下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

众所周知USCPC考试一共有四门科目,为了帮助大家更好的备考USCPA,帮考网今天给大家分享下软件研发费用资本化知识点的相关分享,接下来就一起去了解下吧!

Software capitalization involves the recognition of internally-developed software as fixed assets. Software is considered to be for internal use when it has been acquired or developed only for the internal needs of a business. Examples of situations where software is considered to be developed for internal use are:

Accounting systems

Cash management tracking systems

Membership tracking systems

Production automation systems

Further, there can be no reasonably possible plan to market the software outside of the company. A market feasibility study is not considered a reasonably possible marketing plan. However, a history of selling software that had initially been developed for internal use creates a reasonable assumption that the latest internal-use product will also be marketed for sale outside of the company.

Software Capitalization Accounting Rules

The accounting for internal-use software varies, depending upon the stage of completion of the project. The relevant accounting is:

Stage 1: Preliminary. All costs incurred during the preliminary stage of a development project should be charged to expense as incurred. This stage is considered to include making decisions about the allocation of resources, determining performance requirements, conducting supplier demonstrations, evaluating technology, and supplier selection.

Stage 2: Application development. Capitalize the costs incurred to develop internal-use software, which may include coding, hardware installation, and testing. Any costs related to data conversion, user training, administration, and overhead should be charged to expense as incurred. Only the following costs can be capitalized:

---Materials and services consumed in the development effort, such as third party development fees, software purchase costs, and travel costs related to development work.

---The payroll costs of those employees directly associated with software development.

---The capitalization of interest costs incurred to fund the project.

Stage 3. Post-implementation. Charge all post-implementation costs to expense as incurred. Samples of these costs are training and maintenance costs.

Any allowable capitalization of costs should begin after the preliminary stage has been completed, management commits to funding the project, it is probable that the project will be completed, and the software will be used for its intended function.

The capitalization of costs should end when all substantial testing has been completed. If it is no longer probable that a project will be completed, stop capitalizing the costs associated with it, and conduct impairment testing on the costs already capitalized. The cost at which the asset should then be carried is the lower of its carrying amount or fair value (less costs to sell). Unless there is evidence to the contrary, the usual assumption is that uncompleted software has no fair value.

以上就是帮考网给大家带来的全部内容,希望能够帮到大家!后续请大家持续关注帮考网,帮考网将会为大家持续更新最新、最热的考试资讯!

