当前位置: 首页ACCA考试管理会计(基础阶段)每日一练正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

备考ACCA考试,好的学习方法很重要,但是练习也很重要,下面帮考网就给大家分享一些,ACCA考试F2考试试题,备考的小伙伴赶紧来练练手吧。

1.A company operates a job costing system. Job number 1207 requires $80 of direct materials and $120 of direct labour. Direct labour is paid at a rate of $12 per hour. Direct expenses for the job are $50. Production overheads are absorbed at a rate of $40 per direct labour hour and non-production overheads are absorbed at a rate of 110% of prime cost.

What is the total cost of job number 1207?

$()

答案:$925

Prime cost= $250 (80 + 120 + 50)

Overheads = $675 ((120/ 12)x40) + (1.1 X 250)

Total cost= $925 (250 + 675)

2.Which TWO of the following problems are associated with performance measurement in public sector organisations?

A.The profit is difficult to measure

B.Unable to compare with the competition

C.Performance measures are difficult to define

D.Regional benchmarking cannot be carried out

答案: Unable to compare with the competition and Performance measures are difficult to define

It is not possible to compare with the competition. With public sector services there is rarely any market competition. This makes it difficult to know whether they are performing well.

Performance measures are difficult to define. Measures of output quantity and output quality provide insufficient evidence of, for example, a local authority\'s success in serving the community.

Regional benchmarking is a useful way of overcoming performance measurement problems in the public sector.

Public sector organisations rarely exist to make a profit so attempts to measure profit are invalid.

3.A company manufactures and sells a single product. Next year the budgeted total fixed production costs are $480,000, budgeted sales are 24,000 units and budgeted production is 25,000 units. The budgeted profit for next year using absorption costing principles is $57,500.What is the budgeted profit for next year using marginal costing principles?

A.$76,700

B.$77,500

C.$38,300

D.$37,500

答案:$38,300

Budgeted fixed production cost per unit = $19.2 (480,000 125,000)

Marginal costing profit = $38,300 (57 ,500 - (25,000 - 24,000)x 19.2)

以上就是帮考网分享给大家的ACCA考试F2考试试题的内容,希望可以帮助到大家。如果想要了解更多关于ACCA考试的试题,敬请关注帮考网!

