下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

各位小伙伴注意了,今天帮考网为大家分享2020年ACCA考试审计与认证业务(基础)精选考点(4),供大家参考,希望对大家有所帮助。

Audit risk

Candidates studying Paper F8, Audit and Assurance, are required under the syllabus to: ‘Explain the components of audit risk and explain the risks of material misstatement in the financial statements’.

This element of the syllabus has been examined in the last three sessions of Paper F8 – in June 2010, December 2010 and June 2011. However, the performance of candidates has on the whole been unsatisfactory. This article aims to identify the most common mistakes made by candidates as well as clarifying how audit risk questions should be tackled in order to maximize marks.

An example question requirement relating to audit risks is as follows:

Describe the audit risks and explain the auditor’s response to each risk in planning the audit of XYZ Co. Previously examined risk questions have carried a mark allocation of 10 marks.

However, a significant majority of candidates have not passed this part of the question. Common mistakes made include: providing definitions of the audit risk model, even though this was not part of the question requirement.

a lack of understanding of what audit risk is and providing business risks instead not providing an adequate response to the risk. This needs to be from the perspective of the auditor and not from management’s perspective.

a limited range of risks identified, often just focusing on one area such as going concern.

Audit risk definitions

Audit risk is defined as ‘the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated.

Audit risk is a function of the risks of material misstatement and detection risk’. Hence, audit risk is made up of two components – risks of material misstatement and detection risk.

Risk of material misstatement is defined as ‘the risk that the financial statements are materially misstated prior to audit. This consists of two components… inherent risk … control risk.’

Inherent risk is ‘the susceptibility of an assertion about a class of transaction, account balance or disclosure to a misstatement that could be material, either.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

