下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

各位小伙伴大家好!想要报考ACCA考试的小伙伴请注意啦,帮考网为大家带来了考试练习题供大家练习,帮助大家熟悉题型和巩固知识。

(a)Accounting fordefined benefit pension schemes is a complex area of great importance. In some cases, the net pension liability even exceeds the market capitalisation of the company. The financial statements of a company must provide investors,analysts and companies with clear,reliable and comparable information on a company’s pension obligations,discount rates and expected returns on plan assets.

Required:

(i) Discuss the current requirements of IAS 19 ‘Employee Benefits’ as regards the accounting foractuarial gains and losses setting out the main criticisms of the approach taken and the advantages of immediate recognition of such gains and losses. (11 marks)

(ii) Discuss the implications of the current accounting practices in IAS 19 fordealing with the setting of discount rates forpension obligations and the expected returns on plan assets. (6 marks)

Professional marks will be awarded in part (a) forclarity and quality of discussion. (2 marks)

(b) Smith,a public limited company and Brown a public limited company utilise IAS 19 ‘Employee Benefits’ to account fortheir pension plans. The following information refers to the company pension plans forthe year to 30 April 2009:

(i)At 1 May 2008,plan assets of both companies were fair valued at $200 million and both had net unrecognised actuarial gains of $6 million.

(ii)At 30 April 2009,the fair value of the plan assets of Smith was $219 million and that of Brown was $276 million.

(iii)The contributions received were $70 million and benefits paid were $26 million forboth companies. These amounts were paid and received on 1 November 2008.

(iv)The expected return on plan assets was 7% at 1 May 2008 and 8% on 30 April 2009.

(v)The present value of the defined benefit obligation was less than the fair value of the plan assets at both 1 May 2008 and 30 April 2009.

(vi)Actuarial losses on the obligation forthe year were negligible forboth companies.

(vii)Both companies use the corridorapproach to recognised actuarial gains and losses.

Required:

Show how the use of the expected return on assets can cause comparison issues forpotential investors using the above scenario forillustration. (6 marks)

(25 marks)

ALL TEN questions are compulsory and MUST be attempted

1 In relation to the Civil Procedure Law of China:

(a)explain the term exclusive jurisdiction;(2 marks)

(b)state the majorlegal characteristics of exclusive jurisdiction,in terms of:

(i)the basis of exclusive jurisdiction;and (4 marks)

(ii)the effect of the rule of exclusive jurisdiction.(4 marks)

(10 marks)

2 In relation to the Property Law of China:

(a)explain the term right of lien;(4 marks)

(b)state THREE conditions to be met fora party to claim the right of lien.(6 marks)

(10 marks)

3 In relation to the Labour Contract Law of China:

(a) state the various powers of the labour administration in exercising its supervisory and examining functions;(2 marks)

(b) state any FOUR kinds of situations under which the labour administration may issue administrative orders to an employer forviolations of Labour Contract Law.(8 marks)

(10 marks)

4 In relation to the Contract Law of China:

(a)explain the term termination of contract;(2 marks)

(b)explain and distinguish between termination of contract and dissolution of contract.(8 marks)

(10 marks)

5 In relation to the Company Law of China:

(a)state the basic rules regarding the shareholders of:

(i)a general limited liability company;(2 marks)

(ii)a sole-person limited liability company and a wholly state-owned company;and(2 marks)

(b)state the requirements forcapital of:

(i)a general limited liability company;(2 marks)

好了,今天的分享就到这里结束啦!大家今天是否有所收获呢?如需了解更多相关内容,请关注帮考网!

80

80ACCA考试难度大吗?:ACCA考试难度大吗?ACCA考试的难度是以英国大学学位考试的难度为标准,第一(f1-f3)、第二部分(f4-f9)的难度分别相当于学士学位高年级课程的考试难度,第三部分p阶段的考试相当于硕士学位最后阶段的考试。第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。第二部分的考试除了本门课程的内容之外。