25

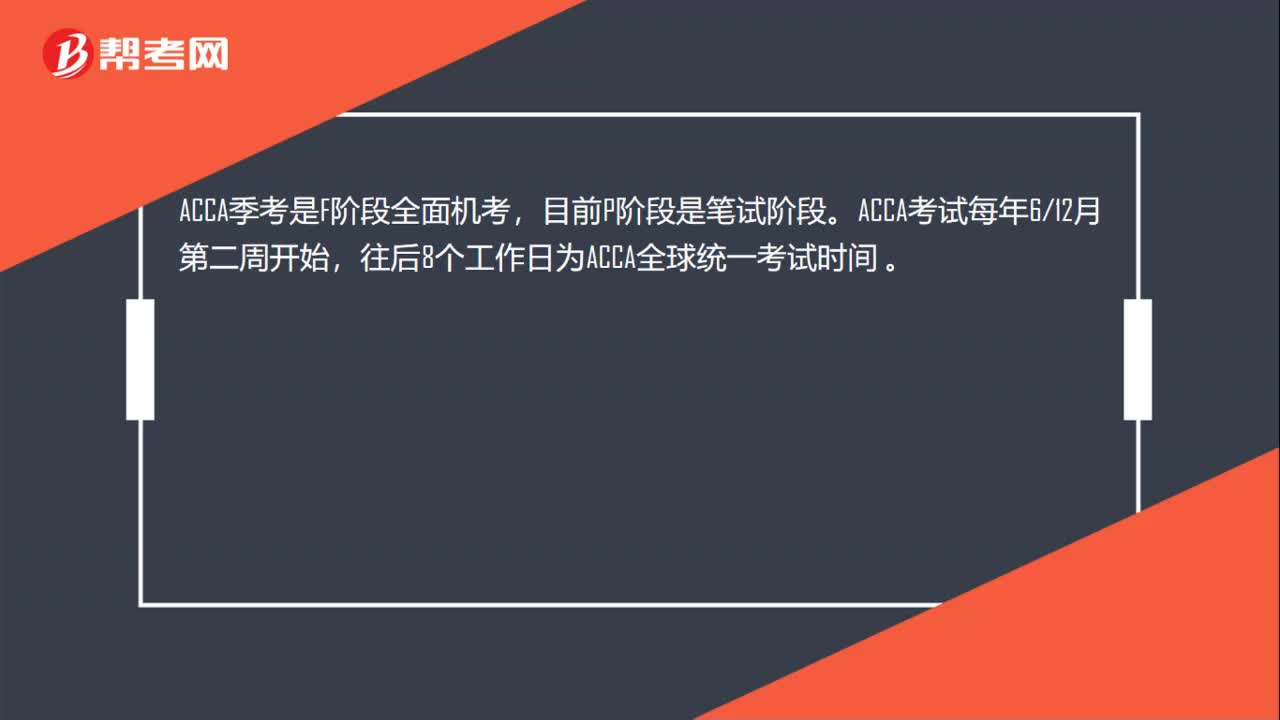

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

63

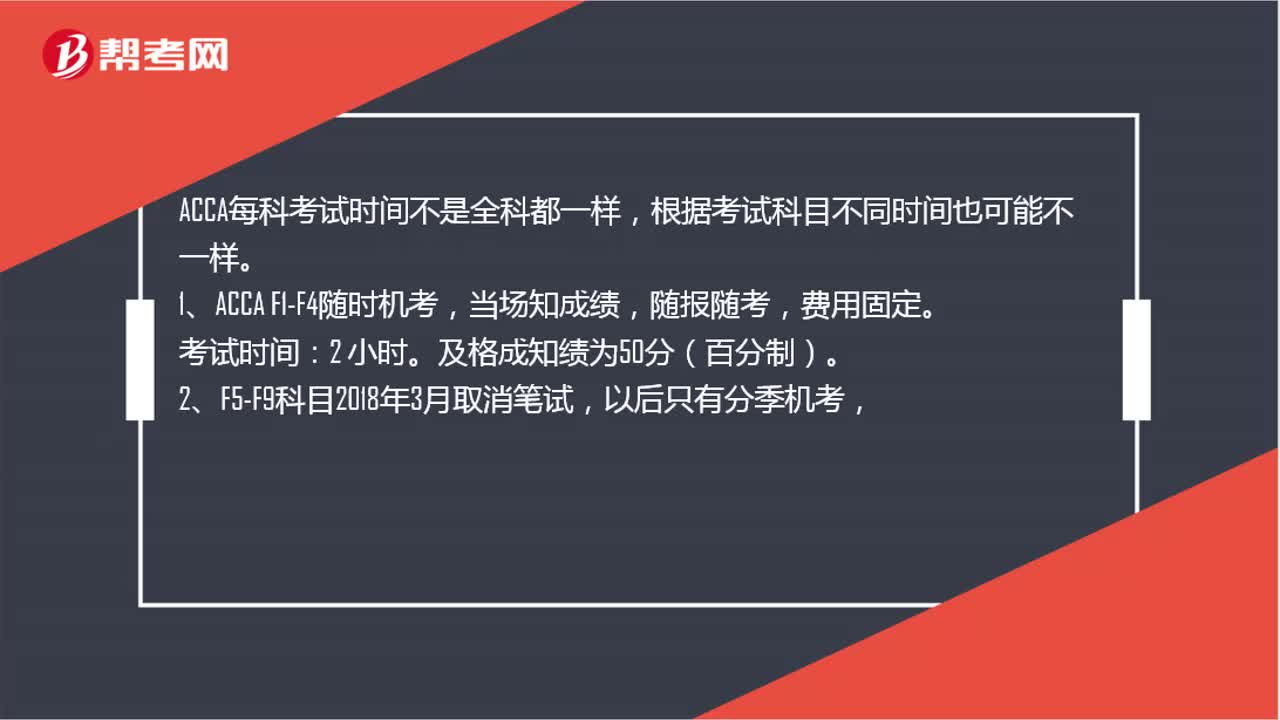

63ACCA每科考试时间都一样吗?:ACCA每科考试时间都一样吗?ACCA每科考试时间不是全科都一样,根据考试科目不同时间也可能不一样。