66

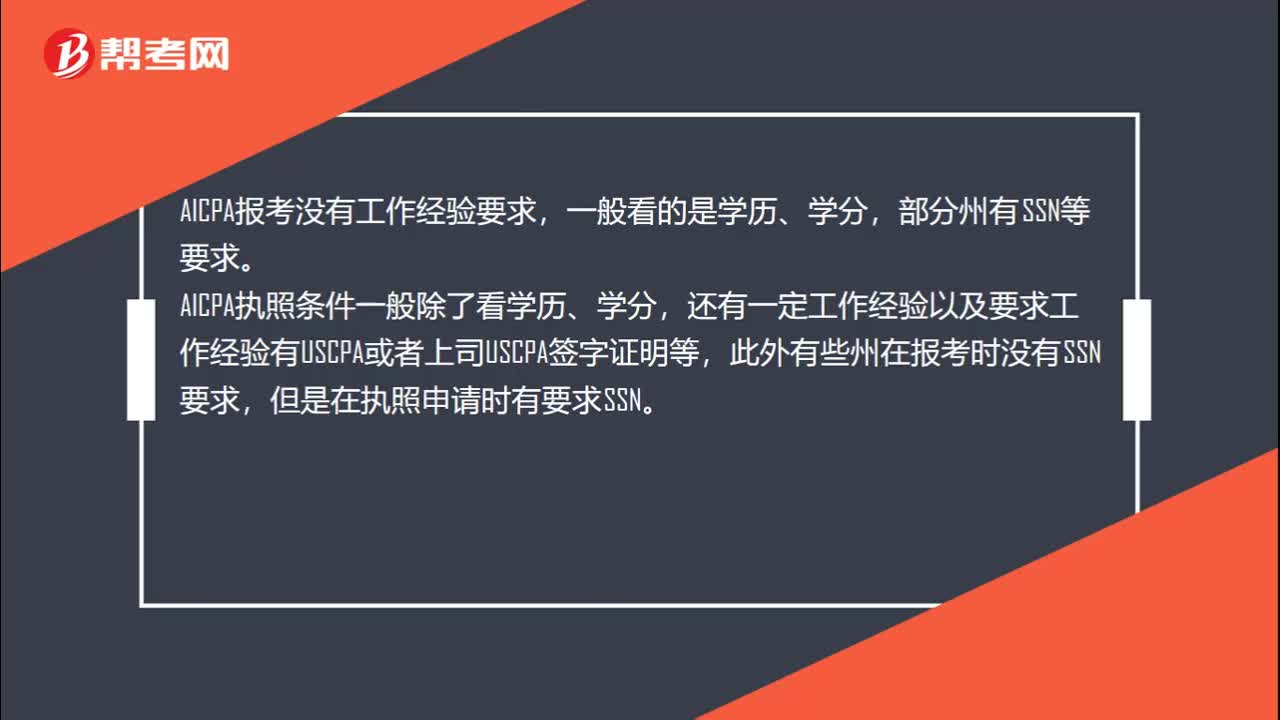

662020年AICPA报考条件和执照申请条件一样吗?:2020年AICPA报考条件和执照申请条件一样吗?AICPA执照申请和报考是两个不同的步骤和环节,AICPA执照和报考要求也是不同的,所以能报考的州并不一定是适合申请执照的。AICPA报考没有工作经验要求,一般看的是学历、学分,部分州有SSN等要求。AICPA执照条件一般除了看学历、学分,还有一定工作经验以及要求工作经验有USCPA或者上司USCPA签字证明等,此外有些州在报考时没有SSN要求。