56

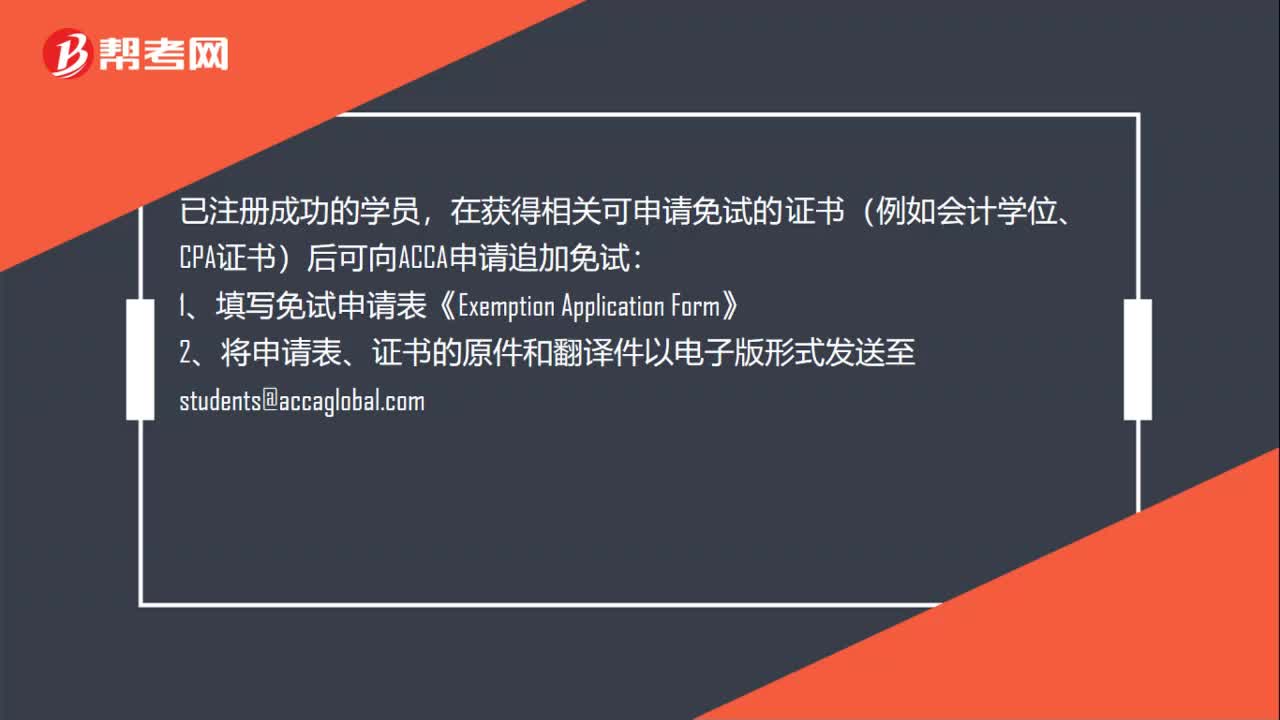

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

12

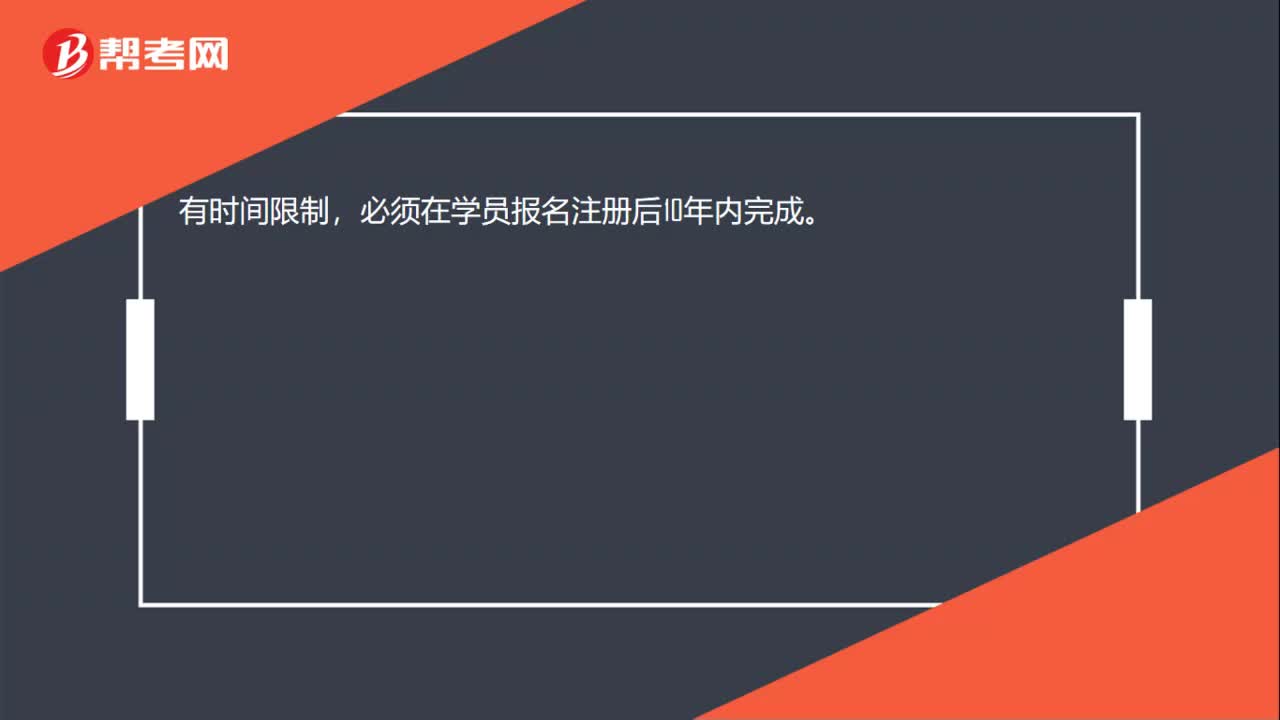

12ACCA考试有时间限制吗?:ACCA考试有时间限制吗?有时间限制,必须在学员报名注册后10年内完成。

01:03

01:032020-06-04

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料