当前位置: 首页ACCA考试财务报告(基础阶段)技巧心得正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

今日帮考网为大家带来“备考资料:2020年ACCA考试FR财务报告知识点(6)”的相关知识点,各位辛勤备考的小伙伴一起来看看吧。

【知识点】Other Government assistance其他政府援助

Other Government assistance

Some forms of government assistance are excluded from the definition of government grants.

(a) Some forms of government assistance cannot reasonably have a value placed on them, e.g. free technical or marketing advice, provision of guarantees.

(b) There are transactions with government which cannot be distinguished from the entity\'s normal trading transactions, e.g. government procurement policy resulting in a portion of the entity\'s sales. Any segregation would be arbitrary.

Disclosure of such assistance may be necessary because of its significance;Its nature, extent and duration should be disclosed.

【知识点】Development costs开发成本

Development costs

Development costs may qualify for recognition as intangible assets provided that the following strict criteria can be demonstrated.

a) The technical feasibility of completing the intangible asset so that it will be available for use or sale.

b) Its intention to complete the intangible asset and use or sell it.

c) Its ability to use or sell the intangible asset.

d) How the intangible asset will generate probable future economic benefits. The entity should demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself.

e) Its ability to measure the expenditure attributable to the intangible asset during its development reliably.

f) Resources adequate and available to complete.

【知识点】Indicators of impairment 减值指标

Indicators of impairment

External sources of information

A fall in the asset\'s market value that is more significant than would normally be expected from passage of time over normal use.

A significant change in the technological, market, legal or economic environment of the business in which the assets are employed.

An increase in market interest rates or market rates of return on investments likely to affect the discount rate used in calculating value in use.

The carrying amount of the entity\'s net assets being more than its market capitalization.

Internal sources of information

evidence of obsolescence or physical damage, adverse changes in the use to which the asset is put, or the asset\'s economic performance.

No indications of impairment

Even if there are no indications of impairment, the following assets must always be tested for impairment annually.

An intangible asset with an indefinite useful life.

Goodwill acquired in a business combination.

以上就是帮考网带给大家的全部内容,相信小伙伴们都了解清楚。预祝12月份ACCA考试取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注帮考网!

63

63ACCA报考有年龄限制吗?:ACCA报考有年龄限制吗?ACCA报考是没有年龄限制的,报名参加ACCA考试,1.凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;顺利完成了大一全年的所有课程考试,专即可报名成为ACCA的正式学员;3.未符合1、2项报名资格的申请者,可以先申请参加FIA资格考试,通过FFA、FMA和FAB三门课程后,可以申请转入ACCA并且豁免F1-F3三门课程的考试。

