当前位置: 首页ACCA考试管理会计(基础阶段)每日一练正文

下载亿题库APP

联系电话:400-660-1360

下载亿题库APP

联系电话:400-660-1360

请谨慎保管和记忆你的密码,以免泄露和丢失

请谨慎保管和记忆你的密码,以免泄露和丢失

特许公认会计师公会(The Association of Chartered Certified Accountants)简称ACCA,成立于1904年,是目前世界上领先的专业会计师团体,也是国际学员最多、学员规模发展最快的专业会计师组织。今天我们要看的就是ACCA考试中P2科目的每日一练,希望大家能从做题过程中提升自己。

Question:Which 3 of the following might be part of the fair value of purchase consideration on acquisition of a subsidiary?

A. Costs of issuing capital instruments to fund the acquisition.

B. Cash paid.

C. Quoted shares, at their market valuation.

D. Provisions for future losses of the subsidiary being acquired.

E. Due diligence investigation fees.

The correct answers are:

Cash paid;

Quoted shares, at their market valuation.

解析:Cash is the most obvious way of paying for an acquisition. However shares might be offered to the subsidiary's shareholders as well as cash. If the acquiring company is covering the costs of acquisition these form part of the total cost of the investment.

Fees associated with the acquisition must be expensed as incurred under the revised IFRS 3.

The costs of issuing capital instruments to fund the acquisition are specifically excluded under IFRS 3. These should be written off against the carrying value of the capital instrument.

Provision for future losses of the subsidiary being acquired is not allowed under IFRS 3 unless the outgoing subsidiary management incurred those liabilities since otherwise no obligating event existed at the time of combination. If so this would impact the assets and liabilities being transferred not the purchase consideration. If the liability were incurred post-acquisition it would not be part of the cost of the investment on acquisition.

备考之路漫长艰辛,需要大家持之以恒,每天要进行复习,切忌三天打鱼两天晒网,帮考网会一直在您的身边,支持您,陪伴您。祝愿大家早日功成名就!!!

