下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Required:

(A)Briefly discuss how the fair value of financial instruments is determined,commenting on the relevance of fair value measurements for financial instruments where markets are volatile and illiquid. (4 marks)

(B)Further they would like advice on accounting for the following transactions within the financial statements for the year ended 31 May 2009:

Aron issued one million convertible bonds on 1 June 2006. The bonds had a term of three years and were issued with a total fair value of $100 million which is also the par value. Interest is paid annually in arrears at a rate of 6% per annum and bonds,without the conversion option,attracted an interest rate of 9% per annum on 1 June 2006. The company incurred issue costs of $1 million. If the investor did not convert to shares they would have been redeemed at par. At maturity all of the bonds were converted into 25 million ordinary shares of $1 of Aron. No bonds could be converted before that date. The directors are uncertain how the bonds should have been accounted for up to the date of the conversion on 31 May 2009 and have been told that the impact of the issue costs is to increase the effective interest rate to 9·38%.

86

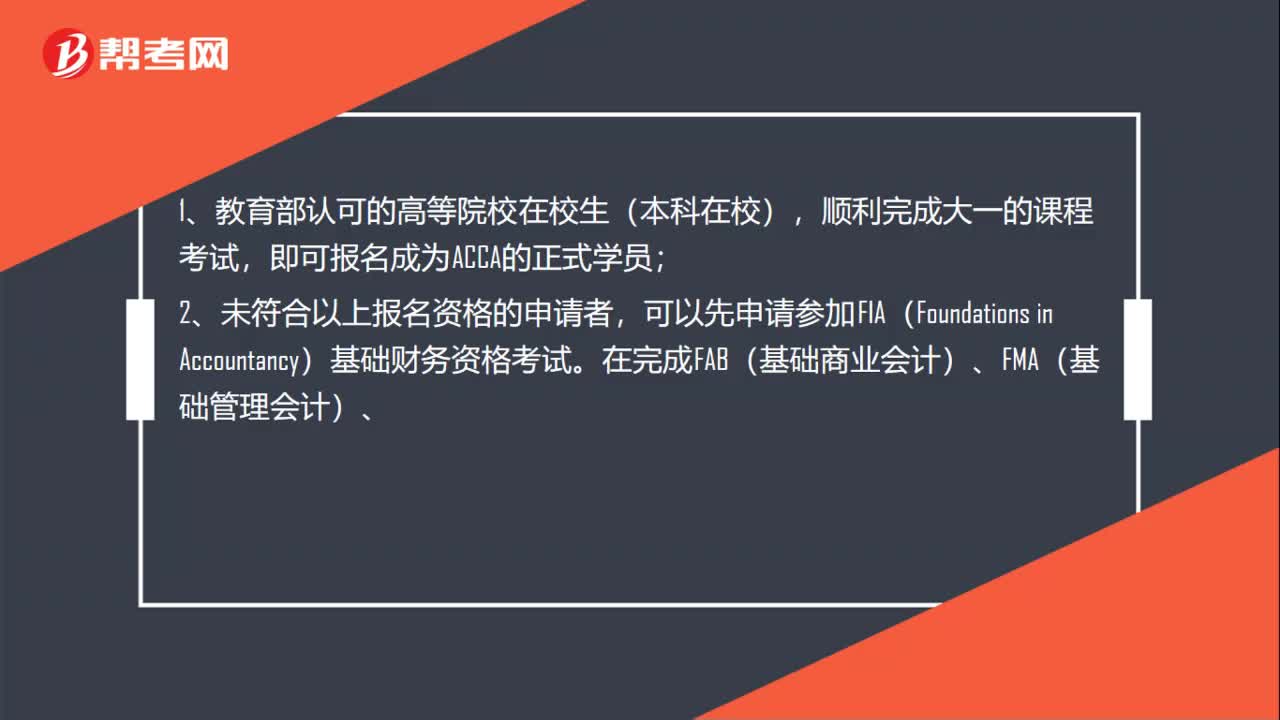

86大专学历可以参加ACCA考试吗?:大专学历可以参加ACCA考试吗?ACCA国际注册会计师考试是一个门槛相对较低的证书,持有国家教育部认可的高等专科院校的毕业证即可参加考试。满足以下条件中的1条也可报名ACCA考试:即可报名成为ACCA的正式学员;可以先申请参加FIA(Foundations in Accountancy)基础财务资格考试。可以豁免ACCA前三门课程的考试。直接进入ACCA技能课程的考试。