44

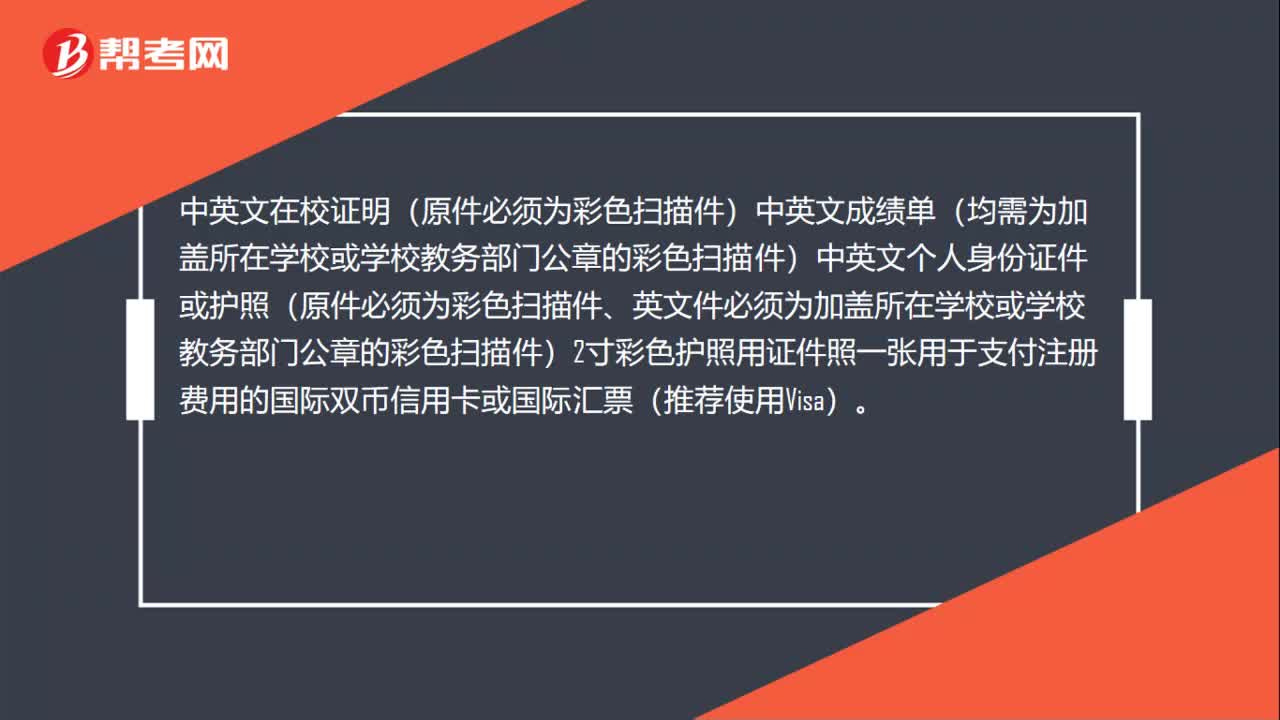

44报考ACCA需要准备什么?:中英文在校证明(原件必须为彩色扫描件)中英文成绩单(均需为加盖所在学校或学校教务部门公章的彩色扫描件)中英文个人身份证件或护照(原件必须为彩色扫描件、英文件必须为加盖所在学校或学校教务部门公章的彩色扫描件)2寸彩色护照用证件照一张用于支付注册费用的国际双币信用卡或国际汇票(推荐使用Visa)。

22

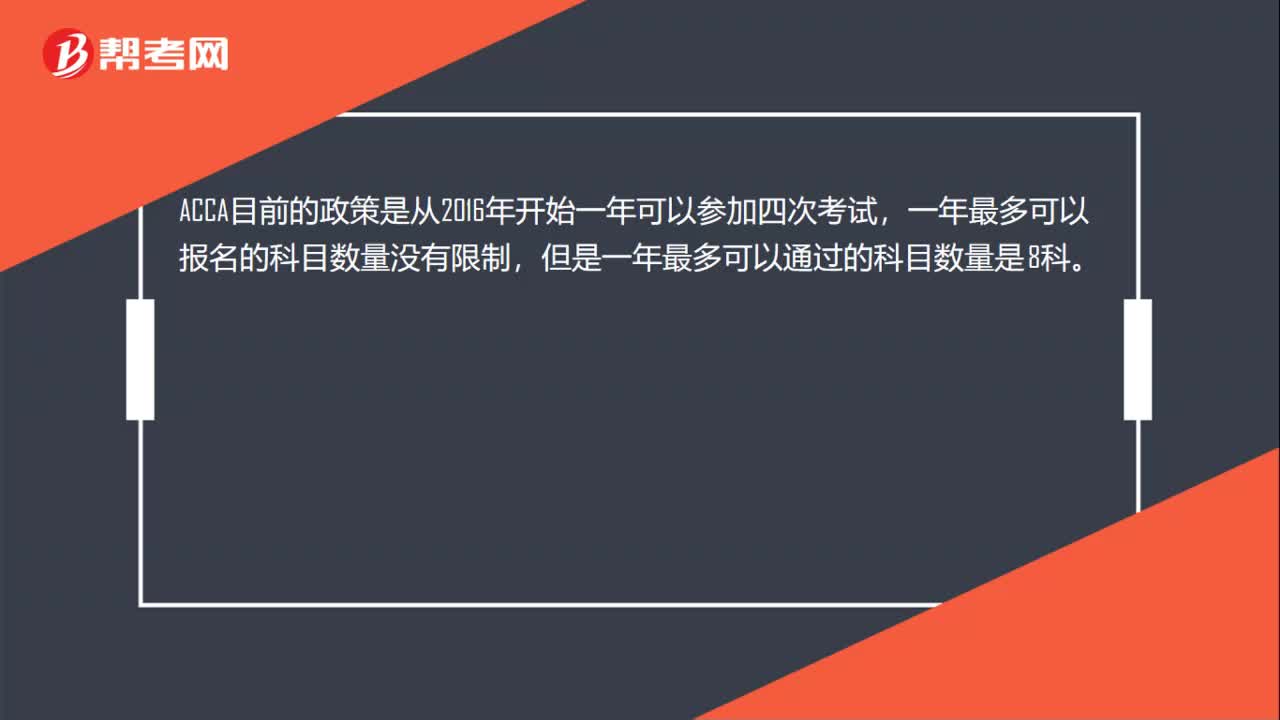

22ACCA考试一次最多可以报考几门?:ACCA考试一次最多可以报考几门?ACCA目前的政策是从2016年开始一年可以参加四次考试,一年最多可以报名的科目数量没有限制,但是一年最多可以通过的科目数量是8科。

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料