当前位置: 首页ACCA考试财务报告(基础阶段)模拟试题正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

为了帮助备考ACCA考试的小伙伴更好的备考,下面帮考网就分享给大家一些ACCA考试F7考试模拟试题,感兴趣的小伙伴赶紧来练习吧。

The following scenario relates to questions 1–5.

On 1 January 20X5, Blocks Co entered into new lease agreements as follows:

Agreement one This finance lease relates to a new piece of machinery. The fair value of the machine is $220,000. The agreement requires Blocks Co to pay a deposit of $20,000 on 1 January 20X5 followed by five equal annual instalments of $55,000, starting on 31 December 20X5. The implicit rate of interest is 11·65%.

Agreement two This three-year operating lease relates to a fleet of vans. The fair value of the vans is $120,000 and they have an estimated useful life of five years. The agreement requires Blocks Co to make no payment in year one and $48,000 in years two and three.

Agreement three This sale and leaseback relates to a cutting machine purchased by Blocks Co on 1 January 20X4 for $300,000. The carrying amount of the machine as at 31 December 20X4 was $250,000. On 1 January 20X5, it was sold to Cogs Co for $370,000 and Blocks Co will lease the machine back for five years, the remainder of its useful life, at $80,000 per annum.

1 According to IAS 17 Leases, which of the following is generally considered to be a characteristic of an operating, rather than a finance, lease?

A Ownership of the assets is passed to the lessee by the end of the lease term

B The lessor is responsible for the general maintenance and repair of the assets

C The present value of the lease payments is approximately equal to the fair value of the asset

D The lease term is for a major part of the useful life of the asset

答案:B

2 For agreement one, what is the finance cost charged to profit or loss for the year ended 31 December 20X6?

A $23,300

B $12,451

C $19,607

D $16,891

答案:C

3 The following calculations have been prepared for agreement one:

Year Interest Annual payment Balance

$ $ $

31 December 20X7 15,484 (55,000) 93,391

31 December 20X8 10,880 (55,000) 49,271

31 December 20X9 5,729 (55,000) 0

How will the finance lease obligation be shown in the statement of financial position as at 31 December 20X7?

A $44,120 as a non-current liability and $49,271 as a current liability

B $49,271 as a non-current liability and $44,120 as a current liability

C $93,391 as a non-current liability

D $93,391 as a current liability

答案:B

4 For agreement two, what would be the correct statement of profit or loss entries for the year ended 31 December 20X5?

A Depreciation of $24,000 and no lease rental expense

B No depreciation and lease rental expense of $32,000

C Depreciation of $24,000 and lease rental expense of $32,000

D No depreciation and lease rental expense of $48,000

答案:B

5 For agreement three, what profit should be recognised for the year ended 31 December 20X5 as a result of the sale and leaseback?

A $24,000

B $120,000

C $70,000

D $20,000

答案:A

以上就是帮考网分享给大家的ACCA考试试题的内容,希望可以帮助到大家。如果想要了解更多关于ACCA考试的试题,敬请关注帮考网!

80

80ACCA考试难度大吗?:ACCA考试难度大吗?ACCA考试的难度是以英国大学学位考试的难度为标准,第一(f1-f3)、第二部分(f4-f9)的难度分别相当于学士学位高年级课程的考试难度,第三部分p阶段的考试相当于硕士学位最后阶段的考试。第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。第二部分的考试除了本门课程的内容之外。