86

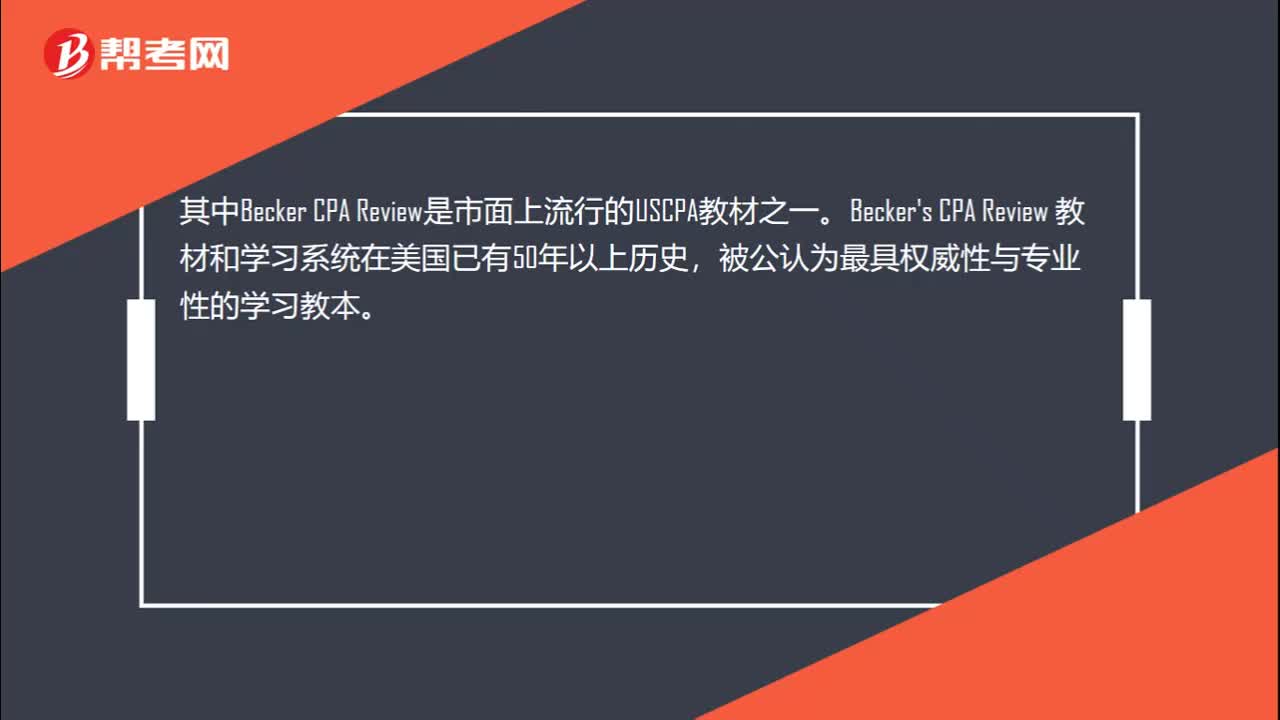

862020年AICPA考试用什么教材学习?:2020年AICPA考试用什么教材学习?在美国有数百种AICPA考试的辅导书籍或资料,Becker's CPA Review 教材和学习系统在美国已有50年以上历史,使用Becker教材通过美国注册会计师考试的人数是未使用该教材人数的两倍;75%的考试通过者、90%的一次通过者以及95%的高分区学员皆选用Becker教材。美国各地超过70多所大学院校选择Becker教材作为他们的课程。

