下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

1.Which of the following auditor concerns most likely could be so serious that the auditor concludes that a financial statement audit cannot be performed?

a.Management is dominated by one person who is also the majority stockholder.

b.Management fails to modify prescribed internal controls for changes in information technology.

c.There is a substantial risk of intentional misapplication of accounting principles.

d.Internal control activities requiring segregation of duties are rarely monitored by management.

Explanation

Choice "c" is correct. Intentional misapplication of accounting principles would indicate that management lacks integrity and as a result, the auditor might conclude that a financial statement audit cannot be performed.

Choice "b" is incorrect. Management's failure to modify prescribed internal controls for changes in information technology would preclude the auditor from relying on those controls but would not prevent the auditor from performing a financial statement audit.

Choice "d" is incorrect. If management rarely monitors segregation of duties, the auditor would not rely on that particular control, but this would not prevent the auditor from performing a financial statement audit.

Choice "a" is incorrect. If management is dominated by one person who is also the majority stockholder, the risk of fraudulent financial reporting is increased, but this would not preclude the auditor from performing a financial statement audit.

2.Which of the following factors most likely would cause a CPA to not accept a new audit engagement?

a.The prospective client is unwilling to make all financial records available to the CPA.

b.The prospective client has already completed its physical inventory count.

c.The CPA makes oral inquiries (only) to the predecessor auditor regarding the prior year's audit.

d.The CPA lacks an understanding of the prospective client's operations and industry.

Explanation

Choice "a" is correct. An auditor must consider the availability and adequacy of the client's accounting records and the integrity of management in deciding whether or not to accept a new audit engagement. A prospective client that is unwilling to provide all financial records would give the auditor cause for concern about both of these issues.

Choice "b" is incorrect. The auditor may apply acceptable alternative procedures to audit inventory.

Choice "d" is incorrect. The auditor can accept the engagement and obtain an understanding of the client's operations and industry after acceptance.

Choice "c" is incorrect. The CPA is required to make oral or written inquiries of the predecessor auditor before accepting an engagement. Oral inquiries are sufficient here.

