分级机考,每年4次考试时间,F1-F4还是随时机考,只要预约考位成功就可以参加考试,按照最快的时间也就1年半可以通过全部的考试。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料