当前位置: 首页ACCA考试业绩管理(基础阶段)历年真题正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

Question:

Glove Co makes high quality,hand - made gloves which it sells for an average of $180 per pair. The standard cost of labour for each pair is $42 and the standard labour time for each pair is three hours. In the last quarter,Glove Co had budgeted production of 12,000 pairs,although actual production was 12,600 pairs in order to meet demand. 37,000 hours were used to complete the work and there was no idle time. The total labour cost for the quarter was $531,930.

At the beginning of the last quarter,the design of the gloves was changed slightly. The new design required workers to sew the company‘s logo on to the back of every glove made and the estimated time to do this was 15 minutes for each pair. However,no - one told the accountant responsible for updating standard costs that the standard time per pair of gloves needed to be changed. Similarly,although all workers were given a 2% pay rise at the beginning of the last quarter,the accountant was not told about this either. Consequently,the standard was not updated to reflect these changes.

When overtime is required,workers are paid 25% more than their usual hourly rate.

Required:

(a) Calculate the total labour rate and total labour efficiency variances for the last quarter.

(b) Analyse the above total variances into component parts for planning and operational variances in as much detail as the information allows.

(c) Assess the performance of the production manager for the last quarter.

Answer:

(a) Basic variances

Labour rate variance

Standard cost of labour per hour = $42/3 = $14 per hour.

Labour rate variance = (actual hours paid x actual rate) - (actual hours paid x std rate)

Actual hours paid x actual rate = $531,930.

Actual hours paid x std rate = 37,000 x $14 = $518,000.

Therefore rate variance = $531,930 - $518,000 = $13,930 A

Labour efficiency variance

Labour efficiency variance = (actual production in std hours - actual hours worked) x std rate

[(12,600 x 3) - 37,000] x $14 = $11,200 F

(b) Planning and operational variances

Labour rate planning variance

(Revised rate - std rate) x actual hours paid = [$14·00 – ($14·00 x 1·02)] x 37,000 = $10,360 A.

Labour rate operational variance

Revised rate x actual hours paid =$14·28 x 37,000= $528,360.

Actual cost = $531,930.

Variance = $3,570 A.

Labour efficiency planning variance

(Standard hours for actual production - revised hours for actual production) x std rate

Revised hours for each pair of gloves = 3·25 hours.

[37,800 – (12,600 x 3·25)] x $14 = $44,100 A.

Labour efficiency operational variance

(Revised hours for actual production - actual hours for actual production) x std rate

(40,950 - 37,000) x $14 = $55,300 F.

(c) Analysis of performance

At a first glance,performance looks mixed because the total labour rate variance is adverse and the total labour efficiency variance is favourable. However,the operational and planning variances provide a lot more detail on how these variances have occurred.

The production manager should only be held accountable for variances which he can control. This means that he should only be held accountable for the operational variances. When these operational variances are looked at it can be seen that the labour rate operational variance is $3,570 A. This means that the production manager did have to pay for some overtime in order to meet demand but the majority of the total labour rate variance is driven by the failure to update the standard for the pay rise that was applied at the start of the last quarter. The overtime rate would also have been impacted by that pay increase.

Then,when the labour efficiency operational variance is looked at,it is actually $55,300 F. This shows that the production manager has managed his department well with workers completing production more quickly than would have been expected when the new design change is taken into account. The total operating variances are therefore $51,730 F and so overall performance is good.

The adverse planning variances of $10,360 and $44,100 do not reflect on the performance of the production manager and can therefore be ignored here.

63

63ACCA报考有年龄限制吗?:ACCA报考有年龄限制吗?ACCA报考是没有年龄限制的,报名参加ACCA考试,1.凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;顺利完成了大一全年的所有课程考试,专即可报名成为ACCA的正式学员;3.未符合1、2项报名资格的申请者,可以先申请参加FIA资格考试,通过FFA、FMA和FAB三门课程后,可以申请转入ACCA并且豁免F1-F3三门课程的考试。

19

19没有及时缴纳ACCA年费会有什么影响?:没有及时缴纳ACCA年费会有什么影响?如果会员没有在规定时间内及时支付所欠的费用(包括年费、会员申请费等),ACCA总部将在当年把会员进行除名。

64

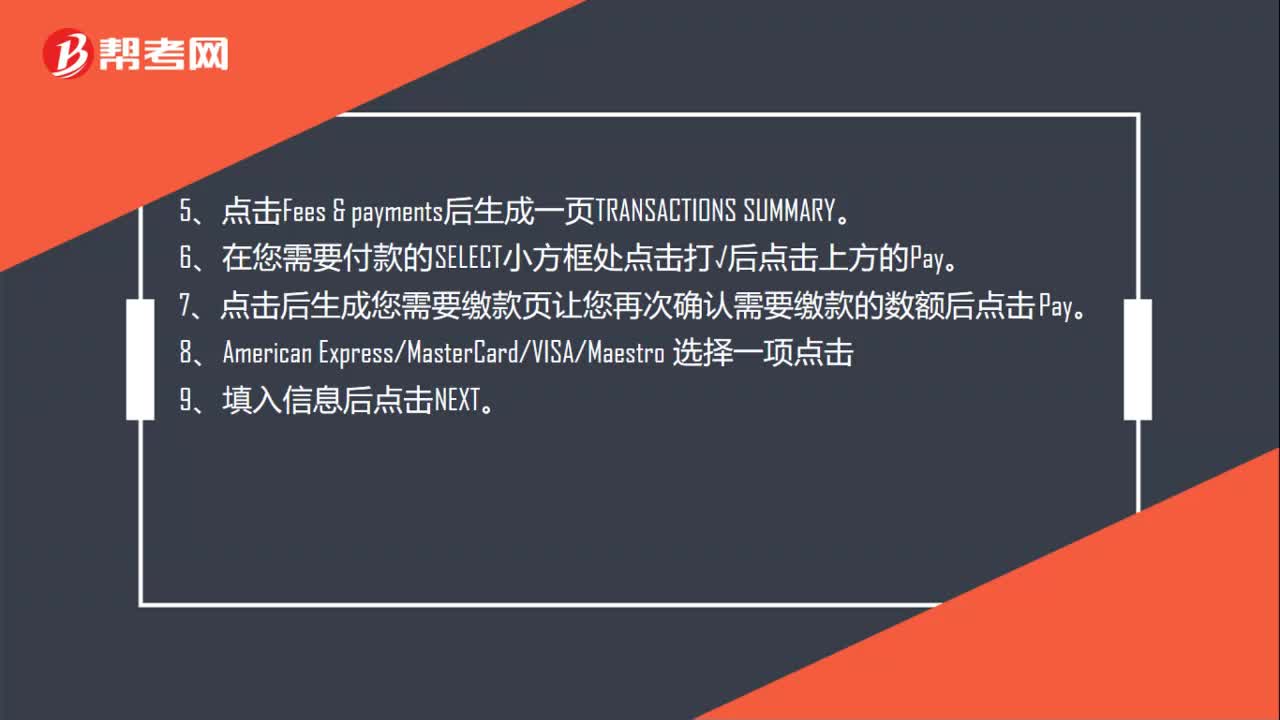

64ACCA年费怎么缴费?:ACCA年费怎么缴费?ACCA年费缴纳步骤如下:1、登陆ACCA全球官网。3、输入您的学员号和密码。进入您的个人空间。5、点击Fees。payments后生成一页TRANSACTIONS SUMMARY。6、在您需要付款的SELECT小方框处点击打√后点击上方的Pay7、点击后生成您需要缴款页让您再次确认需要缴款的数额后点击Pay9、填入信息后点击NEXT

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料