66

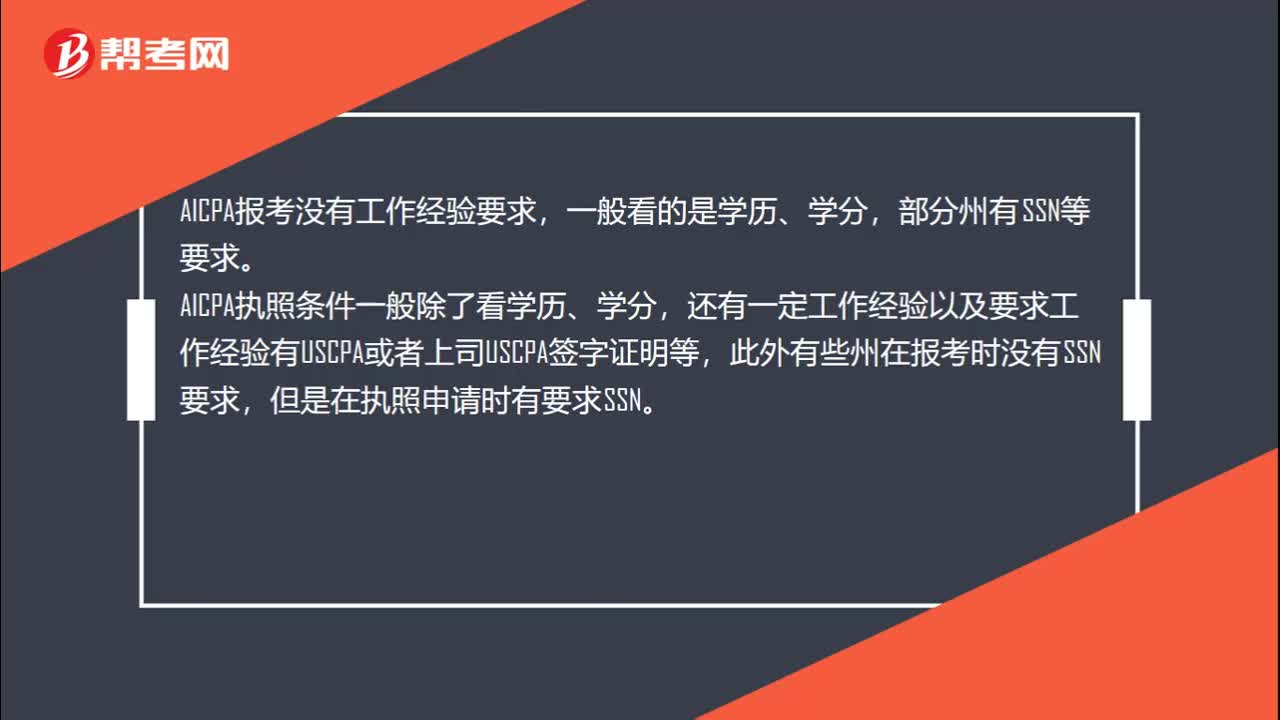

662020年AICPA报考条件和执照申请条件一样吗?:2020年AICPA报考条件和执照申请条件一样吗?AICPA执照申请和报考是两个不同的步骤和环节,AICPA执照和报考要求也是不同的,所以能报考的州并不一定是适合申请执照的。AICPA报考没有工作经验要求,一般看的是学历、学分,部分州有SSN等要求。AICPA执照条件一般除了看学历、学分,还有一定工作经验以及要求工作经验有USCPA或者上司USCPA签字证明等,此外有些州在报考时没有SSN要求。