1、ACCA F1-F4随时机考,当场知成绩,考试时间:及格成知绩为50分(百分制)。2、F5-F9科目2018年3月取消笔试,以后只有分季机考,每年3、6、9、12月4个考季,机考时间:另有10分钟时间阅读考前须知,3、ACCA专业P阶段所有课程考试时间为3小时,及格成绩为50分(百分制)。

56

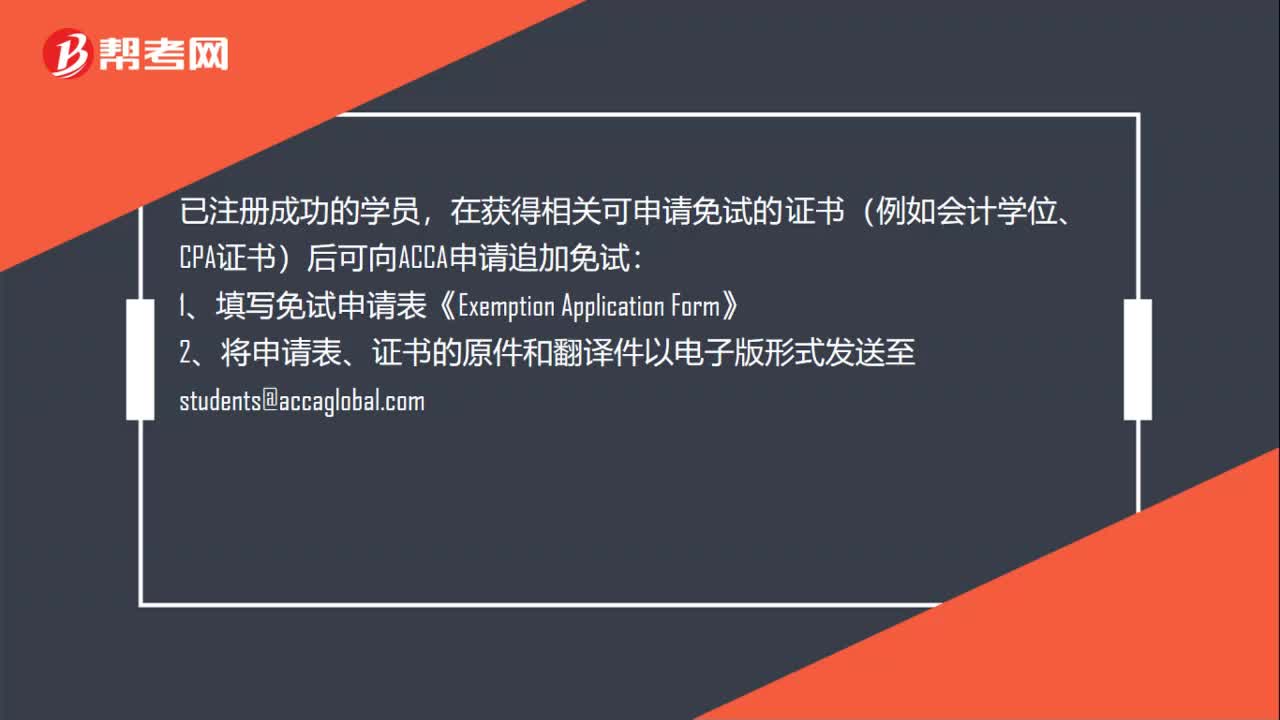

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料