64

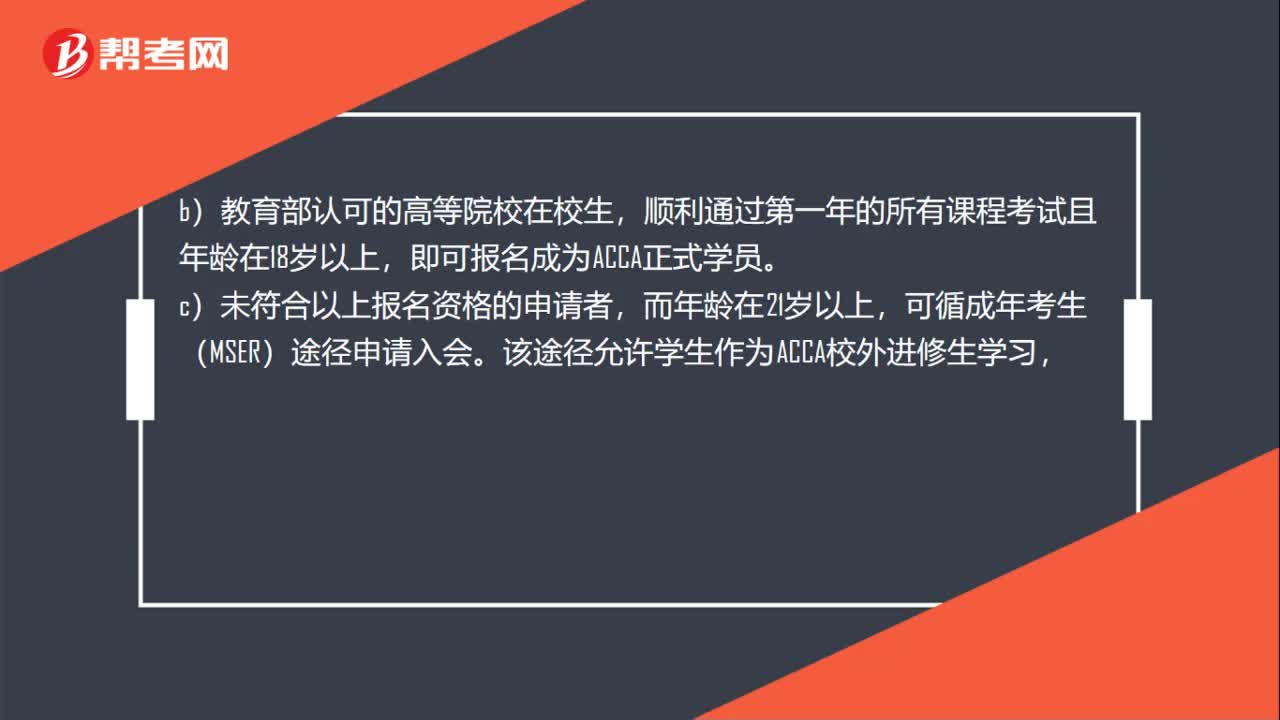

64ACCA是什么专业都可以考的吗?:ACCA是什么专业都可以考的吗?ACCA报名是不限制专业条件的。ACCA考试入学资格:1.凡具有教育部认可的大专以上学历的申请者,2.教育部认可的高等院校在校生,顺利通过第一年的所有课程考试且年龄在18岁以上,即可报名成为ACCA正式学员。3.未符合以上报名资格的申请者,可循成年考生(MSER)途径申请入会。该途径允许学生作为ACCA校外进修生学习。

25

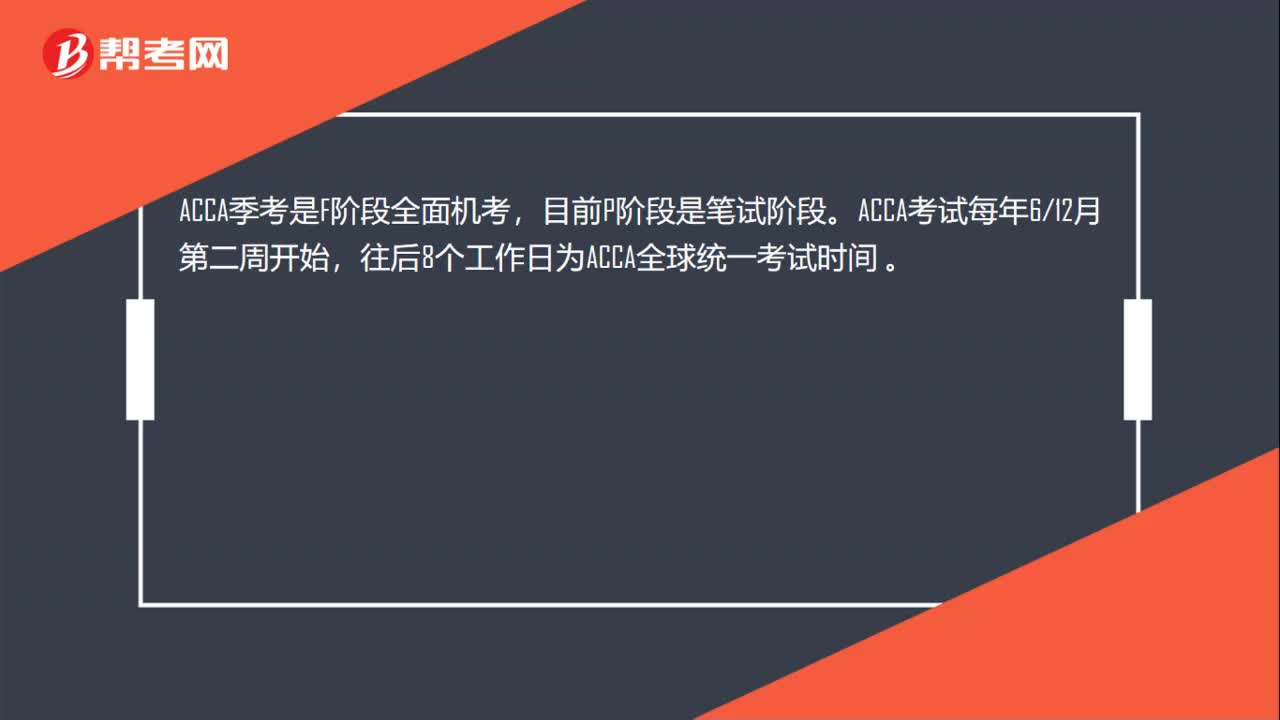

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料