29

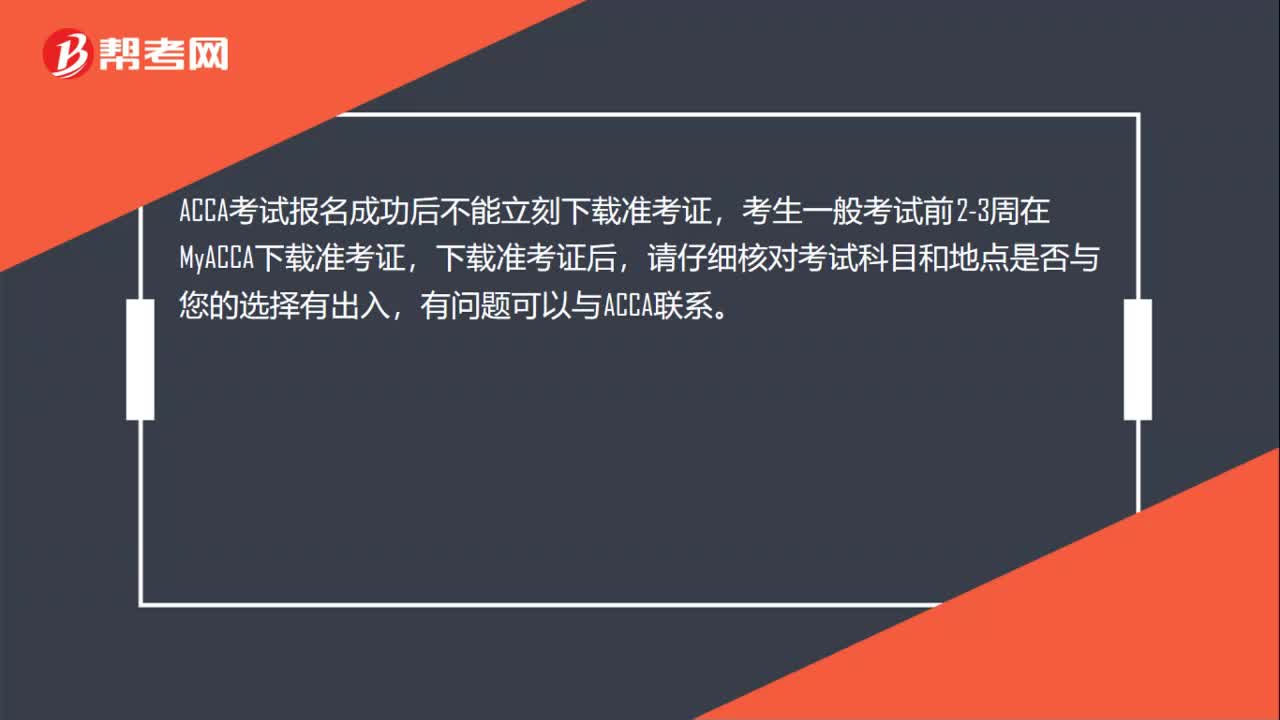

29ACCA考试准考证什么时候打印?:ACCA考试准考证什么时候打印?ACCA考试报名成功后不能立刻下载准考证,考生一般考试前2-3周在知MyACCA下载准考证,下载准考证后,请仔细核对考试科目和地点是否与您的选择有出入,有问题可以与ACCA联系。