86

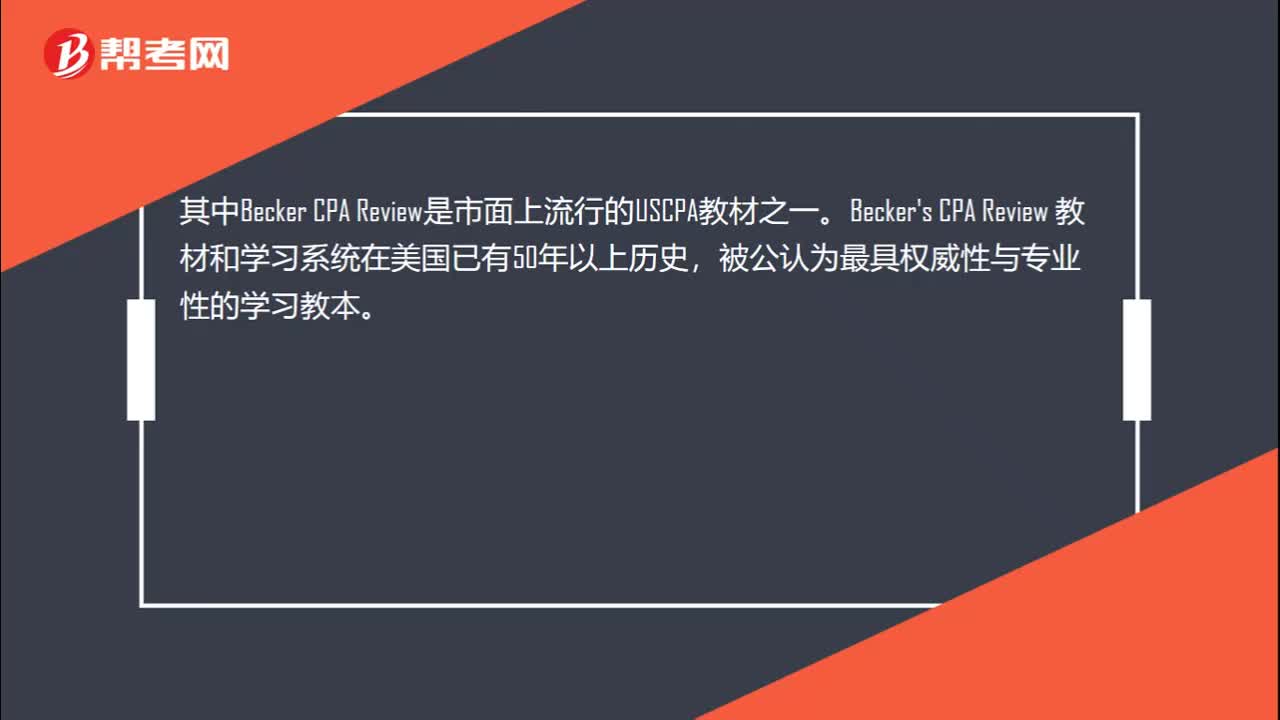

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

22

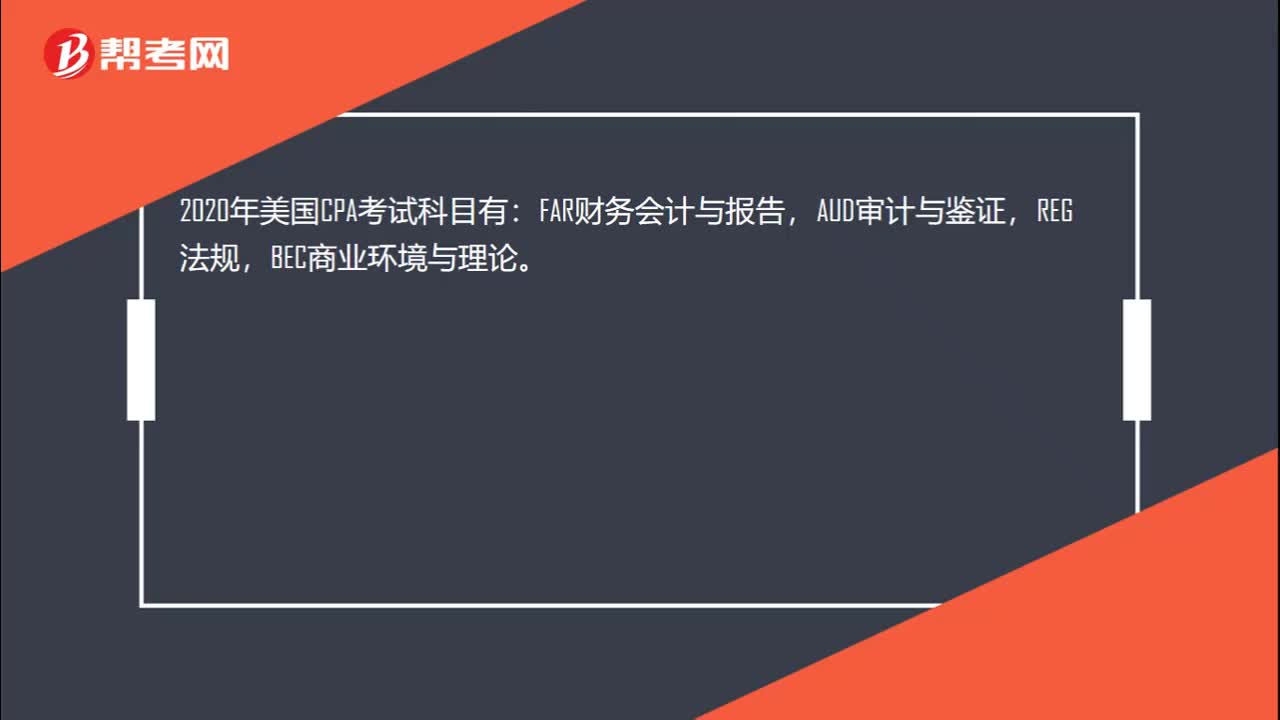

222020年美国CPA考哪些科目?:2020年美国CPA考哪些科目?2020年美国CPA考试科目有:FAR财务会计与报告,AUD审计与鉴证,REG法规,BEC商业环境与理论。共有3种考试题型:分别是选择题,案例分析题,写作题。不同科目题型分配不同,FAR,AUD,REG都是有50%的选择题和50%的案例分析题组成,另外BEC还有个写作题,其BEC题型是由50%的选择+35%的案例分析+15%的写作题组成。

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料