56

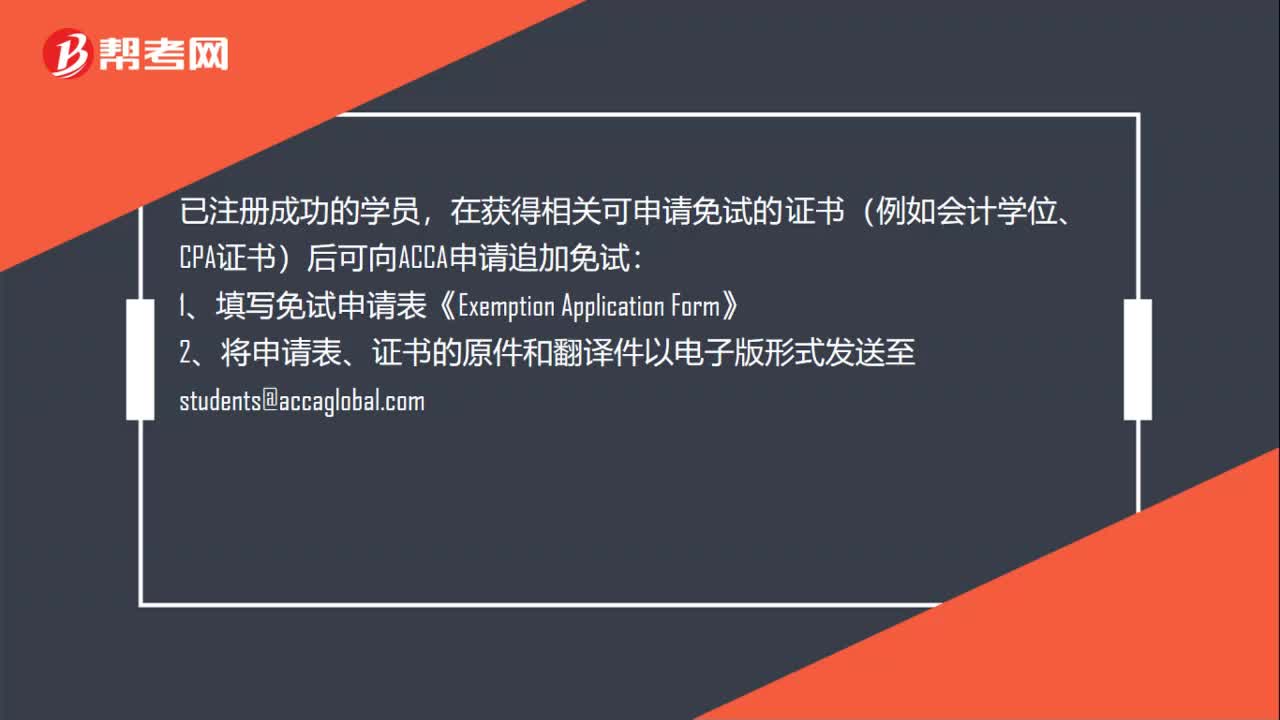

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

66

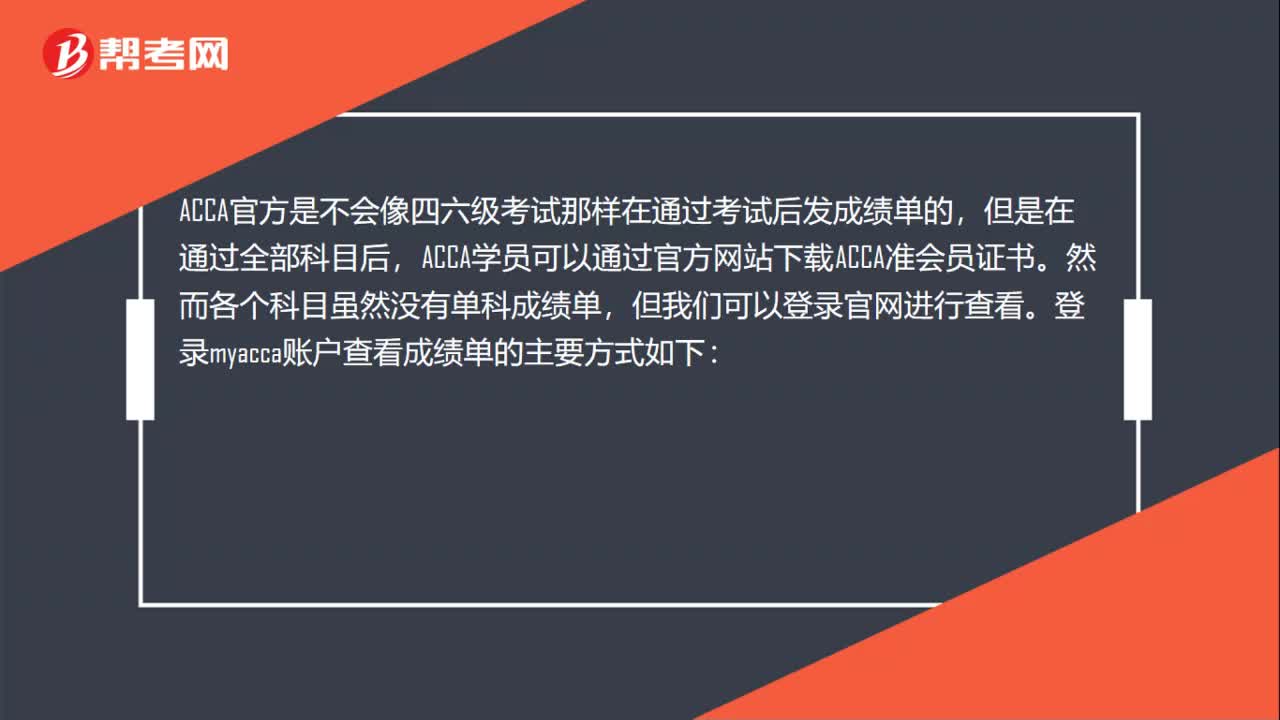

66ACCA考试有成绩单吗?:ACCA考试有成绩单吗?ACCA官方是不会像四六级考试那样在通过考试后发成绩单的,但是在通过全部科目后,ACCA学员可以通过官方网站下载ACCA准会员证书。然而各个科目虽然没有单科成绩单,但我们可以登录官网进行查看。登录myacca账户查看成绩单的主要方式如下:1、登陆ACCA官网accaglobal.com,进入学员个人页面;2、 输入个人的学员注册号码及密码后点击按钮“login”

01:03

01:032020-06-04

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料