20

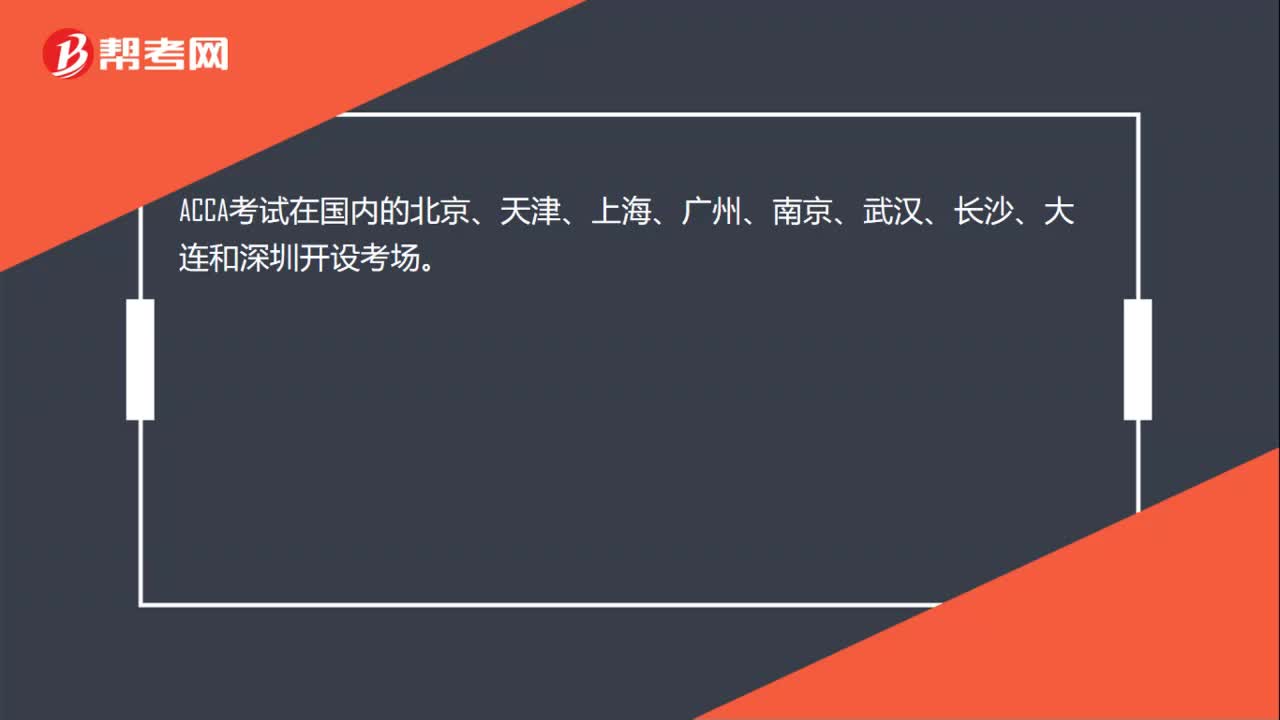

20ACCA考试在中国哪些地方设置了考点?:ACCA考试在国内的北京、天津、上海、广州、南京、武汉、长沙、大连和深圳开设考场。

42

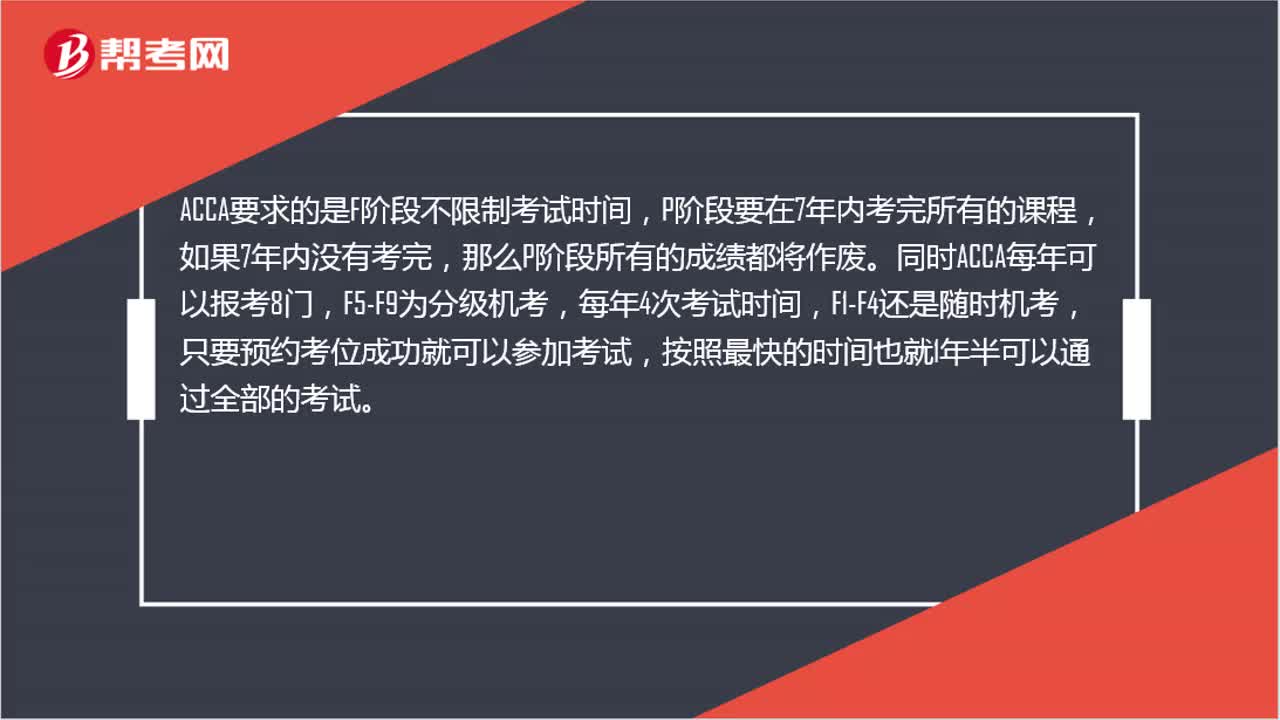

42ACCA考试需要几年才能拿到证书?:ACCA考试需要几年才能拿到证书?ACCA要求的是F阶段不限制考试时间,P阶段要在7年内考完所有的课程,如果7年内没有考完,那么P阶段所有的成绩都将作废。同时ACCA每年可以报考8门,F5-F9为分级机考,每年4次考试时间,F1-F4还是随时机考,只要预约考位成功就可以参加考试,按照最快的时间也就1年半可以通过全部的考试。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料