48

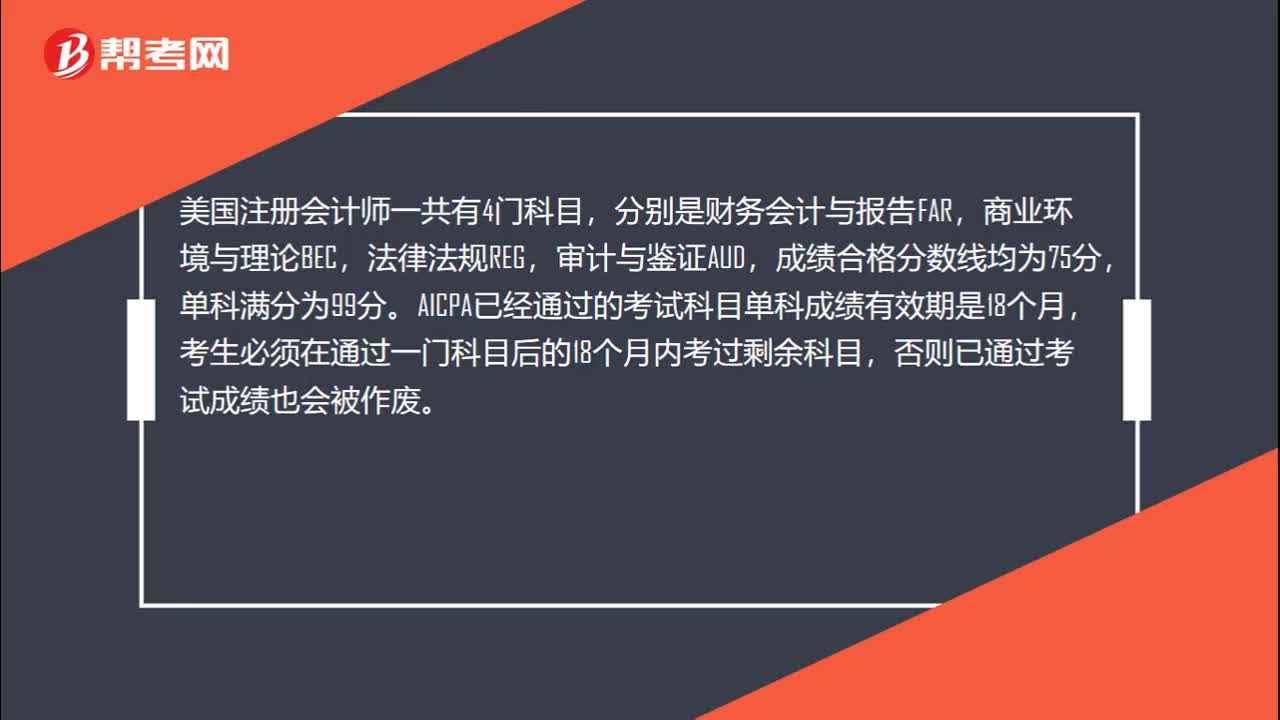

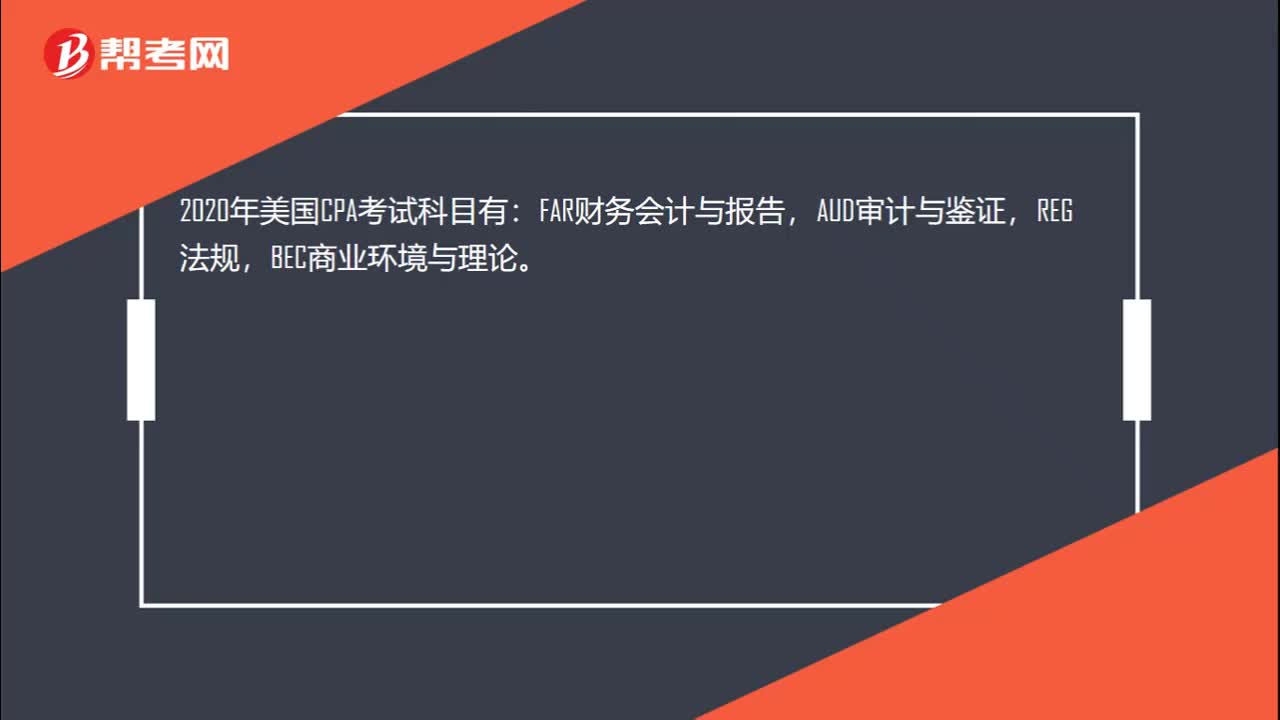

482020年AICPA考试多少分合格?:2020年AICPA考试多少分合格?美国注册会计师一共有4门科目,分别是财务会计与报告FAR,商业环境与理论BEC,法律法规REG,审计与鉴证AUD,成绩合格分数线均为75分,单科满分为99分。AICPA已经通过的考试科目单科成绩有效期是18个月,考生必须在通过一门科目后的18个月内考过剩余科目,否则已通过考试成绩也会被作废。

00:22

00:222020-05-21

01:20

01:202020-05-21

00:25

00:252020-05-21

01:01

01:012020-05-21

00:45

00:452020-05-21

微信扫码关注公众号

获取更多考试热门资料