下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Accounting for defined benefit pension schemes is a complex area of great importance. In some cases, the net pension liability even exceeds the market capitalisation of the company. The financial statements of a company must provide investors,analysts and companies with clear,reliable and comparable information on a company’s pension obligations,discount rates and expected returns on plan assets.

Required:

1.Discuss the current requirements of IAS 19 ‘Employee Benefits’ as regards the accounting for actuarial gains and losses setting out the main criticisms of the approach taken and the advantages of immediate recognition of such gains and losses.

2.Discuss the implications of the current accounting practices in IAS 19 for dealing with the setting of discount rates for pension obligations and the expected returns on plan assets.

86

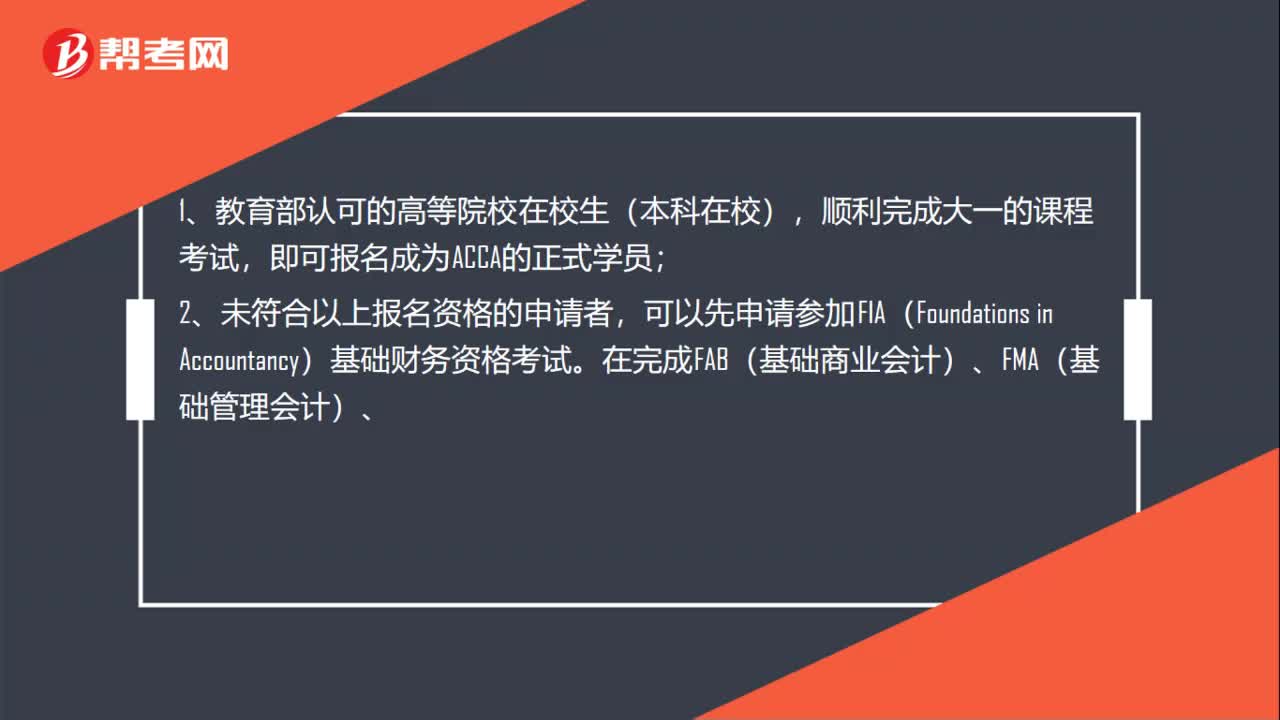

86大专学历可以参加ACCA考试吗?:大专学历可以参加ACCA考试吗?ACCA国际注册会计师考试是一个门槛相对较低的证书,持有国家教育部认可的高等专科院校的毕业证即可参加考试。满足以下条件中的1条也可报名ACCA考试:即可报名成为ACCA的正式学员;可以先申请参加FIA(Foundations in Accountancy)基础财务资格考试。可以豁免ACCA前三门课程的考试。直接进入ACCA技能课程的考试。