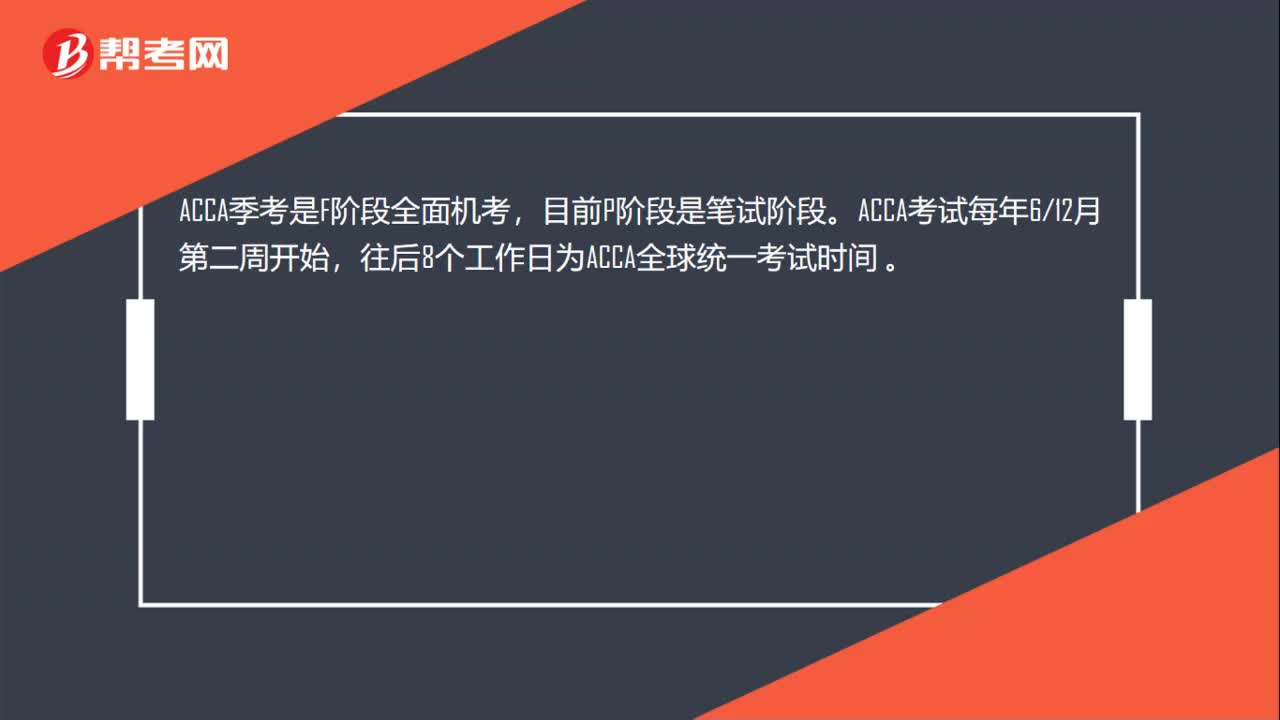

25

25ACCA每年的考试时间是什么时候?:ACCA每年的考试时间是什么时候?ACCA季考是F阶段全面机考,目前P阶段是笔试阶段。ACCA考试每年612月第二周开始,往后8个工作日为ACCA全球统一考试时间。

63

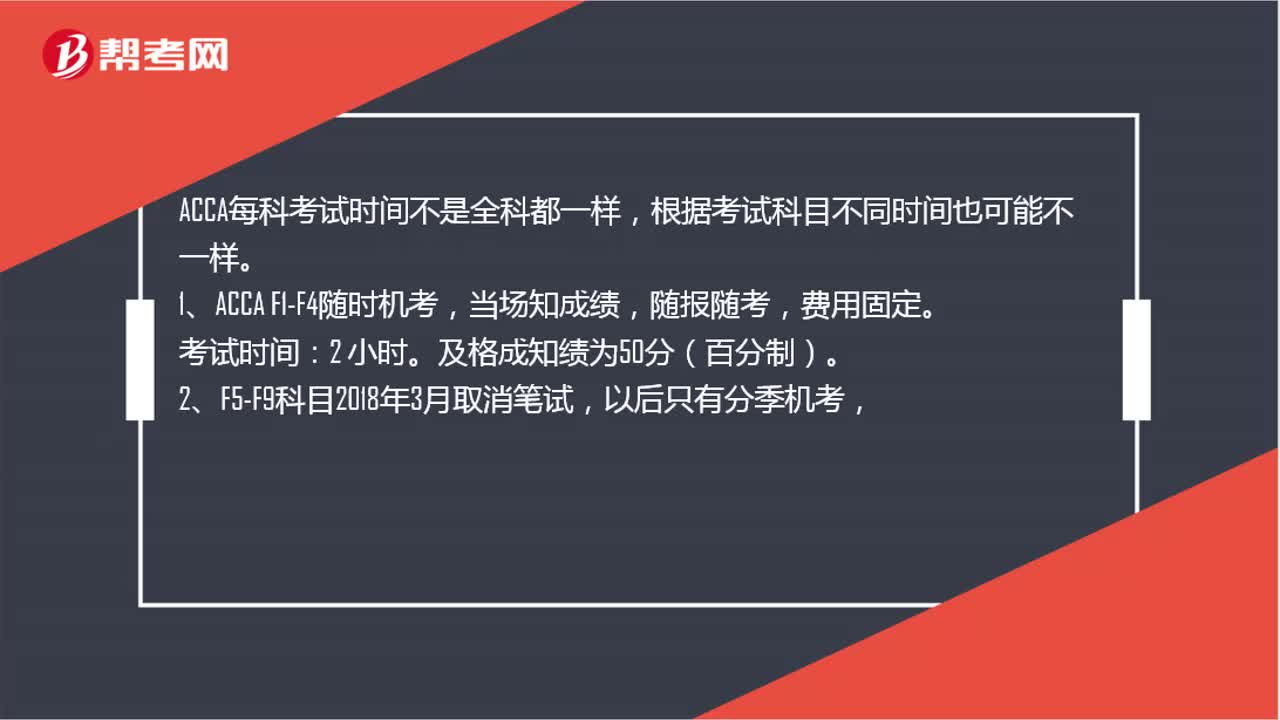

63ACCA每科考试时间都一样吗?:ACCA每科考试时间都一样吗?ACCA每科考试时间不是全科都一样,根据考试科目不同时间也可能不一样。1、ACCA F1-F4随时机考,当场知成绩,考试时间:及格成知绩为50分(百分制)。2、F5-F9科目2018年3月取消笔试,以后只有分季机考,每年3、6、9、12月4个考季,机考时间:另有10分钟时间阅读考前须知,3、ACCA专业P阶段所有课程考试时间为3小时,及格成绩为50分(百分制)。

