下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

A tax return preparer is subject to a penalty for knowingly or recklessly disclosing corporate return information, if the disclosure is made:

a. To enable the tax processor to electronically compute the taxpayer's liability.

b. To enable a third party to solicit business from the taxpayer.

c. Under an administrative order by a state agency that registers tax return preparers.

d. For peer review.

答案:B

Explanation

Choice "b" is correct. Use of a taxpayer's return information to assist a third party to solicit business subjects a return preparer to penalty.

Choice "a" is incorrect. Disclosure can properly be made in this case by a return preparer without penalty.

Choice "d" is incorrect. Disclosure can properly be made in this case by a return preparer without penalty.

Choice "c" is incorrect. Disclosure can properly be made in this case by a return preparer without penalty.

22

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

48

482020年AICPA考试多少分合格?:2020年AICPA考试多少分合格?美国注册会计师一共有4门科目,分别是财务会计与报告FAR,商业环境与理论BEC,法律法规REG,审计与鉴证AUD,成绩合格分数线均为75分,单科满分为99分。AICPA已经通过的考试科目单科成绩有效期是18个月,考生必须在通过一门科目后的18个月内考过剩余科目,否则已通过考试成绩也会被作废。

42

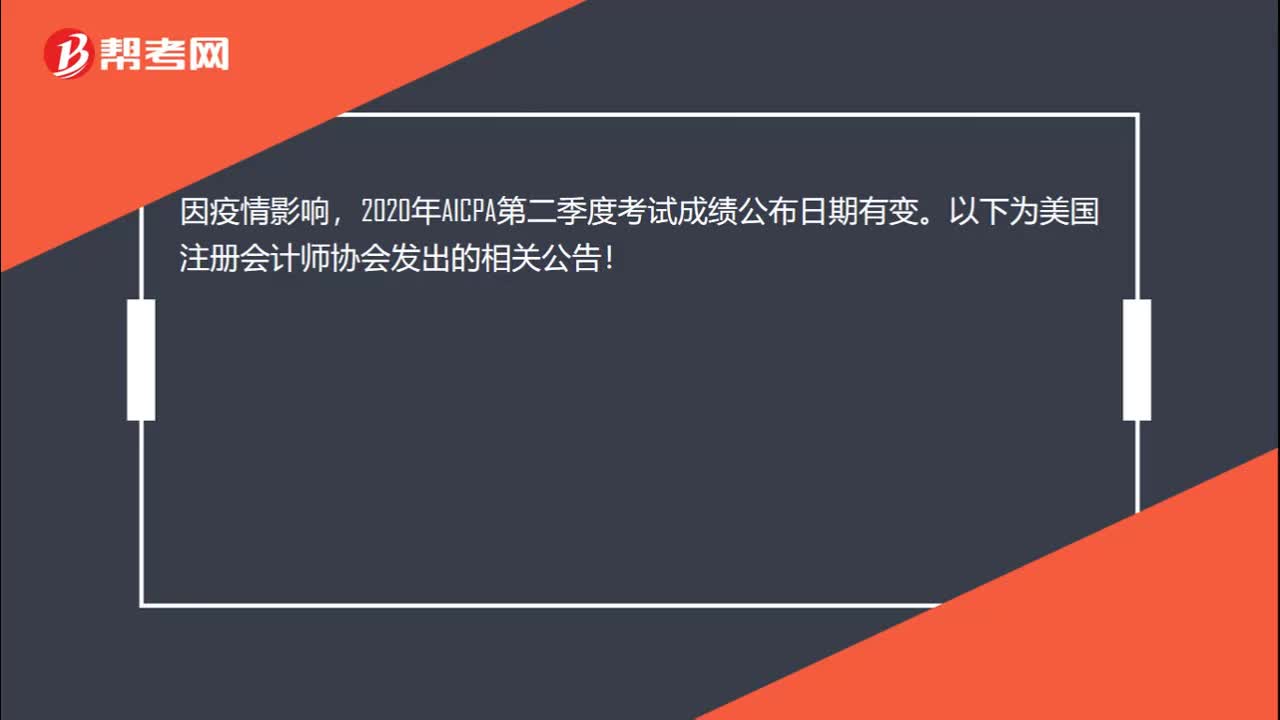

422020年AICPA考试预约考试后多久收到NTS准考证?:2020年AICPA考试预约考试后多久收到NTS准考证?NTS大约需要二到八周才能到达。在大多数州,一旦你收到NTS,它的有效期为六个月,你可以一次申请多个考试科目部分。当你重新申请时,收到你的NTS通常只需要1-2周时间。中国考生申请考试一般需要2-3个月的时间,取得NTS后,建议考生在考前45天去预约考试日期,以确保能参加考试。

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料