49

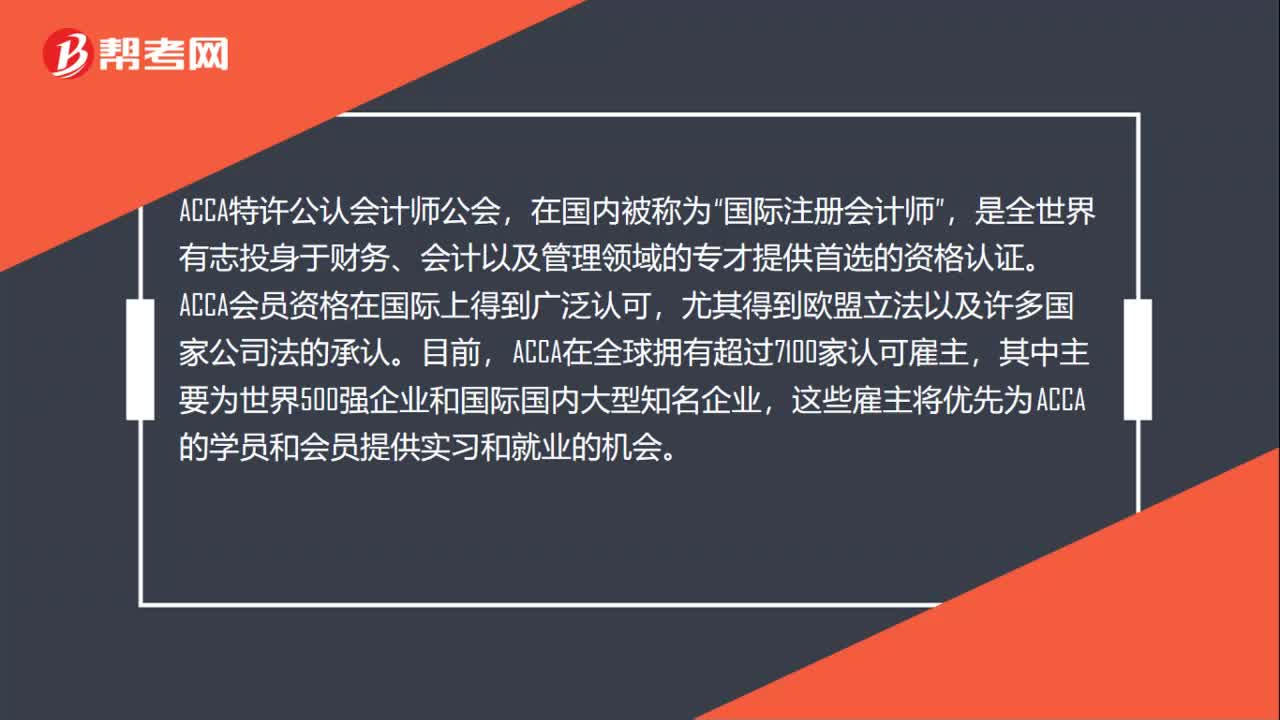

49ACCA证书的含金量高不高?:ACCA证书的含金量高不高?ACCA特许公认会计师公会,在国内被称为“国际注册会计师”是全世界有志投身于财务、会计以及管理领域的专才提供首选的资格认证,ACCA会员资格在国际上得到广泛认可。尤其得到欧盟立法以及许多国家公司法的承认,目前。ACCA在全球拥有超过7100家认可雇主,其中主要为世界500强企业和国际国内大型知名企业,这些雇主将优先为ACCA的学员和会员提供实习和就业的机会。

25

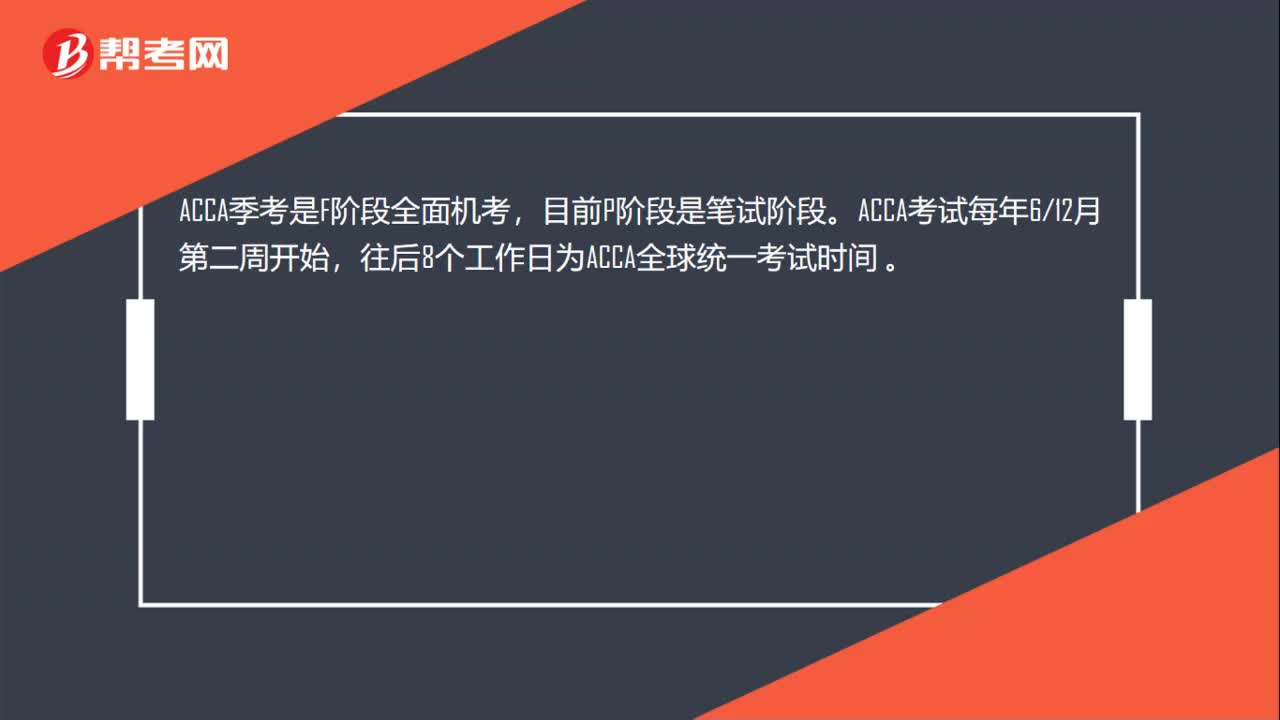

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料