56

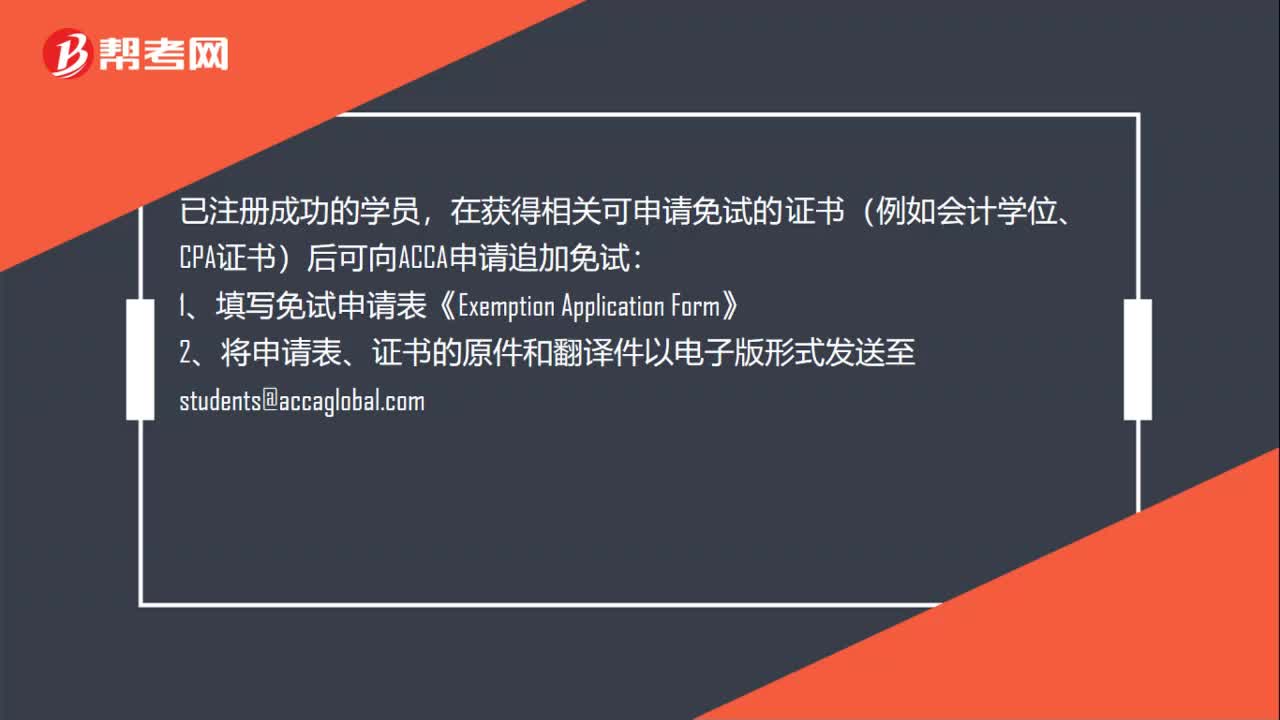

56ACCA考试怎么申请免考?:ACCA考试怎么申请免考?已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试:1、填写免试申请表《Exemption。2、将申请表、证书的原件和翻译件以电子版形式发送至students@accaglobal.com:3、请注意查收邮件或登录MYACCA学员账户查看免试信息,4、确认时间为5个月左右版;(例如,7月15日前提交申请12月考试生效

01:03

01:032020-06-04

01:20

01:202020-06-04

01:21

01:212020-06-04

00:34

00:342020-06-04

00:19

00:192020-06-04

微信扫码关注公众号

获取更多考试热门资料